Jessie Casson

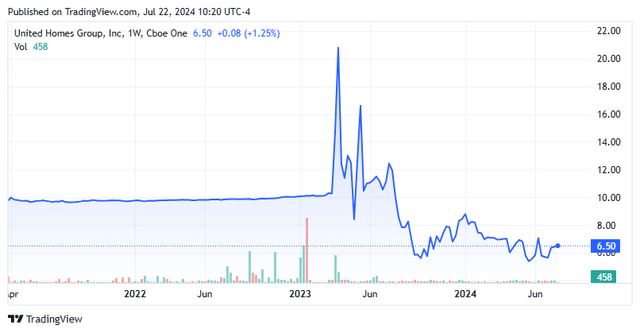

Shares of home builder United Homes Group, Inc. (NASDAQ:UHG) have fallen 65% in the past 13 months as high interest rates have countered migration tailwinds and a lack of existing homes for sale. The company predominantly builds in South Carolina but is looking to grow within and beyond the state line through acquisition, of which it has made three since going public in March 2023. With low float and no Street coverage, the two considerable insider transactions on June 7th and 10th merited a deeper dive into this small-cap home builder. An analysis follows below.

Seeking Alpha

Company Overview:

United Homes Group, Inc. is a Chapin, South Carolina-based home builder with a focus on entry-level, first move-up, and second move-up single-family houses in South Carolina, North Carolina, and Georgia. Having constructed over 14,000 homes since its inception in 2004, the company ranked as the 25th largest single-family starter-home builder in the U.S. by Pro Builder magazine in 2022. Originally founded as Great Southern Homes, United Homes changed to its current moniker when it merged into special purpose acquisition company (SPAC) DiamondHead Holdings Corp. in March 2023, receiving net proceeds through a PIPE investment of $94.4 million. Its first official trade as a public concern was transacted at $22.70 per share, much higher than its current trading level of around $6.50 a share. The shares have an approximate market capitalization of $310 million.

The company is capitalized by two classes of stock. The 11.4 million shares of publicly traded Class A stock bestow economic interest and one vote per share. The 37.0 million shares of privately held Class B stock confers economic interest, two votes per share, and convertibility into Class A shares. All the Class B shares are effectively held by UHG’s Founder, CEO, and Chairman of the Board of Directors Michael Nieri and his family.

Operating Segments

Until going public, United almost exclusively conducted its operations in South Carolina, just expanding into North Carolina and Georgia. Its focus has been on the Upstate (Greenville and Clemson), Midlands (Columbia), and Coastal regions of the state with a small presence in Augusta, Georgia. Those territories fall under its South Carolina segment, with Raleigh, North Carolina and a mortgage banking joint venture with Homeowners Mortgage, LLC housed under a unit dubbed “Other.” That said, the preponderance of the company’s top and bottom lines come from South Carolina.

Approach

Before going public, United split off its land development unit from its home building operations, employing the former’s inventory of owned and controlled lots as a pipeline. In essence, it used a land-light operating model where it enters into option agreements and land banking arrangements to later reacquire those developed lots – if it so chooses – which comprised the preponderance of its 10,900-lot inventory on March 31, 2024. The home builder is currently constructing homes on 63 active subdivisions at prices typically ranging from $200,000 to $600,000.

Buttressed by the statistic that its principal markets are located within 500 miles (ca. 805 km) of 10 of the top 15 fastest growing metropolitan statistical areas in the U.S., management’s strategy involves rapid expansion within and beyond South Carolina. With demographic tailwinds and a puffed-up balance sheet from the SPAC merger, the company has executed three acquisitions since going public. This began with Raleigh-based Herring Homes in August 2023, which was supplemented by the subsequent addition of 50 building lots and 12 homes under construction for a total consideration of $13.0 million. Those transactions were followed by a $24.7 million acquisition of Upstate home builder Rosewood Communities in October 2023. United’s most recent purchase was Myrtle Beach home builder Creekside for a cash consideration of $16.9 million in January 2024.

