Klaus Vedfelt/DigitalVision via Getty Images

In keeping with my continued coverage on bonds and bond funds, I thought to have a quick look at each of the major fixed-income asset classes. Doing so helped me understand how things stand in the market right now, and hopefully will help investors in the same way.

Bonds Overview

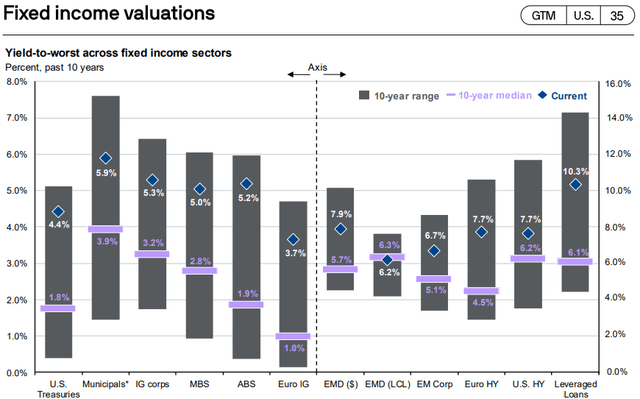

In general terms, almost all bonds and bond sub-asset classes trade with good, above-average yields right now. Due to this, bonds are a broadly attractive asset class and a broad buy. There are some differences between bond sub-asset classes though, which impact their relative attractiveness. Per data from JPMorgan (NYSE: JPM), take special note of the spread between current and historical yields for the different bond sub-asset classes.

JPMorgan Guide to the Markets

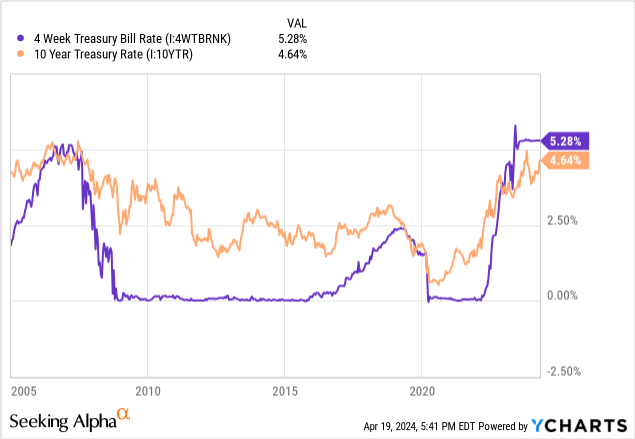

T-Bills

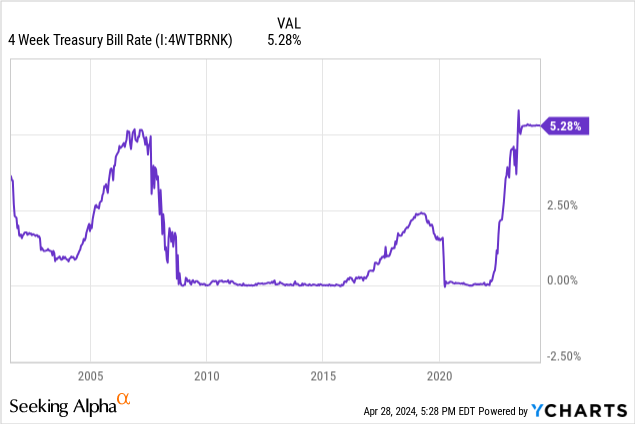

T-bills currently yield 5.3%, a good yield on an absolute basis, highest since the 90s.

Data by YCharts

Data by YCharts

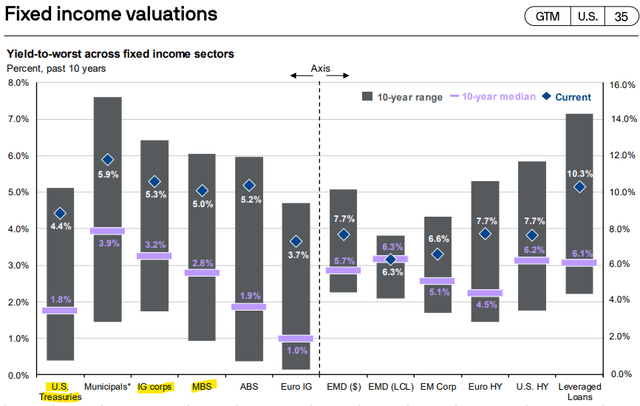

T-bills yield more than most fixed-income assets with roughly comparable credit risk, including treasuries, investment-grade bonds, and mortgage-backed securities.

