Adam Gault

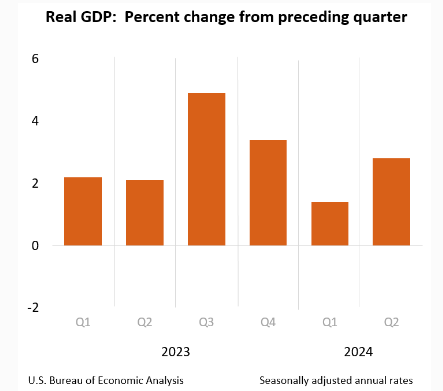

The initial reading of second quarter GDP growth came in at 2.8% last week, far exceeding the two percent consensus. However, this number should be taken with several caveats. First, like most economic readings over the past 12-18 months, that number is likely to revised down like almost every single monthly BLS jobs report since the start of 2023.

U.S. Bureau Of Economic Analysis

It also meant that GDP growth in the first half of 2024 initially stood at 2.1% (First quarter GDP growth was 1.4%). To put context, that is roughly half of the GDP growth that occurred in the back half of 2023. More importantly, it was accomplished thanks largely to a federal deficit that is running near seven percent of GDP (government spending counts in GDP calculations) so far in 2024. In that context, economic growth currently is hardly impressive.

It is also becoming quite apparent that the consumer is under increasing duress. Given consumer spending makes up nearly 70% of economic activity, it is difficult to see how we avoid at least a shallow recession over coming quarters, even if the Federal Reserve finally cut rates as expected at its September FOMC meeting.

The environment for various segments of the consumer population continues to break down, especially for lower- and middle-income tiers. This was made obvious via management commentary following first quarter earnings reports from well-known consumer names such as Home Depot (HD), Starbucks (SBUX), Nike (NKE), Target (TGT) and myriad others. I expect that negative feedback loop to continue in the second quarter, despite the recent, robust initial reading of Q2 GDP growth.

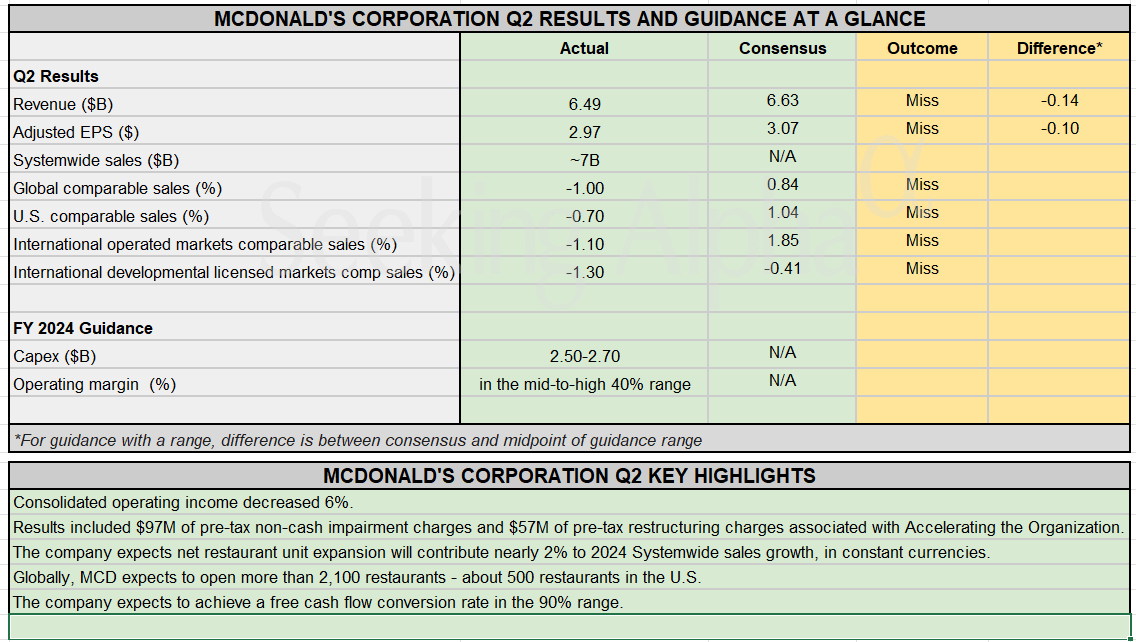

McDonald’s via Seeking Alpha

McDonald’s Corporation (MCD) might be the canary in the consumer coal mine around this trend. The fast-food giant reported Q2 results before the bell on Monday. Quarterly numbers missed both the top and bottom-line analyst firm consensus. Global same-store sales (non-inflation adjusted) fell one percent on a year-over-basis. That is the first time this has happened since the COVID-19 pandemic. Management did say that the return of its temporary $5 value meal menu is helping to boost traffic, as consumers are increasingly looking for bargains.

