seb_ra/iStock via Getty Images

“Politics is the art of looking for trouble, finding it everywhere, diagnosing it incorrectly and applying the wrong remedies.” – Groucho Marx

To My Partners and Friends:

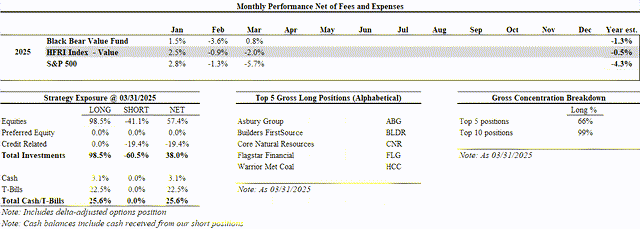

Black Bear Value Fund, LP (the “Fund”) returned +0.8% in March and -1.3% year-to-date. The S&P 500 returned -5.7% in March and -4.3% year-to-date. The HFRI Index returned -2.0% in March and -0.5% year-to-date. We do not seek to mimic the returns of the S&P 500 and there will be variances in our performance.

Note: Additional historical performance can be found on our tear-sheet.

Extreme volatility has re-entered the stock market. It is curious when portfolio managers decry a volatile market, as it is generally the most fertile setup to find interesting investments. While it is too soon to have any firm tariff conclusions, I have been re-examining our portfolio to sanity check our investments amid a range of outcomes. In anticipation of the tariff announcements, we sold some businesses that would provide a “good” return for the possibility of finding businesses with potential “great” returns. This decision coupled with our short portfolio has allowed us to play offense when others are in retreat and not experience as dramatic a draw-down as the broader indices (so far).

Taken at face value, tariffs will likely slow economic growth, decrease corporate confidence in decision-making, increase prices and shake up supply chains, among other consequences. While this will be an uncomfortable period, it will benefit the companies that have some combination of pricing power, healthy capital structures, staying power, low cost-advantages and capable management. It seems premature to jump to dramatic conclusions as the range of outcomes is quite wide. If you own businesses with staying power (We do) it’s an awesome opportunity to take advantage of sellers who have their hair on fire. On the flipside, the businesses we are short are subject to weak capital structures, lack of pricing power and other assorted maladies making them dramatically riskier.

Top 5 Businesses We Own (Alphabetical)

Asbury Group (ABG)

Asbury Group operates auto dealerships across the United States. The strength of the model comes from the back of the house in parts and services where more than 50% of the profits come from.

Tariffs will increase the cost of an automobile, reducing the affordability for both new and used cars (holding all else equal). Some of this will be mitigated by a highly variable component to ABG’s wage expense. Some damage may also be mitigated by increased activity in the Parts & Service division. Most dealers currently have 1-2 months of used inventory and 2-3 months of new inventory on their lots. The impact of tariffs could take some time to be felt and its uncertain if there will be tax credits/interest deductibility to lessen the pain on American consumers.

ABG should be able to earn $20-$30 in free-cash flow per share in a “normal” year. I have reduced some of my estimates given the uncertain nature of the environment. At quarter-end pricing, that implies a 9-14% annual yield.

Builders FirstSource (BLDR)

BLDR is a manufacturer and supplier of building materials with a focus on residential construction. Historically, this business was cyclical with minimal pricing power as the primary products sold were lumber and other non-value-add housing materials. Since the GFC, BLDR has focused on growing their value-add business that is now 40%+ of the topline. The company has modest leverage and has been using their abundant free-cash-flow to buy in over 45% of the stock in the last 33 months.

Our long-term thesis remains intact, as there is a structural shortage of housing in the USA. Higher mortgage rates reduce the supply of existing home supply as homeowners are locked into low-rate mortgages. As we have seen in recent history, the overall pie of housing activity may shrink, with new homebuilders capturing an increasing share of home sales. Homebuilders can buy-down the mortgage to a lower rate and accept a lower, yet still healthy, margin on the home sale.

Past letters have commented that the coming 6-12 months could be rocky, and BLDR (the stock) has not disappointed. The business continues to perform well, and management continues to reduce the share count, thereby increasing our ownership.

The company has sustained higher gross margins as they have gained scale. I estimate normalized free cash flow per share to be $10-$15 per year, implying a free-cash-flow yield of 8-12% with no growth priced in.

Core Natural Resources (CNR)

Core is the result of the merger between Consol and Arch Resources. As a combined entity, they are one of the leading producers of metallurgical coal (steel) and thermal coal (energy). The Company is heavily dependent on exports, so retaliatory tariffs would be damaging. At the same time, there has been a reduction in global capacity, so many countries may not have much choice, especially if they need higher quality coal.