JPMorgan Guide to the Markets

This is because investors expect the Federal Reserve to start cutting rates in the coming months and are pricing bonds accordingly. As per Fed guidance, and at current prevailing rates, t-bills should continue to yield more than these other asset classes for around a year.

JPMorgan Guide to the Markets

In my opinion, and considering the above, t-bills remain fantastic short-term investment opportunities, although treasuries should outperform long-term. This is not as obvious or common as it sounds. T-bills rarely yield more than longer-term treasuries, the current situation is uncommon, and a significant short-term positive for t-bills.

Data by YCharts

Investors looking for t-bill investments should consider an investment in the Alpha Architect 1-3 Month Box ETF (BATS: BOXX). BOXX has almost identical, marginally higher, returns to t-bills, with some potential tax advantages. I last covered BOXX here.

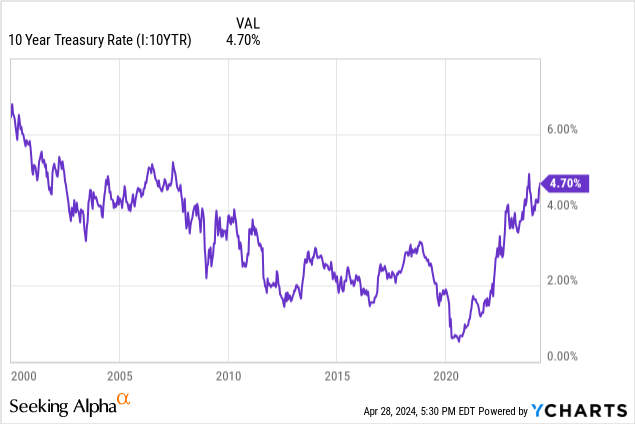

Treasuries

Benchmark 10y treasuries currently yield 4.7%, highest since the 2000s.

Data by YCharts

Data by YCharts

Treasuries yield a bit less than investment-grade bonds and MBS, assets of roughly comparable credit risk in my view, although treasury yields have risen by more.

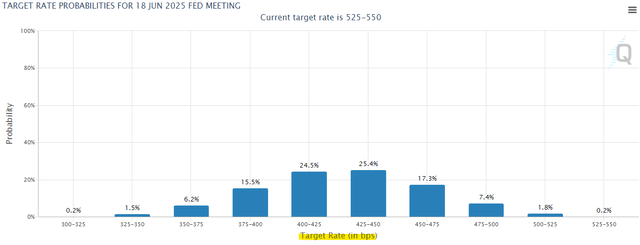

Treasury prices might increase if the Fed cuts rates, which seem exceedingly likely. Any such price gains are dependent on the magnitude and speed of any rate cuts, and of broader investor sentiment / expectations. As the market expects some cuts already, smaller, more methodical rate cuts might have limited impact on treasury prices. As an example, future markets currently expect around 4 – 5 rate cuts by mid-2025. I would not expect significant treasury price movements from fewer than 4 cuts by then.

CME FedWatch

Notwithstanding the above, significant, swift rate cuts would almost certainly lead to treasuries outperforming. Dovish market sentiment would have a similar effect, although that is much more difficult to predict.

In my opinion, treasuries are reasonably good investment opportunities right now due to their reasonably good long-term yields. I’m not expecting significant price gains from rate cuts, however.

I’ve yet to find a particularly strong treasury fund, which somewhat reduces the practical attractiveness of this asset class. As an example, treasuries should yield more than t-bills in a year or two, but BOXX could continue to provide higher after-tax yields for much longer.

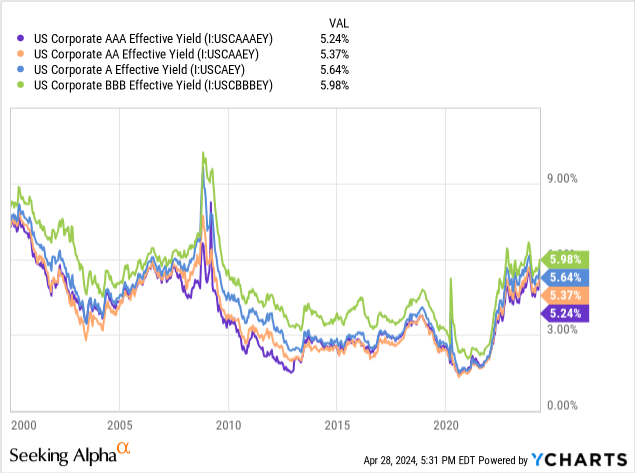

Investment-Grade Bonds

Investment-grade bonds currently yield 5.3% – 6.0%, highest since the 2000s. As per JPM, the average rate is 5.3%, but that figure is a few weeks old, and does not consider a recent spike in rates.

