guvendemir

Kraft Heinz (NASDAQ:KHC) needs no introduction, they are owners of a collection of iconic packaged food brands such as Heinz Ketchup, Philadelphia Cream Cheese and Kraft Mac & Cheese. Many of us have grown up with these brands and continue stocking up on them during our weekly grocery runs, no matter what. After all, we still have to eat.

Traditionally this business has been practically risk-free and investors loved it. Nobody made fortunes out of it, but if you were looking for a reliable way to protect your retirement savings from inflation while earning some profit on top, consumer stapes was the go-to sector.

Things changed when grocers started stocking their own private-label products. First, these were seen as poor-quality, low-cost alternatives that most shoppers were not least tempted to add to their baskets. Gradually, the quality, acceptance and sales of private labels have grown. In 2023 private labels have reached a record 18% share of Fast Moving Consumable Goods sales.

Kraft Heinz is having to wrestle with changing consumer preferences and its business is not as certain any more. Having said that, the company is still very profitable and has a lot of control over its cost base. It is now focussing its marketing and innovation efforts on core category-leading brands, such as Heinz and Philadelphia, to expand its product portfolio in the areas of strength and reconnect with customers.

We see KHC as an attractive opportunity for yield-seeking investors, as growth in core product categories as well as continuing cost-cutting efforts should enable the business to grow its already attractive Free Cash Flow yield at a rate of inflation, or even above.

The Recent Performance

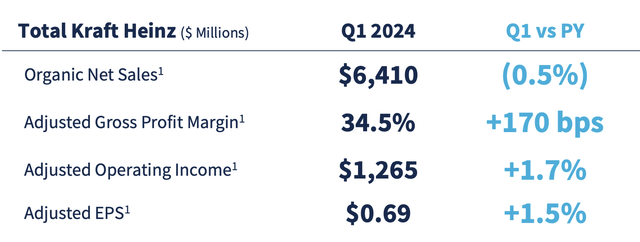

Kraft Heinz reported its Q1 FY2024 results, a few weeks back. The company is continuing to display a stagnant top line as pricing increases are being offset by sales volume losses. Gross margins, on the other hand, were increasing due to cost-cutting efforts.

KHC Investor Relations Presentation

Earnings growth has lagged behind the gross profit improvement as KHC has considerably increased spending on marketing, technology, and Research & Development. The company has ended the quarter with a ~20% operating profit margin.

For the full year, Kraft Heinz expects to return to positive sales growth as volumes are expected to turn positive in the H2. Volume performance in the Q1 US was also weighted down by a reduction in SNAP benefits, with comparable numbers lapping in H2.

KHC Investor Relations Presentation

In our analysis, we prefer to take a long-term fundamental view of the businesses we cover. We are long-term buy-and-hold investors and therefore prefer to get a clear sense of the headwinds and the tailwinds that the business is facing and square these off against the valuation. So let’s take a look into the drivers of the future earnings growth of the business

The Growth of Private Labels

Private labels is the largest challenge that Kraft Heinz is facing. Quite a few structural and shorter-term factors have boosted the sales of private labels. We believe that these trends are likely to continue, albeit at a rather gradual pace. The impact is not uniform across product categories though. Brands like Coca-Cola (KO) have fared rather well, while some other categories, such as dairy, have been practically taken over by private labels.

Most recently inflation was to blame for the growing market share of private Abels, as many cash-strapped consumers had no choice but to opt for the cheapest alternatives. As wage increases continue outstripping general inflation, the purchasing power of consumers should eventually recover, enabling many to continue buying their favourite brands. Having said this, it’s quite clear that private label sales will not go down to zero even as purchasing power recovers. Structural longer-term trends are driving the growth of this market segment.

With stagnant American population growth and a rather stable average per-person calorie intake, significant growth in the private label segment means that the market for the brands is contracting. This suggests that sales of consumer staples brands are no longer likely to keep up with inflation as sales volume trends are negative.

Cost Cutting and Strategic Re-Focus

To counteract these developments KHC and its industry peers have to engage in cost-cutting to maintain profit margins in an inflationary environment. The branded staples manufacturers do have a lot of areas to get cost savings from, such as product formulation, factory consolidation and investments in more efficient machinery. As long as volumes decline at a slow gradual pace, branded food manufacturers can take a lot of free cash flow out of the business as it shrinks.

The problems surface if the decline accelerates as then expensive broad-reaching restructuring and redundancy programs have to be implemented. Rapid restructuring can be expensive and the cash that is spent on optimisation cannot be paid out to shareholders. Restructuring, if done incorrectly, can further accelerate the decline. We prefer to stay away from rapid volume decline situations as these can be very risky, especially when significant levels of financial leverage are involved.