Met coal demand is projected to climb for the next 25 years, driven by the economic development and urbanization in India and the rest of Southeast Asia. ~60% of the world’s population lives in Asia, where met coal demand is centered and where local sources are limited. Over the coming years demand will likely outstrip supply, leading to higher prices. There has been a severe lack of investment in met coal due to ESG concerns with investment peaking in 2014.

I will disclose my updated valuation thoughts at a later date, as I find the investment extremely compelling, and I am hoping the Company can buy back ever cheaper stock. As a reminder, this is a Company with a fortress balance sheet and is one of the cheapest producers in the market. While short-term pain hurts all Companies, they can be major long-term beneficiaries.

Warrior Met Coal (HCC)

Please reference the met coal discussion above, as it applies to Warrior Met Coal. Currently, the bulk of HCC’s FCF is being invested in a capital project that will be concluding this year. Once the business winds down their investment period, they will gush cash.

I will disclose my updated valuation at a later date. I am travelling to Alabama next week to meet with management and should learn a lot more about their prospects. This is one of the most compelling ideas in our portfolio. As a reminder, this is a Company with a fortress balance sheet and is one of the cheapest producers in the market. While short-term pain hurts all Companies, they can be major long-term beneficiaries.

Flagstar Financial (FLG)

Flagstar Financial is the former New York Community Bank (a mashup of Flagstar Bank, New York Community Bank and assets from Signature Bank). Like our SHORT investments in Silicon Valley Bank and First Republic, FLG had a hole in their balance sheet (from soured multifamily and office real estate vs. long-duration securities). That is where the similarities end.

FLG raised over $1BB in additional capital, led by former Treasury Secretary Steven Mnuchin. They revamped the management team and brought in a superstar CEO in Joseph Otting who successfully turned around OneWest Bank post GFC (formerly known as IndyMac Bank). In 12 months, the management team has accomplished more than most teams can do in 2+ years. They have reviewed nearly all the loans on the books, sold off non-core assets raising additional capital and are focused on delivering a narrowly-focused, well-capitalized boring regional bank. In this case, boring is good. Importantly, they have taken a conservative view of their loan book and a large credit reserve. This contrasts with several bank/private credit lenders we are short who have taken minimal reserves. Mr. Otting and his team are my kind of managers – they are plain-spoken, hardworking and plan for the worst while hoping for the best.

At quarter-end, the bank was trading at ~67% of a conservatively marked balance sheet. This is in contrast with similar banks (who are NOT conservatively marked) trading at 140-160% of their tangible book value. FLG should complete working thru the bulk of their issues by the end of 2025 and approach “normal” during 2026. Given the conservative nature of the management team, I wouldn’t be surprised if it happened sooner. At these prices the downside seems minimal and could see this business up 50-150% over the next 1-3 years as it is more appropriately valued.

Concluding Thoughts

It is often the most uncomfortable environments that provide the best opportunities. The fog of uncertainty causes many to hide and wait for the “all-clear”. If you have been contemplating adding or joining our Partnership, this is an attractive time. If you are contemplating adding capital, please make sure you have a multi-year horizon in mind, as that is the nature of our Partnership.

Our edge comes from an ability to look out further than most and ride out the short-term roller coaster of momentum and negative investor psychology. When we look back at our portfolio a year from now, I think we’ll be pleased with the fundamental performance of our businesses, despite an uneasy macroeconomic environment. I also think we’ll see our management teams taking aggressive actions to both manage the businesses appropriately as well as allocate capital in a shareholder-friendly manner.

While it is an extremely hectic news environment, these are the kinds of climates that are the most fun. We know what we own and are sober/objective in our reasoning and will stand to do well in the coming years. Please reach out if the Fund is of further interest.

Thank you for your trust and support.

Black Bear Value Partners, LP

THIS DOCUMENT IS NOT AN OFFER OF, OR THE SOLICITATION OF AN OFFER TO BUY, INTERESTS IN BLACK BEAR VALUE PARTNERS, LP (THE “FUND”). AN OFFERING OF INTERESTS WILL BE MADE ONLY BY MEANS OF THE FUND’S CONFIDENTIAL PRIVATE OFFERING MEMORANDUM (THE “MEMORANDUM”) AND ONLY TO SOPHISTICATED INVESTORS IN JURISDICTIONS WHERE PERMITTED BY LAW.

This document is confidential and for sole use of the recipient. It is intended for informational purposes only and should be used only by sophisticated investors who are knowledgeable of the risks involved. No portion of this material may be reproduced, copied, distributed, modified or made available to others without the express written consent of Black Bear Value Partners, LP (“Black Bear”). This material is not meant as a general guide to investing, or as a source of any specific investment recommendation, and makes no implied or express recommendations concerning the matter in which any accounts should or would be handled.