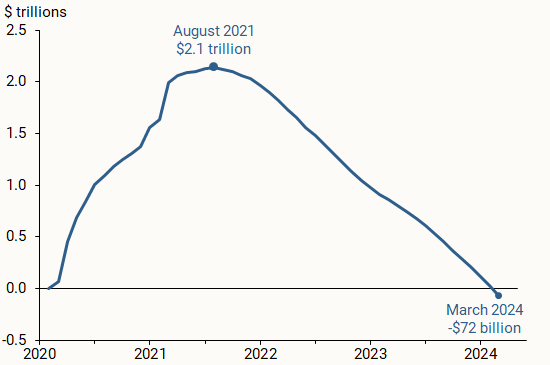

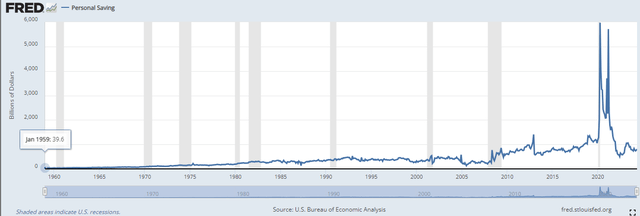

U.S. excess personal savings (Bureau of Economic Analysis)

The American consumer faces myriad headwinds. While inflation has ebbed significantly since peaking in the early summer of 2022 at 9.1%, the average American household has lost ground to inflation since the start of 2021. Consumer spending was sustained for quite some time by the huge amount of excess savings from the various COVID-19 era stimulus programs.

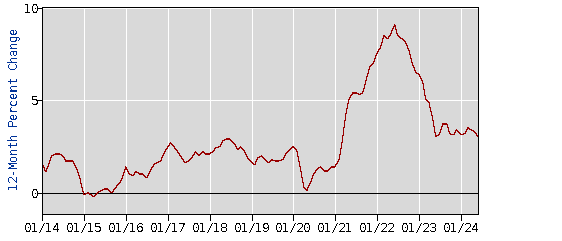

U.S. CPI (U.S. Bureau Of Labor Statistics)

Those savings are now gone, and the U.S. personal savings rate is back down to historical lows and half the pre-pandemic levels.

U.S. Personal Savings Rate As Of June 28th, 2024 (Federal Reserve Bank of St. Louis)

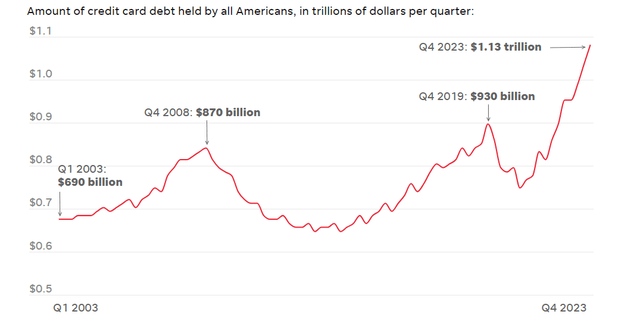

Many Americans have also turned to credit cards to maintain their standard of living. However, with credit card debt at record highs and credit card delinquencies at their highest levels since they started to be tracked by the Federal Reserve in 2012; that avenue is becoming less available.