ALAMY

Kraft Heinz, 5-7 years ago, was one of these situations we would rather avoid. Initially 3G Capital had a brilliant profit-making idea of embracing the unavoidable gradual decline of mass-market brands, and instead of fighting it, just slashed costs aggressively and bled the businesses for cash. Many of these brands have enjoyed dominant positions for years and generated great profits and presumably have built up some excess costs in the organisations. Assuming that the price paid for the acquisition was not too high and that the restructuring would be effective, good returns could be made even on the acquisitions of the business in decline.

The Kraft acquisition, though was a big mistake. 3G and Buffett have paid too much and leveraged the combined group irresponsibly. To keep the creditors off their backs, the management had to slash costs particularly aggressively. They pushed too hard and businesses started cracking at the seams, losing consumers rapidly. It became apparent that KHC had too much debt and cut costs too deep. The company had to slam on the breaks.

From about 2020, Kraft Heinz has started switching gears. Core organic growth areas were chosen and non-core businesses started being divested to strengthen the balance sheet. It took some time as soul-searching as a corporate culture reset is never easy. Overall, since the Kraft-Heinz merger of 2015, the company’s stock is down more than 50 per cent, while the S&P 500 has increased 2.5x over the same period. It has been a terrible stock to own.

Having said that, it appears that the business is finally turning a corner, as the profit margins have started recovering from the lows seen during FY2022 and the balance has also been repaired now, with debts down by $10 billion from the peak. Most importantly the business has found a new strategic direction. The company is no longer engaged in aggressive cost-cutting across its portfolio and instead is investing in product innovation and marketing in its strongest product categories. We believe these efforts could be successful due to the strength and international appeal of the Heinz brand.

The Playbook of Coke

One very significant factor contributing to the declining appeal of mass-market packaged goods brands was the changing media landscape. The declining popularity of mass media channels such as TV, radio and newspapers has made it increasingly difficult for mass-market brands to reach their audiences cost-effectively.

In the old days, category-leading brands could reach a large share of the population through a single channel, leveraging their marketing spending over the largest revenue base. The biggest mass-market brands could reach a large share of the population with a relatively low marketing-to-sales ratio. These days are now over as media distribution channels have been fragmented and it is a lot more expensive to achieve the same broad reach. Most mass-market brands can no longer reach mass audiences, and the reduced engagement with customers leads to the continuing weakening of their goodwill and pricing power.

Not all brands are the same. Coca-Cola (KO) is a good example of a strong mass-market brand that has stayed resilient, and could also provide others in the industry a roadmap on how to navigate this changing landscape. We see two main factors contributing to the continuing success of KO.

Number one, it’s the high sales per single brand name. We can think about this in simple terms, the brands that are likely to continue affording advertising during the Super Bowl will be a lot more resilient. One interesting aspect of KO is that its core brand has branched out just as the marketing channels were fragmenting. The sales of the Coke brand have continued going up as new drinks continued being added to the umbrella, thus preserving some of the marketing efficiency. The advertising cost to reach the mass market has increased, but so has the sales of Coke brands, thus lowering the marketing-to-sales ratios whilst keeping the same reach.

Number two, it’s the unrelenting focus on marketing and innovation over many decades. Coke has never had an intention to run the business for cash and has continued furiously defending its position through innovative marketing and product innovation. These years of well-directed marketing effort do add up and the product itself has evolved with the changing consumer preferences. Diet and Cherry Cokes, for example, now are significant contributors to sales and customers weary of “full-fat” Coke can try out new flavours from their favourite company. Innovation keeps the brand fresh and consumers engaged. It also makes the job of the “advertising men” a lot less difficult. We could bet you that if KO was still generating most of its sales from Coca-Cola Classic, it would be facing significant competition from private labels.

Coca-Cola Inc.

Not all of the mass market FMCG brands can follow the playbook of KO. A lot of the brands do not have the revenue base or the margins to afford to reach mass audiences. Many have also given up on marketing and innovation many years ago, doing irreparable damage to their brands. A lot of the brands of the past will have to be run down for cash and there is nothing wrong with that. The pricing power of many brands will decline very gradually, especially given the distribution power that consumer staples groups have, enabling the owners to take a lot of cash out in the process. Some brands though can continue staying relevant, even in the changing markets.

