nzphotonz

Let’s try to take a look at Trump Media & Technology Group Corp (NASDAQ:DJT) stock out of the context of my (or your) opinion on the 45th. U.S. President. It’ll be difficult, but isolating DJT from its founder is key to understanding the growth prospects of the stock, which has generated a lot of buzz here on Seeking Alpha after the SEC approved Trump Media’s merger with SPAC Digital World in mid-February 2024.

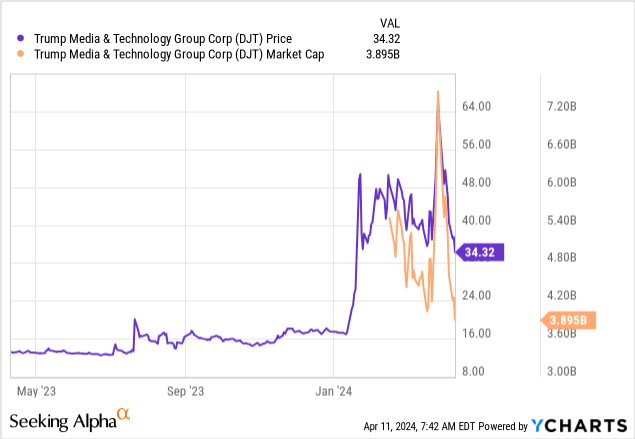

Since then, as expected, the stock has shown very high volatility: At one point, its market capitalization was over $7 billion, but by today, as the hype surrounding DJT died down, its market capitalization has fallen to ~$3.9 billion:

Data by YCharts

Data by YCharts

What exactly do investors pay such huge amounts of money for?

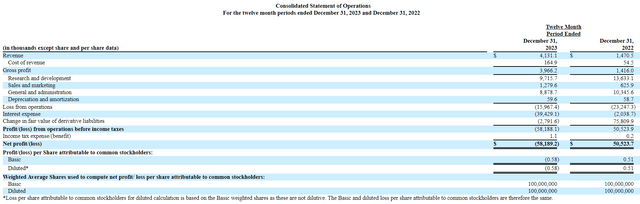

Trump Media increased its sales by 180% compared to the previous year, but in absolute terms, sales amounted to only $4.1 million. I wasn’t wrong: the ~$4 billion company only generated $4.1 million in the 2023 financial year. Already at this point, any debate of the company’s current valuation is proving untenable: DJT seems ridiculously overvalued to me. But what immediately strikes me when I first analyze DJT’s income statement is that the management itself doesn’t seem to see any sense in the company’s future development. I draw this conclusion from the decline in R&D expenditure by more than 30% YoY. At the same time, interest expense exceeded revenue by 8.5x in FY2023 – the first time I have seen the stock grow by 278.70% YoY with such indicators.

SEC, DJT’s recent 10-K

Organizing a digital business like Truth Social – DJT’s most important asset at the moment – requires huge investments in research and development that have not been made so far. One might think that this will change in 2024, as the company now has much more scope for flexible management thanks to its listing on the largest stock exchanges. Nevertheless, I realize that these opportunities for the company will only come through dilution – not a good thing for those who want to hold DJT shares for more than a few trading days.

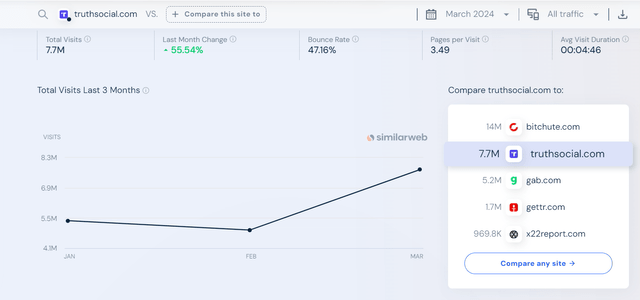

If you look at the visitor numbers for Truth Social on SimilarWeb, it looks at first glance as if the website is growing quite rapidly: last month it recorded a 55.5% increase in total visits. On closer inspection, however, you can see that this metric fell from January to February and the main growth took place in March. I attribute this to the fact that DJT’s website was in the public eye due to all the news that the company received permission from the SEC. That said, it’s unlikely to be a real influx of live users – I think these are just people who happened to come to the site, or analysts like myself who have tried to study DJT’s product.

SimilarWeb, Truth Social

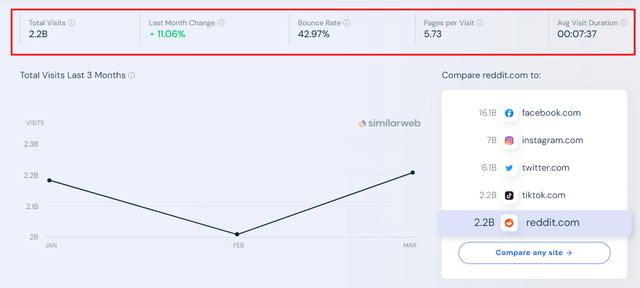

Pay attention to how many pages the user views during a visit and how long an average visit takes: 3.49 pages/visit and 4 minutes and 46 seconds, respectively. Just compare that to Reddit (RDDT), which also recently became a full-fledged public company, only through a classic IPO:

SimilarWeb, Reddit

Traffic is also down from January to February, but a) RDDT’s traffic exceeds Truth Social’s by a factor of ~285, and b) average page visits are significantly better in terms of the time spent on the site and the number of pages visited. Furthermore, RDDT’s market capitalization is only 1.75 times that of Truth Social.

My fundamental analysis tells me that DJT could be worth $206 million at best if we assume that sales increase 5x this year and we use a price-to-sales ratio of 10x (that’s a 48% premium to RDDT’s forwarding multiple). This means that the fundamental downside potential in terms of valuation is 94.7% of the current DJT price.

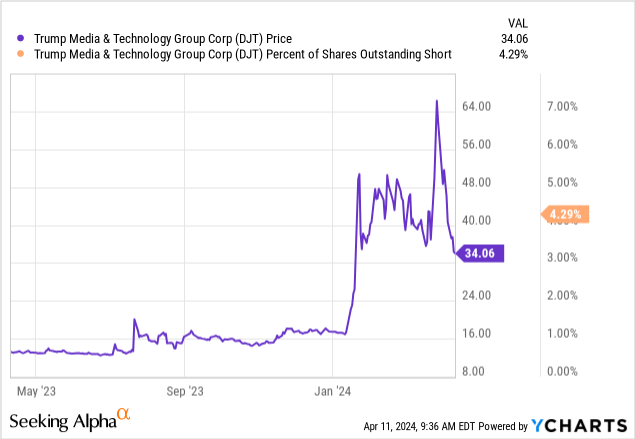

At the same time, I don’t see much sense in hoping for a short squeeze with a short interest of 4.29% as of today. That is why, even speculatively, DJT stock does not look like the best pick, in my opinion.

Data by YCharts

Data by YCharts

So to summarize my article today, let me state that DJT has nothing outstanding if we disregard the entire political context surrounding this stock. The company’s business prospects are dubious because its unit economic metrics are poor (compared to its closest competitors like Reddit), it lacks R&D focus and there’s simply too much competition in the social networking market. At the same time, DJT stock is priced to perfection – at certain moments, in comparison to RDDT or in comparison to the sales volumes, I was amazed. My relatively optimistic valuation findings suggest a downside potential of ~94.7% compared to the current stock price – not including possible dilution.

Based on the sum of all the factors analyzed, I feel compelled to issue a “Sell” rating today.

Thanks for reading!

GIPHY App Key not set. Please check settings