Share Price Performance

United did have the misfortune of going public at the tail end of the Federal Reserve’s battery of rate hikes, which commenced in March 2022 and continued through July 2023. Save for some initial optimism due to strong market undercurrents in its demographic, shares of thinly traded UHG have not poked their head above $10 since mid-August 2023. This is owing largely to undelivered rate cuts due to stubborn inflation, which has negatively impacted housing affordability. With buyer demand attenuated, the company’s financial performance has suffered, reflected in its stock price, which is down over 60% in the past 14 months.

1Q24 Financials

With that as the backdrop, United’s 1Q24 financial report fit the axiom of, “if a tree falls in the forest and no one hears it…” Released before the opening on May 10, 2024, a total of 7,900 shares exchanged hands in the subsequent trading session. As for the metrics, the company posted 1Q24 non-GAAP net earnings of $2.79 million ($0.04 a share) and Adj. EBITDA of $7.3 million on revenue of $100.8 million (on 311 closings) versus non-GAAP net earnings of $5.46 million ($0.15 a share) and Adj. EBITDA of $8.5 million on revenue of $94.8 million (on 328 closings) in 1Q23. Average selling price (ASP) improved $21,000 (7%) year-over-year to $335,000, while net new home orders fell to 384 from 389 in 1Q23. Backlogs, representing homes sold but not yet closed, fell 18% year-over-year to 262 at a value of $78.7 million.

Balance Sheet:

An example of United’s land-light model occurred through an arrangement with a land banking partner in 1Q24. It was able to receive net cash of $14.1 million for finished lots worth $17.8 million and the optionality to repurchase them at a predetermined price. Owing to accounting rules, the $14.1 million is recorded as a liability and the $17.8 million remains an asset under the heading of “real estate inventory not owned.” As for liquidity, the company held cash and equivalents of $28.7 million with $66.3 million remaining on a revolving line of credit as of March 31, 2024. Debt, in the form of a convertible note, was $68.5 million.

Owing to its stock’s incredibly small float, it is not surprising to see no Street coverage, although BTIG analyst Carl Reichardt did participate on the 1Q24 conference call.

That said, the Nieri family, consisting of Founder, Chairman, & CEO Michael (621,328 shares), beneficial owner Maigan (278,150 shares), and Co-Executive VP of Construction Pennington (1,403,019 shares) is clearly bullish. They collectively invested $11.5 million at $5 per share to (very likely) buy out part of DiamondHead’s remaining SPAC position in two transactions that took place off-board on June 7 and 10, 2024. The rationale for that conclusion is twofold: 1. the volume of the two transactions (1.414 million on June 7th and 0.888 million on June 10th) were orders of magnitude more than the 6,200 and 8,200 shares that traded on the NASDAQ on those respective days; and 2. the $5 price was below the trading range realized on both days.

Verdict:

These peculiar and outsized transactions notwithstanding, the Nieri family sees construction cycle times returning to pre-pandemic levels, cheaper lumber, a lack of existing home inventory, and migration tailwinds as reasons to be bullish. Their optimism is further buttressed by United’s hedging through its land-light business model. However, interest rates haven’t meaningfully budged, and even if the Fed eases, there is no guarantee that the long end of the curve will follow. Their stock trades at an EV/TTM Adj. EBITDA of just under nine, which is marginally attractive, but business is dour.

Case in point: In its first four full quarters as a publicly traded concern, its Adj. EBITDAs versus their prior year periods have been as follows: $13.1 vs. $27.8 million (2Q23 vs. 2Q22), $8.8 vs. $18.0 million, $10.0 vs. $17.7 million, and $7.3 vs. $8.5 million (1Q24 vs. 1Q23) for a total of $39.2 million vs. $71.7 million, or down 45% partially “aided” by three acquisitions. Its FY23 top line was down 12% with partial help of two onboarded home builders.

United Homes Group, Inc. business is poor and there are no signs of improvement, despite its higher 1Q24 ASP. Factoring in the extremely illiquid market for its stock, which can further add cost to investment, United’s valuation needs to become much more compelling before purchase is recommended.

GIPHY App Key not set. Please check settings