In The Footsteps of Coke

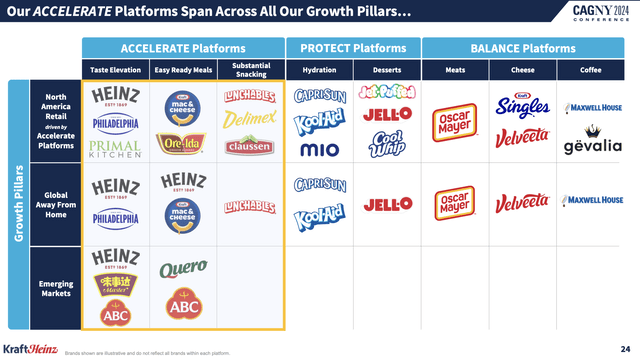

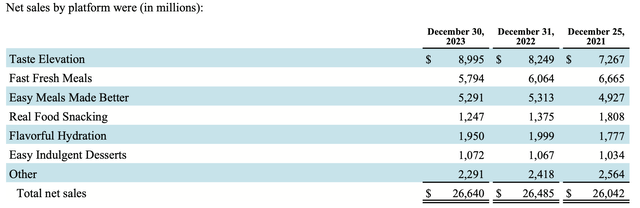

Kraft Heinz, like many of the consumer staples groups, has a mixed bag of different brands, some are strong while others are weak. The company separates its brands into three different baskets. The “Accelerate” platform, which currently accounts for 61% of sales, contains the strongest brands such as Heinz, Philadelphia Cream Cheese and Mac & Cheese. Kraft Heinz intends to focus its marketing and innovation efforts on the brands within “accelerate” while running down “protect” at a gradual pace. The “Balance” brands seem to be open for offers and will likely decline quite rapidly, they account for about 20% of group sales but have rather low gross margins.

KHC Investor Presentation

We see “Taste Elevation”, which accounts for 34% of sales as the strongest segment of the group. Heinz is unquestionably the strongest brand of the group as it has a large scale and an international appeal, while Philadelphia remains strong in its small niche. Unsurprisingly, this segment has been the best performer for the group in terms of sales growth, delivering a ~25% uplift in sales over the last two years.

KHC Annual Report

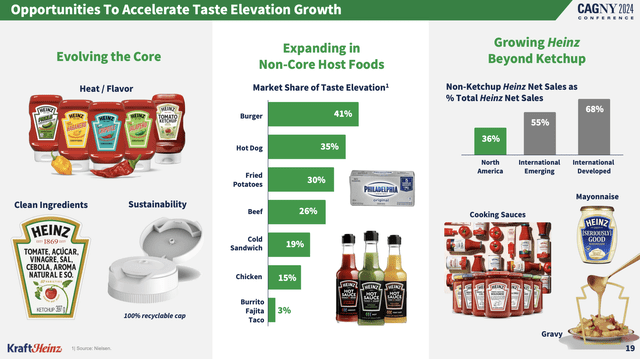

The most significant contributors to the growth of Heinz sales were a brand extension, increasing foodservice market share and also growing international sales. We expect Heinz to continue performing well on the back of continuing product innovation as the growing product umbrella is also making the marketing efforts more efficient. It would seem that Heinz has borrowed the playbook of Coke and that’s definitely a good thing.

Heinz is branching beyond its classic ketchup and introducing different varieties of its core product. On top of this, it is entering entirely new condiment categories with new products such as Heinz-branded hot sauces. Within core ketchup, Heinz is rolling out reduced sugar and sodium sauces as well as introducing new flavours, such as “Habanero”. We see this as a very similar strategy to Coca-Cola introducing Diet Coke, Cherry Coke and others.

KHC Investor Presentation

We are unsure if Heinz is as strong of a brand as Coke, but initial results are encouraging as consumers are buying the new versions of Heinz. Inflation was a factor over the last couple of years, but even accounting for pricing the revenue performance looks encouraging as volumes must have grown even as prices were raised. So far Heinz is performing well and should continue adding sales on the back of its innovation efforts.

The Yield We Expect from Kraft Heinz

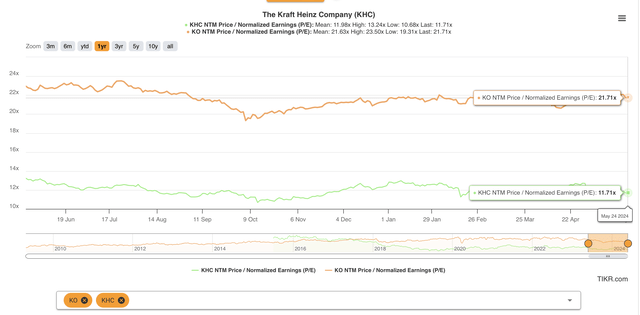

KHC is starting to follow the playbook of Coke and the results are encouraging, but we should not assume that Kraft Heinz is the new KO as “Taste Elevation”, the strongest category of the group, only accounts for 34% of sales. KO trades at a significantly higher PE valuation multiple, and probably deserves it. The 12X PE valuation of KHC, on the other hand, is not demanding at all.

TIKR

KHC does have a couple of strong brands, that will grow most likely, but the majority of group sales still come from rather weak product categories where private labels will continue gaining share. The company does have cost-cutting in its DNA and we believe can continue producing attractive free cash flows even as volumes in most of the product categories decline. KHC is not a growth company, it is rather a yield play and should be judged accordingly.