Data by YCharts

Data by YCharts

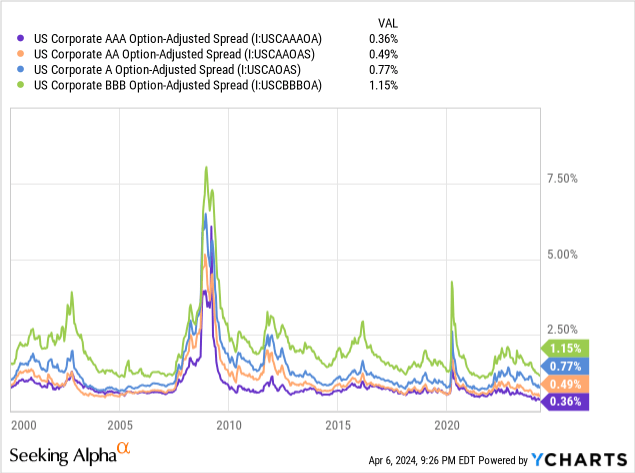

Spreads have narrowed, reaching their lowest levels in decades.

Data by YCharts

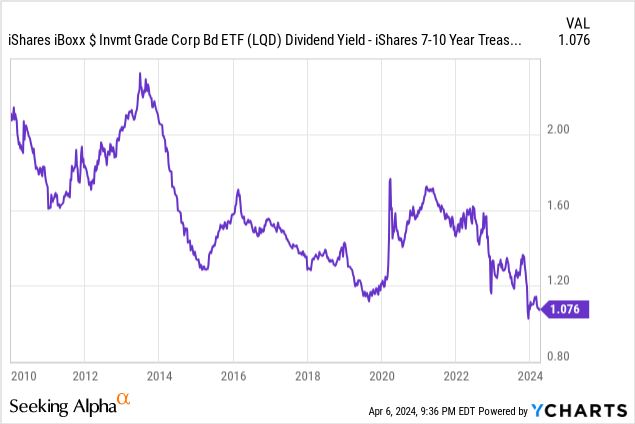

Tighter spreads are also apparent on investment-grade and treasury ETFs.

Data by YCharts

Investment-grade bonds continue to offer higher yields than treasuries, although risk-adjusted yields and expected returns seem weaker.

In my opinion, investment-grade bonds remain reasonable investment opportunities, although perhaps focusing on treasuries is simpler, and less risky too.

As is the case with treasuries, I’ve yet to find a particularly strong investment-grade bond ETF. The Angel Oak Income ETF (NYSEARCA: CARY) is a good choice, with an above-average 6.2% yield and good returns. I last covered CARY here.

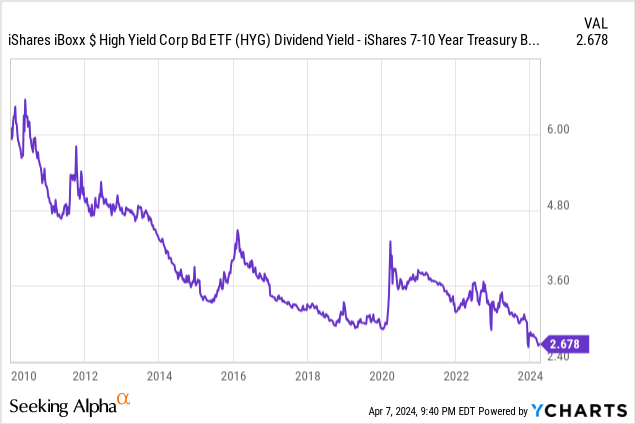

High-Yield Bonds

High-yield bonds currently yield around 7.7%, higher than in prior years, but less overwhelmingly so than treasuries or investment-grade bonds.

Data by YCharts

Data by YCharts

To expand on the above, high-yield bond rates are currently about 1.5% higher than their 10y averages, compared to 2.6% for treasuries and 2.1% for investment-grade bonds.