The returns listed in this letter reflect the unaudited and estimated returns for the Fund for the periods stated herein and are net of fees and expenses, unless stated otherwise. Black Bear currently pays certain fund expenses, but may, at any time, in its sole discretion, charge such expenses to the Fund.

Please note that net returns presented reflect the returns of the Fund assuming an investor “since inception,” with no subsequent capital contributions or withdrawals. You should understand that these returns are not necessarily reflective of your net returns in the Fund, and you should follow-up with Black Bear if you have any questions about the returns presented herein.

An investment in the Fund is speculative and involves a high degree of risk. Black Bear is a newly formed entity with limited operating history and employs certain trading techniques, such as short selling and the use of leverage, which may increase the risk of investment loss. As a result, the Fund’s performance may be volatile, and an investor could lose all or a substantial amount of his or her investment. There can be no assurances that the Fund will have a return on invested capital similar to the returns of other accounts managed by Adam Schwartz due to differences in investment policies, economic conditions, regulatory climate, portfolio size, leverage and expenses. Past performance is not a guarantee of, and is not necessarily indicative of, future results. The Fund’s investment program involves substantial risk, including the loss of principal, and no assurance can be given that the Fund’s investment objectives will be achieved.

The Fund will also have substantial limitations on investors’ ability to withdraw or transfer their interests therein, and no secondary market for the Fund’s interests exists or is expected to develop. Finally, the Fund’s fees and expenses may offset trading profits. All of these risks, and other important risks, are described in detail in the Fund’s Memorandum. Prospective investors are strongly urged to review the Memorandum carefully and consult with their own financial, legal and tax advisers before investing.

The development of an investment strategy, portfolio construction guidelines and risk management techniques for the Fund is an ongoing process. The strategies, techniques and methods described herein will therefore be modified by Black Bear from time to time and over time. Nothing in this presentation shall in any way be deemed to limit the strategies, techniques, methods or processes which Black Bear may adopt for the Fund, the factors that Black Bear may take into account in analyzing investments for the Fund or the securities in which the Fund may invest. Depending on conditions and trends in securities markets and the economy generally, Black Bear may pursue other objectives, or employ other strategies, techniques, methods or processes and/or invest in different types of securities, in each case, that it considers appropriate and in the best interest of the Fund without notice to, or the consent of, investors.

Performance returns compared against benchmark indices are provided to allow for certain comparisons of Black Bear’s performance to that of well-known and widely-recognized indices. Such information is included to show the general trend in the markets during the periods indicated and is not intended to imply that the holdings of any of the applicable accounts were similar to an index, either in composition or risk profile. The indices represented herein are the S&P 500 and the HFRI EH: Fundamental Value Index (“HFRI EH FVI”). The S&P 500 is a free-float weighted/capitalization-weighted stock market equity index maintained by S&P Dow Jones Indices, which tracks the performance of 500 large companies listed on

U.S. stock exchanges. The HFRI EH FVI reflects fundamental value strategies which employ investment processes designed to identify attractive opportunities in securities of companies which trade a valuation metrics by which the manager determines them to be inexpensive and undervalued when compared with relevant benchmarks.

This presentation contains certain forward-looking statements. Such statements are subject to a number of assumptions, risks and uncertainties which may cause actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by these forward-looking statements and projections. Prospective investors are cautioned not to invest based on these forward-looking statements.

Furthermore, many statements in this presentation are the subjective views of Black Bear, and other reasonable persons may have differing views. Unless it is unequivocally a statement of fact, any statement herein (even if not specifically qualified as an opinion (i.e., with language such as “in the opinion of” or “we believe that”)) should nevertheless be understood and interpreted as an opinion with which reasonable persons may disagree, and not as a material statement of fact that can be clearly substantiated.

The information in this presentation is current as of the date listed on the cover page and is subject to change or amendment. The delivery of this presentation at any time does not imply that the information contained herein is correct at any time subsequent to such date.

Certain information contained herein has been supplied to Black Bear by outside sources. While Black Bear believes such sources are reliable, it cannot guarantee the accuracy or completeness of any such information.

This Presentation has not been approved by the U.S. Securities and Exchange Commission (the “SEC”) or any other regulatory authority or securities commission.

This Presentation does not constitute an offer of interests in the Fund to investors domiciled or with a registered office in the European Economic Area (“EEA”). None of the Fund, Black Bear or any of their respective affiliates currently intends to engage in any marketing (as defined in the Alternative Investment Fund Managers Directive) in the EEA with respect to interests in the Fund. Receipt of this investor presentation by an EEA investor is solely in response to a request for information about the Fund which was initiated by such investor. Any other receipt of this investor presentation is in error and the recipient thereof shall immediately return to the Fund, or destroy, this investor presentation without any use, dissemination, distribution or copying of the information set forth herein.

Click to enlarge

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

GIPHY App Key not set. Please check settings