We should also take into consideration the low-risk nature as well as the free cash flow generation potential of the consumer staples industry. We believe that investors purchasing the stock at free cash flow yields exceeding 7% are likely to realise returns greater than those offered by investment-grade corporate bonds, even under rather adverse market development scenarios.

At the time of writing this, investment-grade corporate bonds are yielding 5.7% YTM on average, as per “ICE BofA BBB US Corporate Index”. During FY2023, KHC has generated ~$3 billion of free cash flow, with the current market cap at $44 billion, KHC trades at a 6.8% FCF yield. Free Cash Flow is a rough measure of the cash the business would be able to return if no growth initiatives or acquisitions were pursued.

Of the $3 billion generated, last year the company allocated $2 billion to dividends and this year plans to initiate a share buyback program. Combining the dividend yield as well as buyback-driven EPS growth, the business is likely to generate shareholder returns close to the FCF yield. KHC is likely to produce returns exceeding the corporate bond yields.

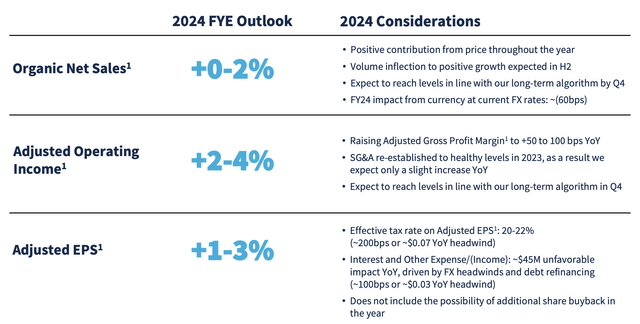

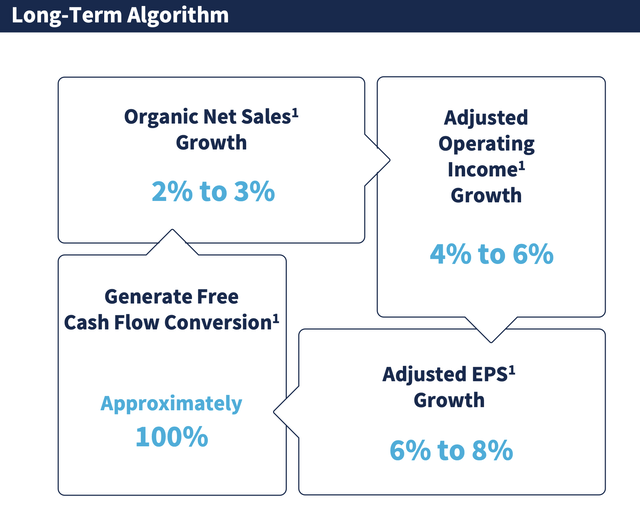

In the best-case scenario, it is also possible that the business will keep cutting costs effectively and that the “Accelerate” platform sales volume growth will offset declines in other categories. If the group revenues can grow in line with, or just below inflation, while the cost base growth lags inflation, the earnings of the business are likely to grow with inflation, or even above it as margins expand. KHC management targets an organic earnings growth of over 6%, nominal.

KHC Investor Presentation

Under this scenario, shareholders would earn returns considerably greater than the ones offered by corporate bonds. We leave these assumptions for the best-case scenario as many things need to come together operationally for the business to achieve an earnings growth rate exceeding inflation. Volumes in “Accelerate” will have to grow and cost-cutting has to be gradual and sustainable. Some of the benefits of the cost-cutting will have to be re-invested back into marketing and innovation to enable volume growth while keeping operating margins stable.

The Bottom Line

The consumer staples industry has been under pressure from declining customer loyalty as many have started opting for lower-priced, private-label alternatives. This trend has been fostered by the structural change in the media landscape and is likely to continue. Kraft Heinz as well as its industry peers will have to adapt to the changes.

Cost cutting is one of the ways how the industry responded. Branded food companies in most product categories have a lot of control over the cost base and can take a lot of cash out provided that the volume declines are quite gradual.

Some brands though, have been more resilient than others. Coca-Cola has managed to stay relevant by innovating and expanding its product portfolio, Kraft Heinz is now also following these footsteps with its core Heinz brand.

KHC is not combining an offensive go-to-market strategy in its core product areas with continuing cost-cutting efforts in weaker categories. We believe that this strategy is likely to yield attractive risk-adjusted returns for holders of the stock. This is not a growth opportunity but should provide an attractive yield over an extended period.

Risks

Accelerating market share gains of private label products. This could be driven by continuing high inflation and a reduction in the disposable incomes of consumers. Accelerating a decline in the “Balance” product categories could reduce the cash generation of the business and its ability to maintain the current dividend yield. Innovation and marketing efforts could not achieve the desired results, leading to profit margin and free cash flow reduction.

Source link

GIPHY App Key not set. Please check settings