JPMorgan Guide to the Markets

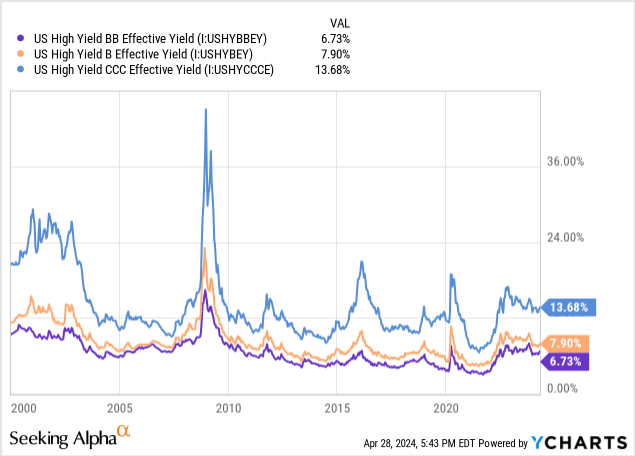

High-yield bond yields have risen by less than average as credit spreads have narrowed.

Data by YCharts

Data by YCharts

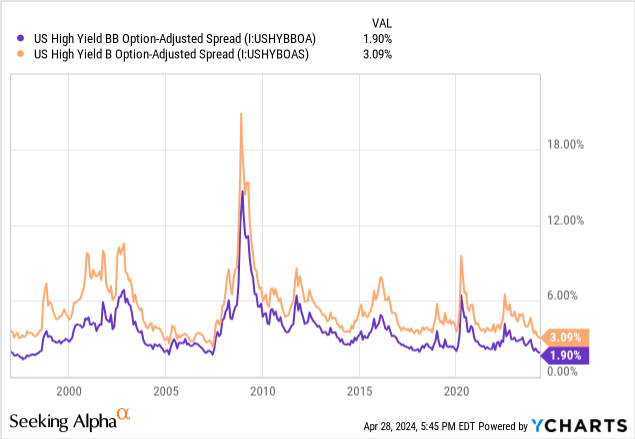

Tighter spreads are also apparent on high-yield bond and treasury ETFs.

Data by YCharts

In my opinion, high-yield bonds remain reasonable investment opportunities, due to their above-average yields. Nevertheless, spreads are much tighter than average, so treasuries present a more compelling risk-return profile.

Senior Loans

Senior loans currently yield 10.3%, around 4.2% more than 10y historical averages, and higher than most other asset classes.

JPMorgan Guide to the Markets

As is the case with t-bills, senior loan yields are particularly compelling right now as investors expect interest rate cuts in the coming months. In my opinion, and considering current market conditions and Fed guidance, senior loan yields will remain competitive for a few more years, at the least.

Specifically, senior loans currently yield around 2.6% more than high-yield bonds. Under current Fed guidance, rates would only drop +2.5% after 2027, so senior loan yields would remain attractive until that time.

Considering the above, I believe that senior loans are strong investment opportunities, and buys.

The Invesco Senior Loan ETF (NYSEARCA: BKLN) and the SPDR Blackstone Senior Loan ETF (SRLN), both with 8.8% yields, are two reasonably good funds in this space. Both are quite pricey though, with an expense ratio of 0.65% for BKLN, 0.70% for SRLN. ETFs focusing on CLO debt tranches are broadly similar, somewhat superior, choices.

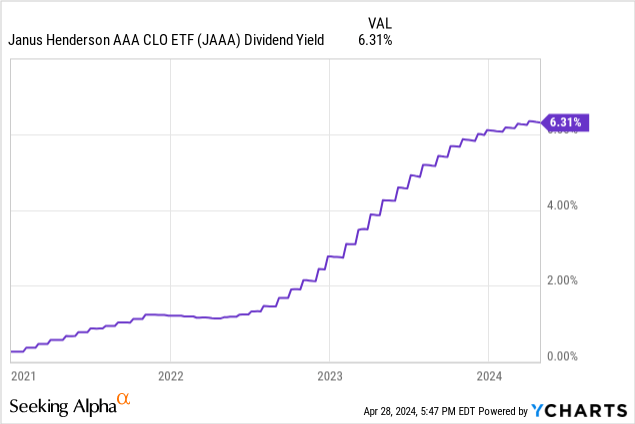

CLO Debt Tranches

CLO debt tranches are something of a niche investment, but a particularly strong one that deserves mention.

Interest rates on CLO debt tranches have risen by a lot these past few years. Although specific figures are not readily available, rates should have risen by more or less 5.25%, in-line with Fed rate hikes. The Janus Henderson AAA CLO ETF’s (NYSEARCA: JAAA) yield has risen by more or less that much, in-line with expectations. Other CLO ETFs are younger, so there is either no data, or unclear data.

