Vertigo3d

Dimensional U.S. Targeted Value ETF (NYSEARCA:DFAT), first launched on 12/11/1998 as a mutual fund managed by Dimensional Fund Advisors, is now an active value ETF that measures its performance against the Russell 2000 Value Index.

The approach of this ETF is consistent with what indicators have the most predictive power for long-term outperformance and the track record supports this. With very low expense and turnover ratios and a portfolio of holdings that are relatively cheap and very profitable on average, I believe that managers will continue to provide the outperformance they have until now.

Methodology

The ETF was listed on 06/14/2021 but has existed as a mutual fund since 12/11/1998. The primary goal is to deliver returns that are attractive on an after-tax basis by delaying and minimizing the realization of net capital gains. To that end, the identification of long-term performance drivers seems appropriate and that’s what the issuer claims that managers emphasize.

This is an active ETF that identifies cheap and profitable stocks within the small and mid-cap range of the U.S. equity market and weights its securities based on market cap. Managers select stocks based on value and profitability as compared to other value stocks within the universe, which constitute the Russell 2000 Value Index, so the idea is to filter out the most undervalued and profitable stocks out of a group of stocks that already have value characteristics.

The primary metric that managers consider when assessing the value factor for each stock against the others is the relation between its price and book value. However, they may consider other metrics as well (e.g. price to cash flow, P/E, etc.) As for the profitability factor, they look at earnings or operating income on equity or assets.

In addition, managers consider ratios like asset changes to total assets so there is an emphasis on growth as well. That makes sense because while the value factor isolated from other ones can outperform in the long run, in retrospect it will have more explanatory power when it’s accompanied by quality and growth factors; it’s the more difficult justification in the undervaluation of companies with relatively strong fundamentals that makes a price “correction” more likely.

So, this ETF’s performance is primarily driven by factors that the market often ignores. The first, of course, is company size as measured by market capitalization. By excluding large-cap stocks which are most followed by the market and are generally slower growers of capital, the fund already gains an advantage over large-cap and total-market ones. The other factor is valuation as measured by the relation between price and book value, which is another important explanatory variable for performance in the academic world. However, the managers also consider quality and growth indicators to make investment decisions here which on their own cannot have predictive power because the market is supposed to price them in; but they do complement the value factor because of the reason I mentioned above.

Therefore, I believe that the approach here makes sense but only in the long term because I think that the selection of very undervalued stocks after a crash is a large contributor to the outperformance that value has realized over decades; one has to simply observe value’s underperformance in the most recent bull market to see that this is the case.

Such a fund could surely work as a satellite in one’s portfolio if the core is the S&P 500 as there would be no overlapping. But I also see DFAT as a core option for the firm believers of value investing who are in the wealth accumulating phase.

Performance & Cost

As of 07/31/2024, the fund has realized a 10.2% annualized return since its inception while the index returned 8.99%. This seems like a good return spread for a mutual fund but even more remarkable is its annualized performance of 8.49% after taxes on distributions and capital gains. This was recorded on 06/30/2024, when the index had returned 8.53% since inception, only 4 bps higher. So, it’s impressive that after accounting for taxes the returns were so close to those reflected by the index. Clearly, the fund’s goal mentioned in the previous section is not just marketing.

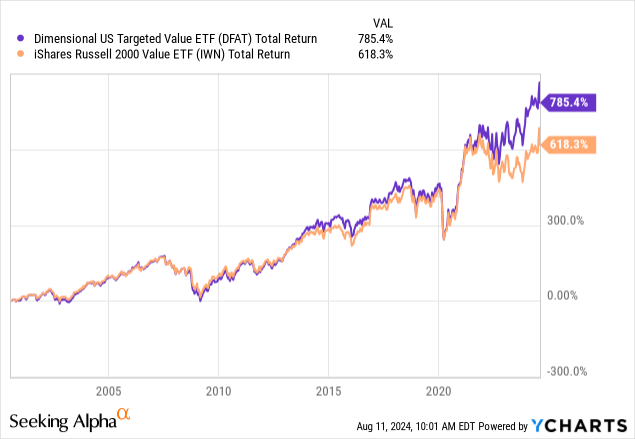

However, by looking at the total return performance of DFAT against an ETF that tracks the benchmark, it becomes clear that a big part of the outperformance came quite recently:

