ahmet ihsan ariturk

Thesis

When I first wrote about Safe Bulkers (NYSE:SB) in January 2023, my thesis had four pillars.

Shipping rates should improve, given the restricted supply and muted demand. SB was cheap relative to the sector, and its valuation might re-rate closer to peer valuations. SB’s efficient fleet set them up to generate profits above industry norms and navigate a changing regulatory environment. Management’s capital allocation fits my investing profile (smaller dividend, larger reinvestment).

Since my article, SB has significantly outperformed a collection of peers on a price appreciation and total return basis, with only Golden Ocean coming in close. Shareholders have achieved a total return of 89%, or 59% annualised.

SB and a peer group’s total stock return since Jan 2023 (Seeking Alpha)

As for my assumptions:

The forward-looking demand/balance setup has weakened a little, with demand likely to strengthen relative to supply in 2024 but weaken in 2025. It’s not a bad set-up still, but it’s not as promising as it was in early 2023. SB remains undervalued for seemingly unjustified reasons. I’m no longer expecting a valuation re-rate, given it hasn’t to date. Nonetheless, SB’s earnings are cheap compared to the sector. SB’s efficient fleet continues to out-margin peers. We’ve seen fleet expansion and stock repurchases. Management continues to impress.

If you want to invest in the dry-bulk sector, SB still seems the best value and highest-quality company. That said, the sector is less attractive to me now, so I am reducing my recommendation from a strong buy to a buy.

Introduction

SB is a dry bulk vessel owner with diversified vessel sizes. They are growing fast and have a further 7 vessels on the order book.

As of December 2023, our fleet of 45 dry bulk vessels consisted of 9 Panamax, 11 Kamsarmax, 17 Post-Panamax and 8 Capesize class vessels… and an aggregate carrying capacity of 4.8 million dwt. (Company website)

In this article, I will discuss the four key pillars of my thesis and how they have changed since early 2023. I’ll compare SB to a random assortment of dry bulk peers, including Golden Ocean Group (GOGL), Star Bulk Carriers (SBLK), Genco Shipping (GNK), Eurodry (EDRY), Pangaea Logistics Solutions (PANL) and Diana Shipping (DSX).

Pillar 1: Shipping Rates

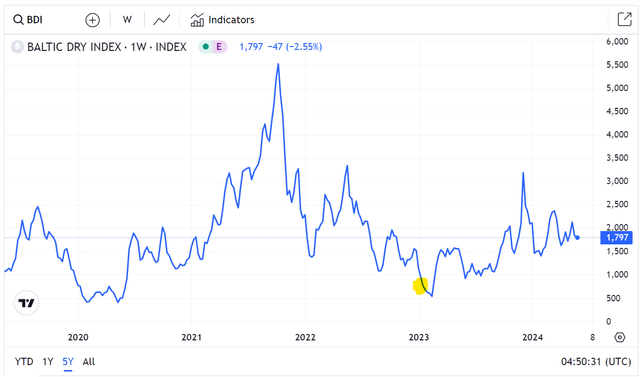

Dry bulk shipping rates have increased 143% since January 2023, when they were at historic lows of 740. The current rates are more in line with historical averages.

Batlic Dry Index chart (TradingView)

Long asset lives and lead times cause dry bulk supply to change slowly. In contrast, global demand for dry bulk commodities (e.g., oil, coal, grains, steel, etc.) fluctuates, and available transportation routes change.

Supply

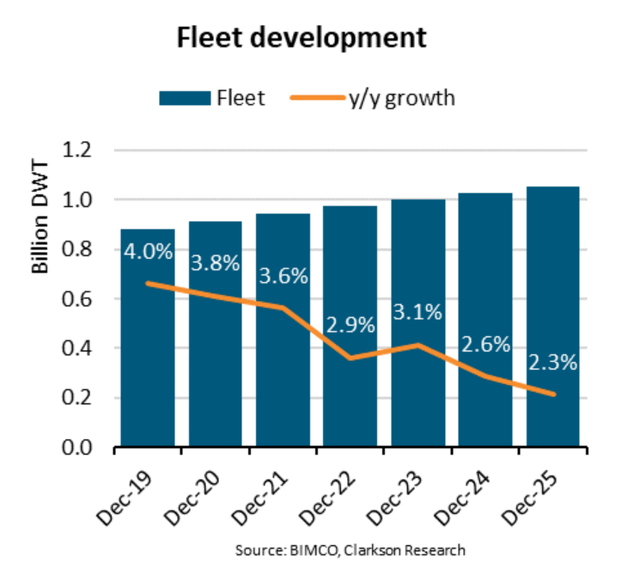

Change in supply is driven by new deliveries, vessels scrapped, and global cruise speeds. In January 2023, the order book had dipped to 7%. According to BIMCO, this has now risen to 8.8%. However, over half will be delivered after 2025. The current recycling/scrapping rate has been low but will likely increase in 2024/5 as delivery volumes increase. Finally, sailing speeds are expected to reduce by up to 1%, incentivised by fuel efficiency improvements and regulations. All factors considered, supply is forecasted to remain relatively constrained for the next year and a half at least, dropping below 3% this year (BIMCO).