Data by YCharts

Data by YCharts

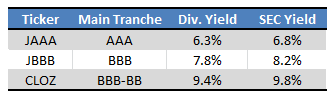

Dividend and SEC yields for three of the larger CLO ETFs are as follows:

Fund Filings – Table by Author

As is the case for t-bills and senior loans, CLO ETFs should see declining dividends as the Fed cuts rates. In my opinion, and considering current conditions, rates should remain competitive for a few years.

As an example, JAAA currently sports a 6.8% SEC yield, around 2.5% higher than treasuries. Current Fed guidance is for +2.5% in cuts by 2027 at the earliest, so JAAA’s yield should remain competitive for a few years.

In my opinion, CLO ETFs have some of the strongest, most well-rounded risk-return profiles in fixed-income markets right now, and are buys.

Municipal Bonds

Municipal bonds currently yield 5.9% on average, around 2.0% more than historical averages.

JPMorgan Guide to the Markets

From the above, yields have risen by a normal amount, slightly less than treasuries, slightly more than high-yield bonds.

The tax advantages of these bonds increases as their yields rise. As an example, avoiding a 35% tax rate on munis yielding 3.9%, their historical average, means saving 1.4% in taxes. Avoiding the same tax rate on munis yielding 5.9%, their current rate, means saving 2.1% in taxes. For investors in higher tax brackets, munis offer particularly compelling after-tax yields right now.

I’ve been unable to find a particularly strong muni bond ETF, which somewhat detracts from their value proposition. In most cases, CLO debt ETFs provide higher after-tax yields. The VanEck High Yield Muni ETF (BATS: HYD) is one of the better muni bond ETFs, with a 4.2% yield.

Dollar-Denominated Emerging Market Bonds

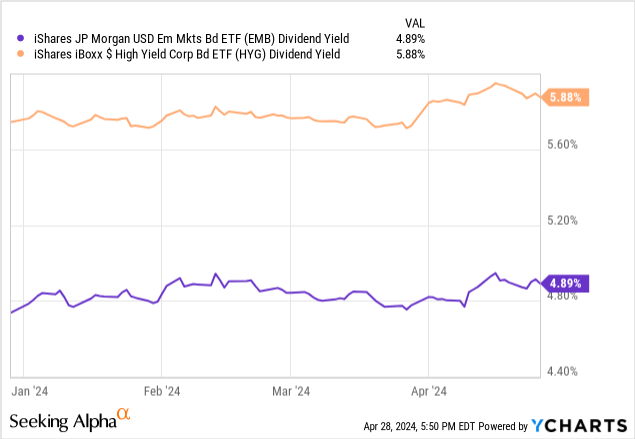

For these bonds, yields have risen by around 2.2%, from 5.7% to 7.9%. These bonds offer the highest fixed-rate yields in the market, second-highest overall behind senior loans.

These securities seem somewhat compelling relative to peers, in the data above at least. When looking at specific ETFs, the situation seems a bit different. As an example, the iShares J.P. Morgan USD Emerging Markets Bond ETF (NASDAQ: EMB), the largest fund for these securities, only yields 4.8%, less than high-yield bonds.

Data by YCharts

Data by YCharts

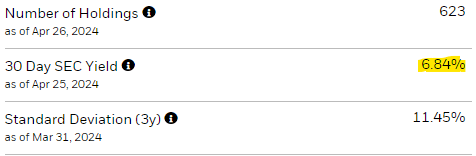

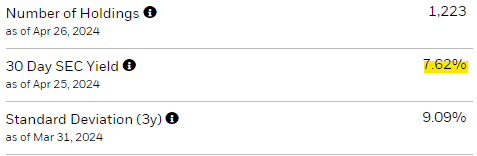

SEC yields are also lower. Compare emerging market bonds:

EMB

with high-yield:

HYG

So, dollar-denominated emerging market bonds seem stronger than most as an asset class, but the actual investment funds available to investors seems a bit weaker. I would personally focus on high-yield bonds in this situation, although it will depend on the specific fund selected.

Conclusion

Bond dividend yields are quite high right now, across sub-asset classes. Yields on short-term and variable rate securities look particularly strong, due to rate cut expectations. Treasuries also look quite compelling right now, due to tightening credit spreads. In my opinion, bonds are a broad buy right now, with CLO debt ETFs offering particularly compelling yields.

GIPHY App Key not set. Please check settings