dlphoto6/iStock via Getty Images

Overview

As a dividend growth investor, I like to find opportunities across all sectors that may add value to my overall portfolio. A good place to start would be to first research a list of companies that have an established track record at raising their annual dividend payout amounts year over year. Lindsay Corporation (NYSE:LNN) caught my attention because they’ve increased their dividend payouts for over 21 consecutive years in a row. While this serves as a good starting point to understand how much the company may value their dividend, there are more layers to this that can determine whether or not the stock fits my needs.

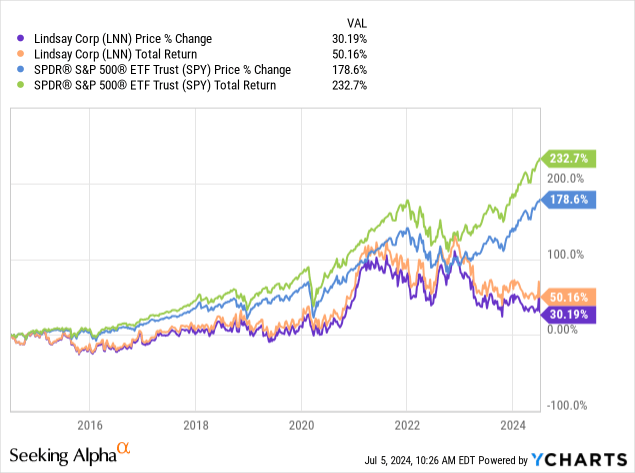

In addition to consistent dividend growth, I like to assess how well a company’s financials are doing through different types of economic environments, as well as how consistent the price growth has been over time. We can see that the Lindsay Corporation has provided a 32% price increase over the last decade, and the inclusion of dividends helps brings the total return profile up over 50% over the same time frame. However, we can see that this performance significantly underperforms that of the S&P 500 (SPY) just as a reference point.

Data by YCharts

Data by YCharts

Just for a bit of context, the Lindsay Corporation operates as an infrastructure service-based business. The company generates its earnings through two main segments: irrigation and infrastructure. LNN sells equipment that has its own unique purposes within the sector, which means that it can be vulnerable to macroeconomic conditions that may limit spending. This is reinforced by the fact that LNN’s public inception dates back to 1997, so we have over two decades worth of data to reference and how performance has played out during unfavorable market cycles.

I believe that we currently sit in one of these unfavorable environments, and that’s why we’ve seen the price come down from its prior highs. I believe the main culprit to be the higher interest rate environment that we remain in, as this causes a trickle-down effect of lower spending and lower sale volumes. Let’s first start by reviewing the company’s financial performance as of recently.

Lindsay Financials

The company recently reported their Q3 earnings at the end of June, as the results showed some weakness. Revenue came in at $139M for the quarter, representing a large 15.4% year-over-year decrease. However, earnings per share came in at $1.85 and beat expectations by $0.68. Additionally, operating income also came in at $19.9M which represents a decrease of 26% year over year. These losses can be attributed to the less favorable environment for LNN at the moment.

The business operates through two main segments, and the irrigation area is much larger in scale. The North America irrigation segment saw revenues land at $68.2M, which is a 9% decrease from the prior year. This was driven by lower unit sales of irrigation equipment and parts. International revenue in the segment also decreased due to lower sale numbers throughout Brazil and Latin America markets. Management seems to believe that order activity is constrained due to the impact that lower commodity prices have on farmer profitability and credit accessibility.

On a positive note, the lower revenue of irrigation was offset by a slight uptick in revenue from the infrastructure segment. Revenue landed at $24.4M for the quarter, which was an 11% increase from the prior year’s total of $22M. Operating income in this segment also increased by a massive 76%, amounting to $6.3M. These increases can be attributed to the higher project sales for ‘Higher Road Zipper System’, which is a moveable barrier technology that helps improve road safety and traffic flow. Despite the growth in this segment, it accounts for a smaller slice of the company’s overall revenue.

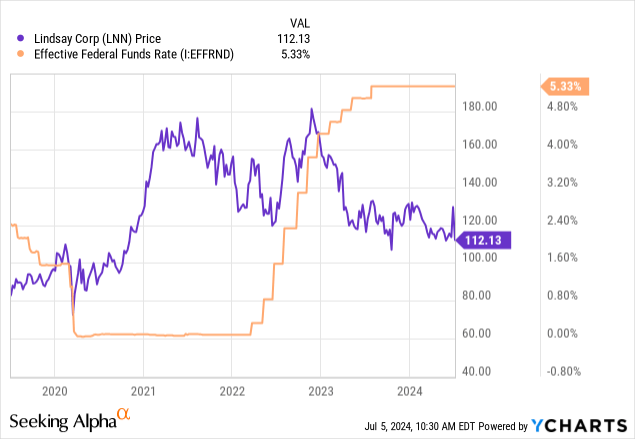

Since the main irrigation segment relies on sales from the farming industry, it remains vulnerable to shifts in spending within the category. As interest rates remain at their decade high level, it’s no surprise that there is less demand for LNN’s products. It’s also no coincidence that the price of LNN has had an inverse relationship to the federal funds rate. When rates were cut to near zero levels during the pandemic, the price rapidly increased due to more favorable borrowing costs and the fact that the economic environment encouraged higher levels of spending.