Dry bulk fleet supply historic changes and forecast (BIMCO report 2024, Q1)

Panamax and Supramax have relatively large portions of the order book (BIMCO). SB doesn’t have Supramax’s, which is a positive, but it does have Panamax’s, so the supply there would increase faster.

A panel of dry-bulk CEOs at the International Shipping Forum stated that they were purposefully under-ordering due to the uncertainties around required technologies and fuel types for upcoming regulations; they wanted to prevent “regret orders”. Additionally, they stated that production slots with deliveries pre-2027/28 are hard to find as they are taken by tankers and container ships.

Demand

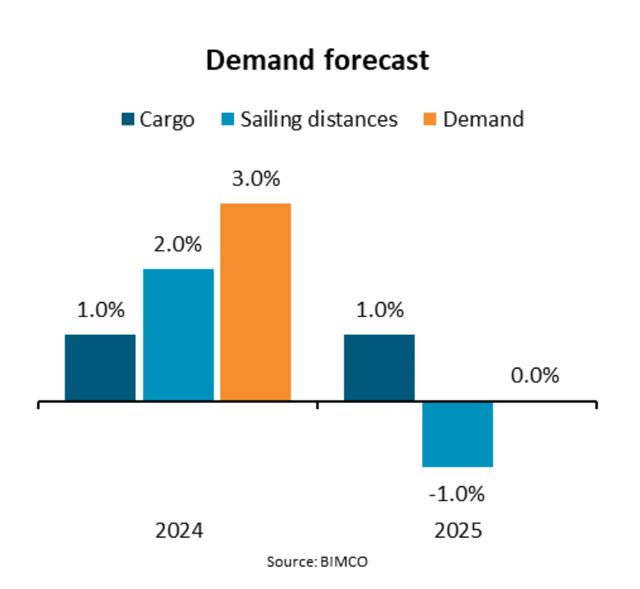

Demand is highly unpredictable due to numerous influencing factors. However, I’ll discuss two factors that could surprise demand forecasts.

China has a disproportionate share of dry bulk demand. This demand has been suppressed, especially due to the housing market’s woes, and it seems the consensus is pessimistic about its recovery near-term. However, the Chinese recovery in Q1 was better than expected, and the Chinese government is attempting to stimulate the housing market. If the recovery continues to exceed expectations, dry bulk demand forecasts would have to rise.

Disruptions in the Panama Canal and the Suez Canal increase demand as dry bulk vessels reroute to longer routes. For the Panama Canal, El Nino water levels are expected to normalise in H2; the Red Sea situation is expected to be resolved in a similar timeframe (BIMCO). Since these forecasts assume these key routes to normalise during H2, any delays would increase demand forecasts.

Dry bulk fleet demand historic changes and forecast (BIMCO report 2024 Q1)

Supply & Demand Balance

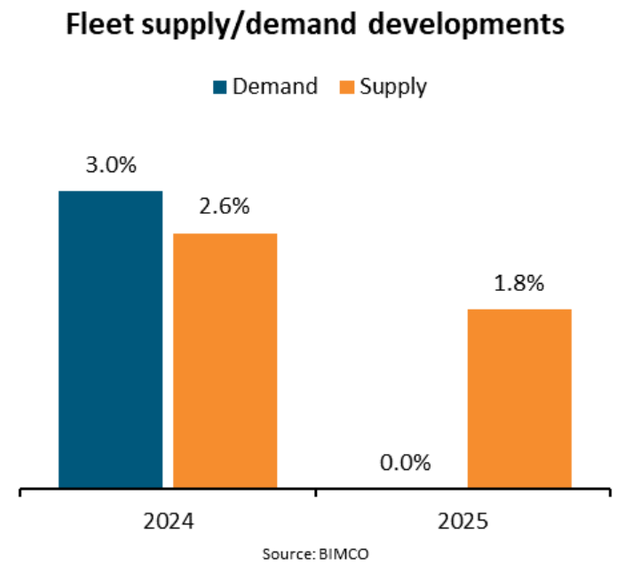

According to the BIMCO report, supply is expected to increase relative to demand in 2024 and decrease in 2025.