Data by YCharts

Data by YCharts

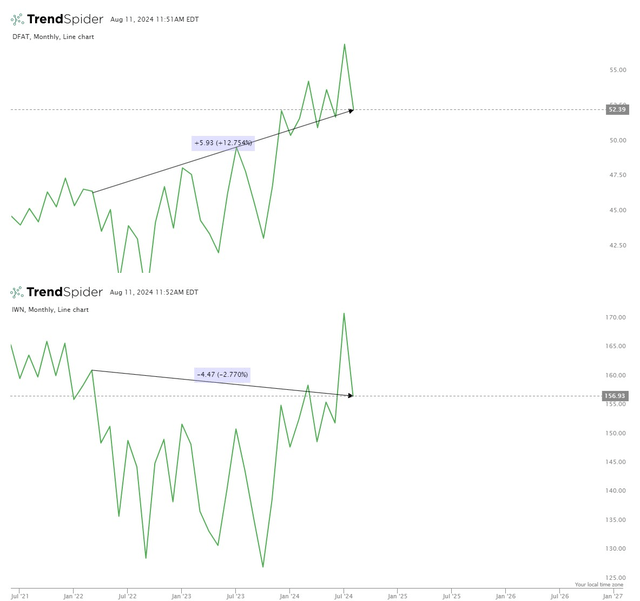

In fact, DFAT has more than recovered since the Fed rate hikes started while the index fund is not there yet:

TrendSpider

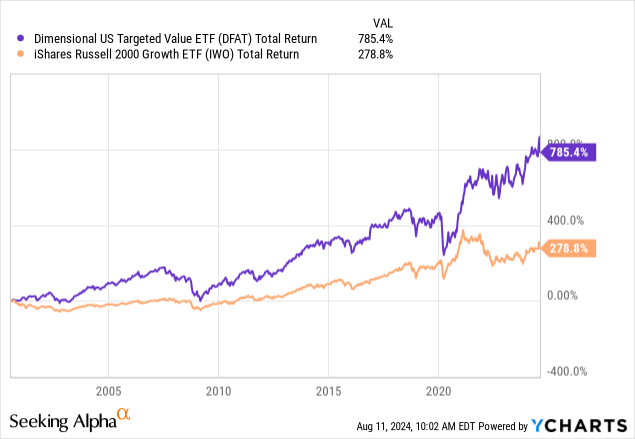

Because of this, I find the following comparisons more illustrative of the fund’s edge. First, DFAT outperformed its growth counterpart in the long run to such a degree that its track record becomes yet another piece of the evidence that value outperforms growth over time:

Data by YCharts

Data by YCharts

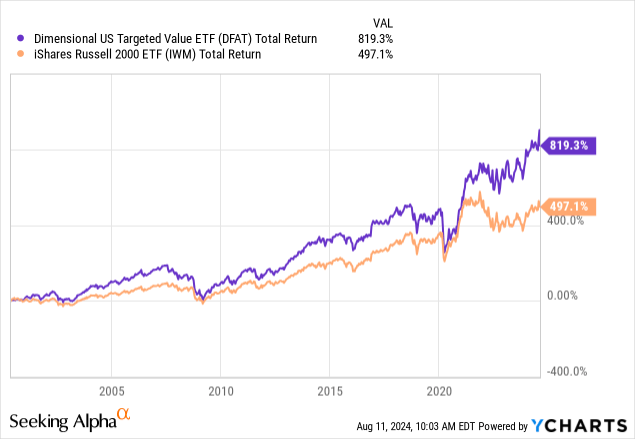

Also, it has been beating its vanilla counterpart since decades ago, reflecting how a value bias can deliver consistent outperformance:

