Thomas Barwick/DigitalVision via Getty Images

Hutchmed logo (Hutchmed)

Investment Thesis

In our article on HUTCHMED (China) Limited (NASDAQ:HCM) on the 26th of March this year, we continued our Buy stance on the back of our expectations that the company finally is becoming profitable.

The share price is up nearly 20%.

HCM’s colon cancer drug FRUZAQLA’s approval by the U.S. FDA at the end of last year was a game-changer for the company with a reported good uptake from U.S. patients after the launch.

We believe the growth rate of 59% in sales of oncology products in FH 2024 will continue on the back of expected approvals from Japan and the E.U. Sales in China, and potentially India will also add to the growth going forward.

Let us start by looking at their latest financial results, which came out on the 31st of July 2024.

HCM made a profit of $25.8 million in FH 2024, with revenue from sales of products up 64% to $128 million. Their full-year revenue guidance remains at $300 million to $400 million.

On the cost side, the R&D costs decreased from $144.6 million in FH 2023 to $95 in FH 2024. However, this does not mean that R&D will receive less priority going forward. It is expected to grow going forward.

The net income attributable to HCM’s shareholders in FH 2024 was $0.03 per ordinary share, which equates to $0.15 per ADS, as one ADS consists of 5 ordinary shares.

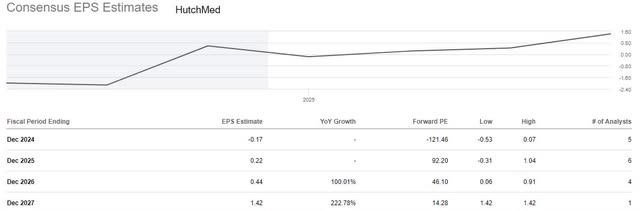

Analysts on Wall Street are, in our opinion, too conservative in their projections about future earnings.

Wall Street analysts consensus on Hutchmed’s forward earning projections (SA)

Their negative EPS estimate of $-0.17 per ADS, we assume, must have been made before the positive EPS of $0.15 communicated by management during the FH 2024 presentation.

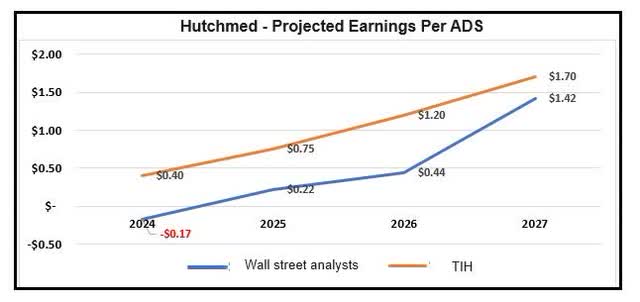

Tudor Invest Holding’s projection of earnings per ADS versus Wall St. (Data from SA and TIH)

Our estimate for SH 2024 EPS is $0.25 per ADS. This makes the FY 2024 EPS $0.40. In 2025, we could see a further growth of about 80% to 90%, assuming regulatory approvals in the various European countries, plus Japan come through. This is the catalyst that will boost sales further.

Now to their balance sheet.

As of the end of FH 2024, they held $802.4 million in cash and cash equivalent assets. Bank borrowings were only $82.1 million.

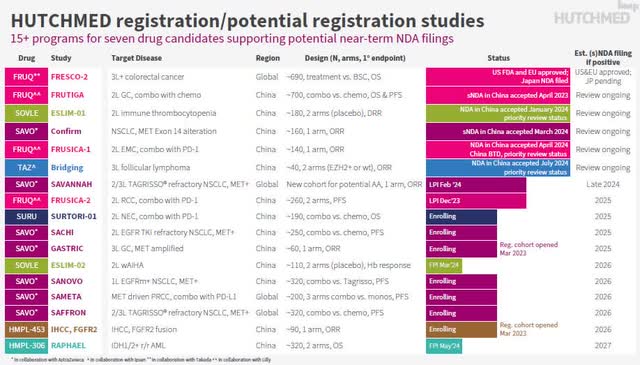

We will be interested to learn more about their capital allocation going forward. Much of the profit will in all likelihood be directed towards the pipeline of new products they have under development.

Hutchmed’s pipeline of products under development (Hutchmed FH 2024 Results Presentation)

Risks to Thesis

There are many areas of risk associated with companies in the pharmaceutical industry.

It is costly to develop and bring medicine to the market.

We have also pointed out in earlier articles on HCM that governments in many countries regulate how much they can charge for the medicine. This can be a risk as it may reduce profitability.

Many industries face challenges from trade barriers. Especially those located in China. However, it is likely if HCM can develop medicine that treats life-threatening illnesses, such as cancers, most countries would not put too many barriers to trade in these.

Conclusion

We do believe in the growth story of HCM. Even if it would not completely cure millions of patients, if it can improve their condition, it seems to me that it should be applauded.

Early investors in HCM must have patience.

It may never become as big as Novo Nordisk (NVO), which has a market capitalization of$576 billion, but HCM’s market capitalization is only $3.4 billion.

It has products that the world needs. It is manufacturing in China, which still is the world’s largest manufacturing nation.

Management of HCM has outlined the future growth and their focus on controlling costs. This was also highlighted at the earnings call with analysts by their CEO, Dr. Wei-Guo Su:

Our previous target was to achieve profitability by the end of 2025. We believe, we are well on our way and potentially ahead of the curve. Looking ahead, there are a lot of events on this map, all lined up for 2025 2026, and beyond. These events if achieved, will help fuel the growth for years to come”

We maintain our Buy stance.

GIPHY App Key not set. Please check settings