Data by YCharts

Data by YCharts

Conversely, as rates started to increase at the start of 2022, we saw LNN’s price fall to the downside over the next year. The price has recently stabilized only now, and I believe that this was caused by the market anticipation around possible interest rate cuts on the horizon. With inflation starting to cool and the unemployment rate now sitting at the 4% rate, we are starting to get closer to an environment that may serve as an incentive for the Fed to consider reducing interest rates. Therefore, we may possibly be at the tail end of these unfavorable conditions for LNN and sales volumes within the irrigation segment may start to increase again.

LNN Q3 Presentation

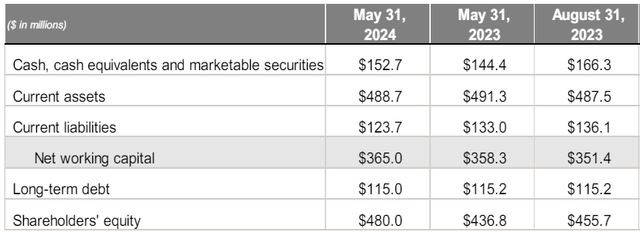

In the meantime, LNN’s balance sheet has remained solid, with cash and equivalents and marketable securities totaling $152M. They’ve slightly increased their cash position over the last year to obtain a more defensive position, which may help the company ride out the ongoing headwinds. They’ve also worked on their long-term debt by not accumulating anymore and slightly decreasing the amount of debt by about $200k.

Underwhelming Dividend Growth

Despite the cyclical challenges of the sector, LNN has been able to still grow their dividend. The most recent 3% raise at the end of June helps instill investor confidence, and as of the latest declared quarterly dividend of $0.36 per share, the current dividend yield sits at a small 1.2%. Despite LNN managing to increase the dividend for over 21 consecutive years in a row, the level of growth just doesn’t satisfy my appetite as a dividend growth investor.

For instance, over the last ten year period, the dividend has been increased at a CAGR (compound annual growth rate) of 6.02%. While this would be an acceptable level of growth for a stock yielding around 3% to 5%, I expect a significantly higher growth rate from a company that has an average dividend yield of around 1%. The growth of the dividend has been even more underwhelming in a smaller time frame. For example, the dividend increased at a CAGR of only 2.46% over the last five year period. This sort of growth rate doesn’t have enough of an impact to increase your yield on cost over a long holding period, which is proven by the current five year yield on cost of 1.7%.

On a more positive note, the dividend at least remains well covered. The dividend payout ratio sits at a very comfortable 21.24%. This undercuts the sector median dividend payout ratio of about 30%. In addition, LNN has a very healthy interest coverage ratio of 25.5x, which is significantly greater than the sector median of 7x. Unfortunately though, the dividend metrics here do not support enough of a case for consideration as part of my portfolio.

LNN Stock Valuation

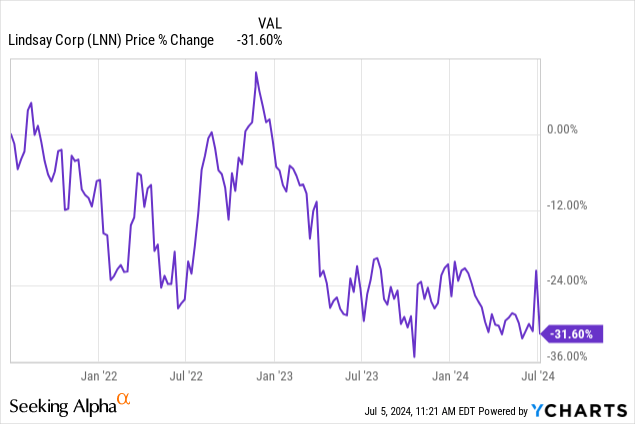

Although LNN may not fit from a dividend growth perspective, there may be an opportunity to capture the price recovery that may be fueled by interest rate cuts. As interest rates get reduced, the cost of borrowing becomes more attractive and farmers may start to purchase LNN products at higher volumes. The price has now fallen over 30% over the last three year period and as conditions improve, there could be an opportunity here to capitalize with some nice upside.