Data by YCharts

Data by YCharts

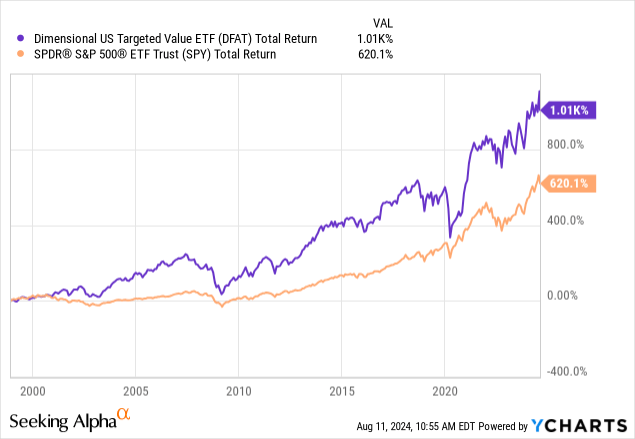

By comparing the fund’s performance to that of the SPDR S&P 500 ETF Trust (SPY) which allows for a comparison since the DFAT’s inception date as a mutual fund, one can easily see how significant the outperformance is:

Data by YCharts

Data by YCharts

Now, its aggregate book value premium is only 37% and its weighted average return on equity as measured by EBITDA to book value is 19%, both good indicators that the current portfolio is well-positioned to continue to outperform.

For an active fund, I also find the annual turnover of 3% as of 10/31/2023 and the net expense ratio of 0.28% very attractive. Going forward, this will be an important factor for DFAT’s returns, considering how transaction costs and management fees eat away the performance spread over time.

Risks

There are some risks you should know about before I conclude my thoughts. First, the exposure to mid-cap and small-cap equities makes for more of a risky investment than investing in a broad-market index fund that either focuses on large-cap stocks or includes all the U.S. stocks. As I already said, DFAT could be a good option for one’s core but only if there is enough faith in the approach to stick with it.

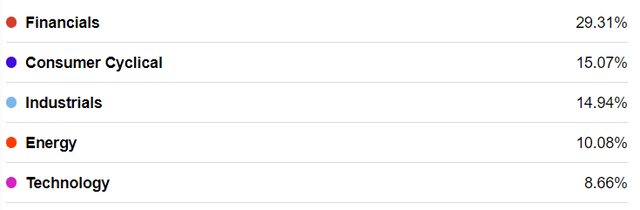

There is also concentration risk here as almost one third of the portfolio is in companies operating in the Financials sector:

Seeking Alpha

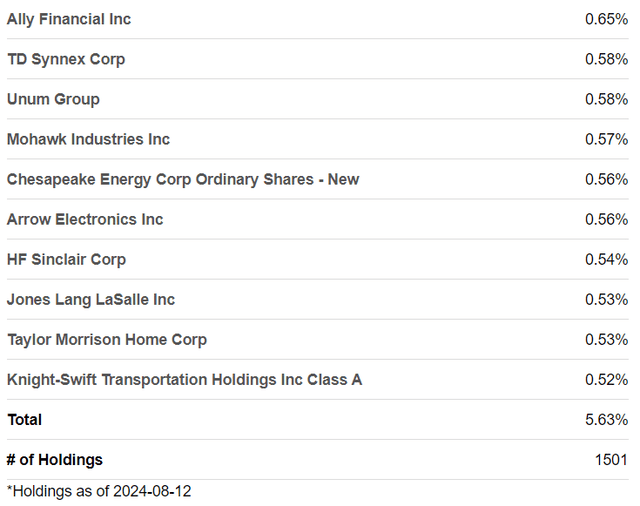

To be fair, I’ll have to note that this doesn’t represent DFAT’s risk management efforts well as the highest weighted holding is currently 0.65% of the portfolio and the 10 top holdings represent 5.63%:

Seeking Alpha

Verdict

All in all, this is one of the few instances that an active fund is worth considering not only as a strategic tilt but also as a long-term option for exposure in the equity market. The expense ratio is very low for active management, and the track record is consistent with the accumulating evidence that value outperforms in the long run. Thus, I am rating DFAT a strong buy.

What do you think? Do you prefer some other value ETF or are you staying away from value-bias approaches in general? Let me know below. Thank you for reading!

GIPHY App Key not set. Please check settings