U.S. Personal Savings Rate As Of June 28th, 2024 (Federal Reserve Bank of New York)

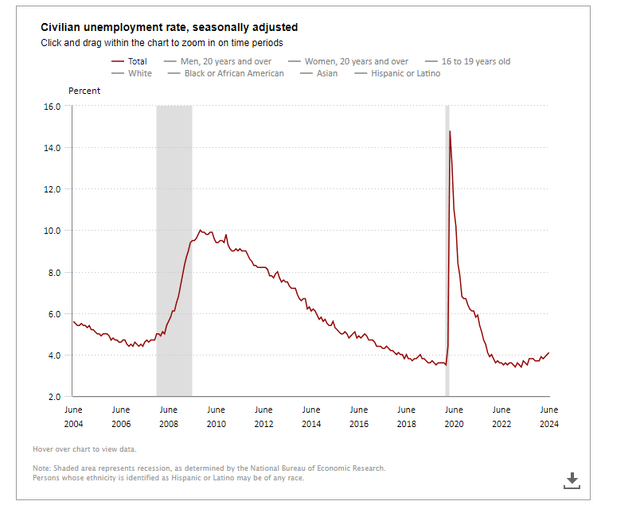

In addition, the jobs market has started to weaken over the past year. After hitting a nadir of 3.5% last summer, the unemployment rate had moved up to 4.1% by June of this year. We will get July BLS numbers on Friday, it should be noted. Total Job Openings recently hit a three-year low as well.

U.S. Bureau Of Labor Statistics

Given the myriad headwinds consumers face (slowing jobs market, lost buying power, low savings levels, growing credit card delinquencies, etc.), it is not surprising to see that 65% of Americans believe the country is heading in the wrong direction in the latest pollsversus just 24% that believe the nation is on the right track.

U.S. Census/ZeroHedge/Apartment List

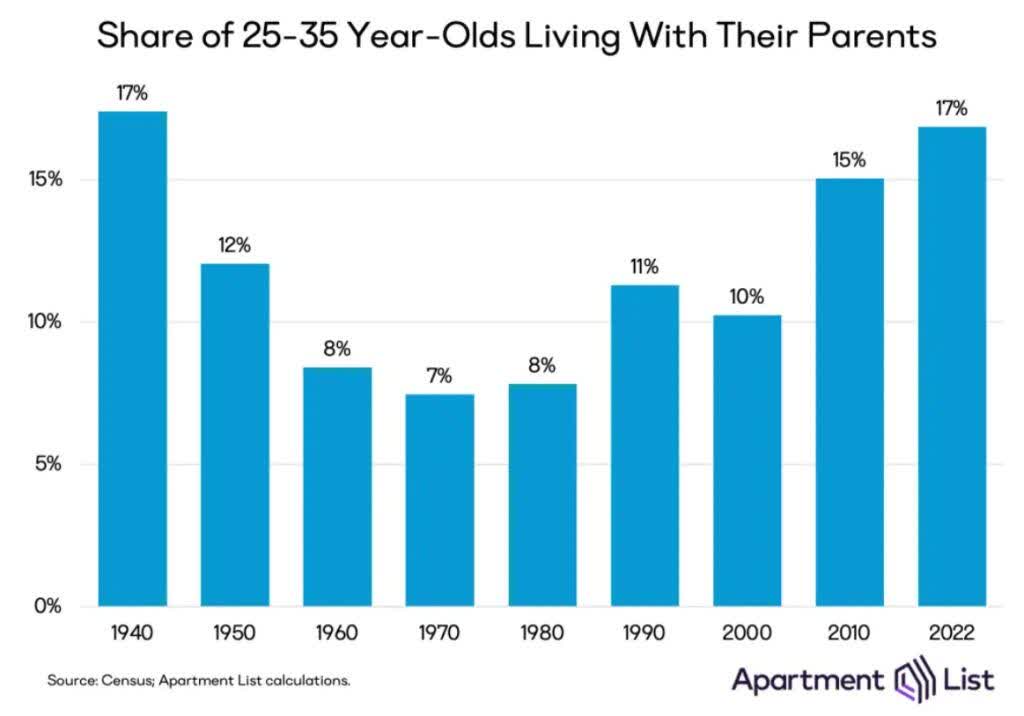

The current environment has been particularly hard on the younger generation. It faces near record lows in housing affordability, 33 straight months now where rents have increased by at least 0.4% on a month-over-month, and average monthly car payments that crested over $700/month for a new car late last year. It is hardly surprising, then, that a record percentage of 25- to 35-year-olds are still living at home.

The $64,000 question for investors with the market trading at over 22 times forward S&P 500 earnings is what is going to power solid economic growth when consumers, who contribute over two thirds of all economic activity, are under considerable pressure on so many different fronts?

The answer I come up with is that a consumer led recession is quite likely in the quarters ahead, and it is a key reason I remain quite wary of equities at these trading levels.

GIPHY App Key not set. Please check settings