Data by YCharts

Data by YCharts

Wall St. seems to agree when you consider that the average price target now sits at $134 per share. This represents a potential upside of 18.6% from the current level. Even the lowest price target of $126 per share remains above the current price level. In terms of valuation metrics, I do see some indications that LNN currently sits at an undervalued level. For example, the current price to earnings ratio sits at 17.3x, which undercuts the sector median price to earnings ratio of 23.3x. The price to book ratio also sits at 2.6x, which remains under LNN’s five-year average price to book ratio of 4x.

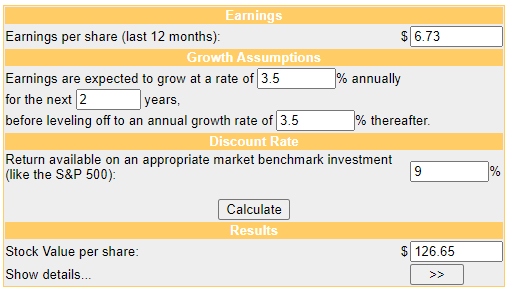

In an effort to get another source of reference for valuation, I also wanted to run a discounted cash flow calculation, which will help determine an estimated fair value. Free cash flow per share currently sits at $6.73 and although EBITDA growth has been negative as of recently, the sector median EBITDA growth sits at 8%. Taking the current unfavorable environment into consideration, I wanted to have a more conservative outlook, so I think that an estimated growth rate of 3.5% would be ideal here and obtainable in an environment where interest rates start to come down. Just as a reference, forward revenue growth for LNN has averaged 5% over the last five year period.

Money Chimp

With these inputs in mind, I come to an estimated fair value of $126.65 per share. This would represent a double digit upside potential of over 12% from the current levels, assuming that a 3.5% growth rate can be achieved in more favorable conditions. This can be considered a conservative estimate when we take into account management’s five year financial goal to grow organic revenue by 7% and earnings per share by 10%.

Risk Profile

Since the relationship between LNN and the federal funds rate is clear, the future risk of rate sensitivity remains. We can only hypothesize what will happen surrounding interest rates by looking at inflation, labor market, and consumer spending data. However, the US Presidential elections are happening towards the tail end of 2024, and this may present elevated levels of uncertainty in the markets. In a case where interest rates remain unchanged or even increase further, I believe that LNN will continue to stay suppressed or even fall further.

LNN Q3 Presentation

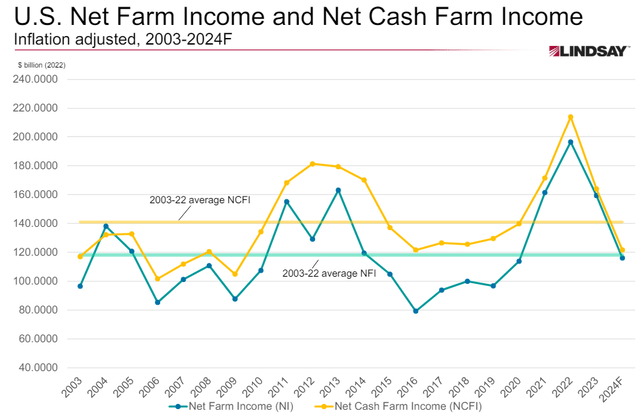

While the cash management of LNN has been solid so far from a balance sheet perspective, the vulnerability and sensitivity to influences outside of their control is still a challenge. We can see that the net farm income and cash of US-based farms have significantly decreased alongside the rise of interest rates. Not only do higher interest rates make it a less attractive spending environment, but it also increases the burden of maintaining any current debt balances if these loans were issued on a floating rate basis.

Debt on a floating rate basis would mean that monthly payments would increase as a result of higher interest amounts due. As cash positions decrease and remain suppressed, it’s very likely that we continue to see LNN’s sale figures suppressed as well. This cyclical vulnerability makes LNN less attractive and takes away from the ‘buy and forget’ appeal, since it requires you to actively track performance and find the most opportune times to add to your position to see significant returns.

Takeaway

In conclusion, LNN remains vulnerable to changes in the interest rate environment. While the current high interest rate environment has suppressed prices, it may have equally created an opportunity to capture the upside price recovery. I am issuing a Hold rating simply because this style of investing is not for me. I prefer holdings that are buy and hold style of companies and provide a total return that is comprised of both consistent price appreciation, as well as a growing stream of dividend income. The dividend growth here is a bit too weak for my taste, and therefore I will be remaining on the sidelines.

However, the current valuation suggests that there is a potential for a double digit upside from here, assuming a 3.5% growth rate. Management is targeting a 7% revenue growth and 10% EPS growth over the next five years, which may add some optimism. This may present a good short-term opportunity. However, the long-term performance has not been attractive enough for me to consider a position as the price has only appreciated by 30% over the last decade and the dividend has not grown at a high enough rate for my appetite.

GIPHY App Key not set. Please check settings