Dry bulk fleet supply/demand historic changes and forecast (BIMCO report 2024 Q1)

Back in early 2023, it was easy to guess that rates should go up. I feel it is much more uncertain now. That said, it was interesting to hear how practically every CEO on the International Shipping Forum panel in March had chosen to keep pricing attached to the indices rather than lock in rates. They felt that rates had further to go up and wanted to lock in charters at higher rates. That was back when rates were over 2200, compared to 1800 today. It remains to be seen whether they were right.

While I’ve focussed on how the rates might change from here, it’s worth appreciating that current rates are very good for dry bulkers, who are collectively enjoying healthy cash generation.

Pillar 2: Relative Price

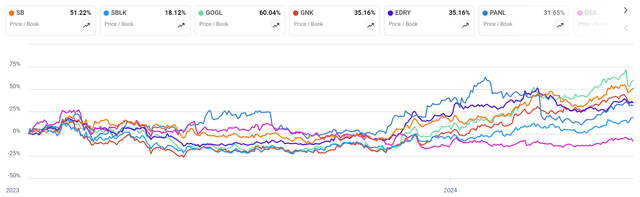

In my original article, I argued that SB was undervalued. I anticipated a valuation re-rating to align with the broader market. In a way, it did. Its price-to-book value increased the second fastest among peers. While P/B ratios are not an ideal way to measure ship owner assets, they’re an easier-to-find proxy than P/NAV. I don’t mind using it because I place limited value on it. I believe that shipping company valuations ultimately reflect their earnings and cash flows, especially when the going is good.

Price to Book relative change (Seeking Alpha)

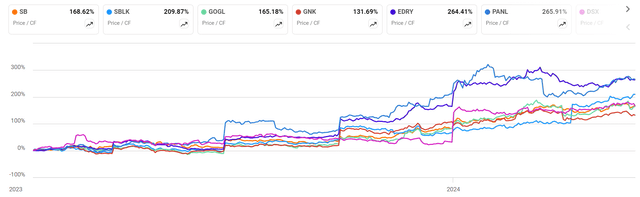

However, considering multiples for the price (and/or EV) compared to sales, gross profits, EBITDA, cash flows, and earnings, SB’s valuation grew less than average (an example of the relative change is shown below). Surprisingly SB appears to have become marginally cheaper compared to its peers.

Price to cash flow relative change (Seeking Alpha)

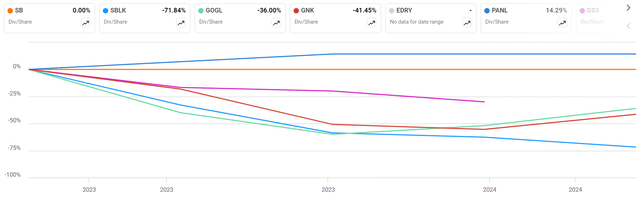

While this strikes me as strange, I see no fundamental reasons for it. I wondered if other companies might have become more attractive by increasing their dividends, but the opposite was generally true. SB held its dividend amount steady, whereas its peers mostly reduced their dividends.

Dividend per share relative change (Seeking Alpha)

I suppose perhaps the valuation is simply not keeping up with the impressive stock price growth.

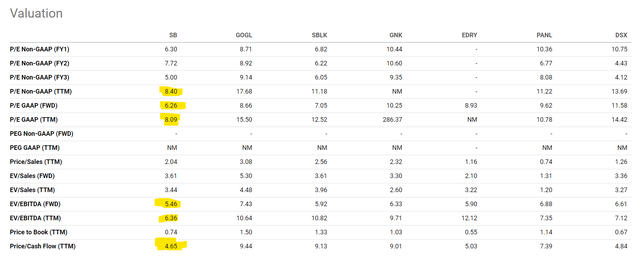

In summary, SB’s valuation remains attractive. I note it is the cheapest stock in all the highlighted metrics below.

Valuation metrics table (Seeking Alpha)

Pillar 3: Fleet Efficiency

Fleet comparison

In 2023, I stated that SB had a more environmentally efficient fleet than most but didn’t numerically compare it with the competition. Below, I analyse SB’s peer group using three factors that are knowable and improve efficiency. Other factors, such as the paint used on the hull, are also significant but not made public.

