MenzhiliyAnantoly

Investment Thesis

In our article in May this year on DHT Holdings, Inc. (NYSE:DHT), we concluded that it was our opinion that the VLCC’s earning potential should be good for the next 2 to 3 years.

It was based on the low order book and that even if this changes, it would still take 2 to 3 years before these new vessels could upset the favorable supply and demand dynamics.

The share price has been down 7% since our previous buy call.

DHT just came out with their Q2 results, allowing us to look at how this investment thesis is progressing.

DHT Q2 Financial Results

Their net income in Q2 came in at $44.5 million, equal to an EPS of $0.27. That is only two cents lower than the previous quarter.

The vessels in the spot market made earnings of $52,700 per day and the vessels on time charters made $36,400 per day. This worked out to an average TCE for the quarter of $49,100 per day.

There are now several listed shipping companies that distribute all, or close to all, of their EPS in dividends. These companies often generate more cash per share than earnings, so they are still able to allocate some of the capital towards Capex.

One good example of this is DHT.

In Q2, they paid down $51.5 million as the first instalment on the four newbuildings. To do this, they utilized $25 million from a revolving credit line and the balance came from cash generated.

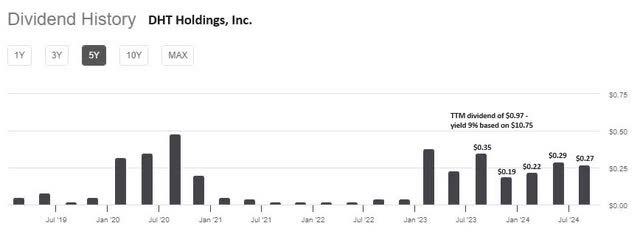

Our preference is to look at dividends on a TTM basis. The yield is presently 9%.

DHT’s dividend history (SA)

At the end of Q2, the leverage was 18.6% based on market values for the vessels. The net debt was $14.2 million per vessel. This is a very comfortable level, but should be expected to go up somewhat with the financing of the four newbuildings under construction.

We were pleased to see that DHT has managed to negotiate earlier delivery of the four newbuildings. This improvement means that they increase expected revenue days for 2026 by 550-600 days when compared to the contract dates. It should also save them some money on interest expenses, as earlier deliveries shorten the time frame of financing vessels that are not yet delivered.

Market Condition

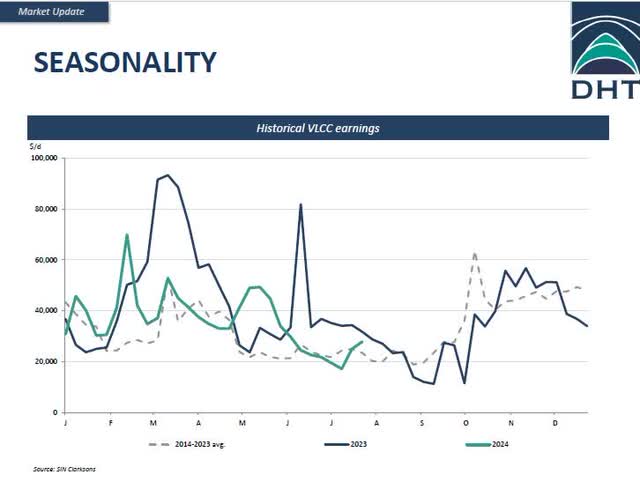

We expect lower earnings in Q3 as seasonality from year to year generally points to lower rates towards the latter part of the summer.

Seasonality points to lower earnings in Q3 (DHT Q2 Results Presentation)

DHT has covered 75% of their spot exposure in Q3 at an average time charter equivalent earning of $42,100 per day, which is $10,600 per day lower than what they achieved in Q2.

When we look at changes in demand, we can predict the changes that come as a result of cyclicality. At least history rhymes, if not repeat itself.

The trickier part is what comes from structural changes.

To the best of my knowledge, the management of DHT lives in Norway. This is a country that has adopted EVs faster than any other country on earth. As of last year, 82% of new cars sold were EVs. It is a tiny country with just 5 million people, so it is not that important.

However, China’s sales of EVs last year reached 24%. I would argue that China, with its political landscape, can make changes faster than Norway, if they want to. China has clearly shown the world that it wants to be a dominant force in the fields of EVs and renewable energy. Some of their export opportunities are shrinking, which means that domestic sales could come to their rescue.

The peak oil demand scenario could come earlier than many people have anticipated.

We are not arguing that there will be no need for crude oil anymore. But expect changes.

DHT’s CEO and President Svein Moxnes Harfjeld also pointed out in the conference call with analysts that heavy transportation is turning more to LNG as fuel in China, but on the positive note, the petrochemical industry is increasing. They do use crude oil as a feedstock to make things like chemicals and plastic.

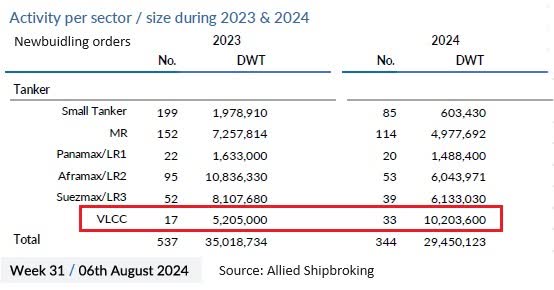

In terms of supply of tonnage, there has been more orders for VLCC’s as can be seen from Allied Shipbroking Weekly Market Report of 6th of August.

VLCC’s new-building order doubled so far this year (Allied Shipbroking)

Twice as many vessels have been ordered in the first seven months than what was ordered in the entire 2023.

However, the good thing is that these new vessels will not enter the market before 2026.

Risks to the Thesis and Conclusion

We believe that the probability of DHT earning insufficient to break even in the next two years is very low. There is, in our opinion, more upside potential in higher earnings.

But spot markets in dry or wet bulk shipping have surprised many in the past and are not for the faint-hearted. As such, the exposure to it is low in our portfolio. We think about it a bit like “spices” in the stew. It does add to our total return each year, but it is not the base of what the stew is made of.

DHT does have an interest in trying to put more of its vessels on long-term charters, such as what SFL Corporation (SFL) has. But so far, it seems that their customers, the major oil companies, are not willing to pay enough to make it worthwhile for DHT to do deals with them. They, meaning the oil companies, prefer that the shipowners take the market risk.

There are still many things we like about DHT and its management. We particularly like the transparency they deliver, and the equal treatment of all shareholders, not just their controlling shareholder.

We also share their optimism for the market for the next two years. This will not happen in Q3, as we have pointed out that lower earnings can be expected.

We have our sight for what is to come in Q4 and thereafter.

As such, we continue our Buy stance.

GIPHY App Key not set. Please check settings