Fleet efficiency metrics (Numbers found across various company websites/filings)

SB fleet’s average age is 10 years. While this is less than Global Ocean’s impressive 8 years, it is below the average. SB also has 7 new vessel deliveries scheduled, which will help offset the wider fleet’s ageing.

In my last article, I explained the benefits of scrubbers (quote below). SB is perhaps in the middle of the pack here. However, they are actively installing more, so I expect their efficiency to improve.

Third, by the end of 2023, almost all of SB’s ships will have scrubbers installed which remove harmful exhaust gases. Scrubbers legally enable ships to run on a relatively cheap fuel with high sulphur content, dramatically reducing costs. The value of the fuel saving (known as Hi5 spread) varies significantly but is expected to average around $190+ per tonne of fuel through 2023 (which it did), which is significant (though less than the crazily high figures through 2022).

Japanese ships are known to be of superior quality, particularly for pre-2015 builds (Citi). They have longer useful economic lives and “solid bases” for improvements and upgrades. Improvements/upgrades are currently preferred over purchases due to previously mentioned uncertainties in future fuel/technology requirements for new builds. SB’s fleet is 85% Japanese-built, 4% Korean-built, and 11% Chinese-built.

SB’s fleet has the highest proportion of high-quality Japanese vessels, has a lower than average age with new vessel deliveries incoming, and has a reasonable number of scrubbers with more to be installed. On paper, SB’s fleet looks great – but how well do these factors contribute to the financials?

Efficiencies into profits

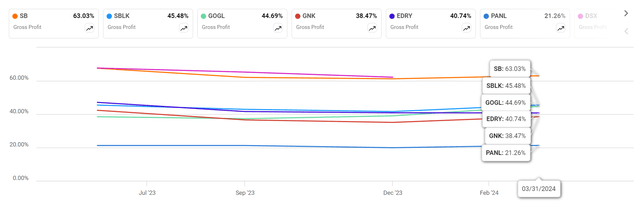

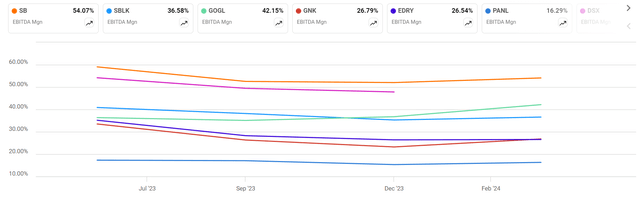

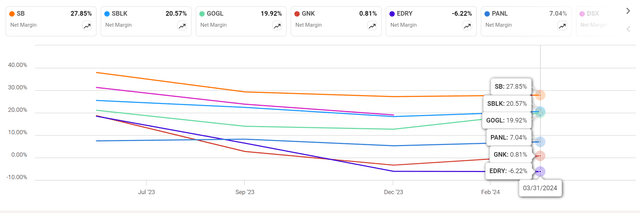

In my initial write-up, I proposed that SB’s higher margins were due to its efficient fleet. SB has successfully maintained the margin advantage over its peers.

Gross profit margin chart since Jan 2023 (Seeking Alpha)

EBITDA margin chart since Jan 2023 (Seeking Alpha)

Net margin chart since Jan 2023 (Seeking Alpha)

Note: Dry bulk shipping rates were low early in 2023, but a lot of the sector’s income was locked in at much higher rates from 2021/22. As these charters expired, margins fell across the board as seen above.

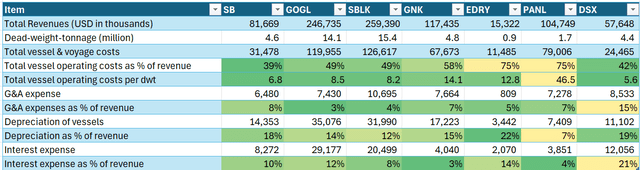

To determine the source of SB’s competitive advantage, I analysed the peer group’s income statements. The first thing I found is that SB is not able to generate revenue at a premium to other shippers. Note: PANL is an outlier due to its unique focus on “ice-class” vessels (this also applies under expenses comparison).

Revenues compared to fleet size (Numbers found across various company websites/filings)

In contrast, by examining operating expenses, I found that SB does indeed operate more efficiently than its peers. Below, I group all vessel, voyage, dry-docking, commission, and management expenses into one line item. I would have liked to have drilled down further, but with companies reporting line items in different ways and with different mixes of charter ratios, it was impossible. In any case, SB has the second lowest operating costs, but DSX’s advantage is mitigated by comparatively lower revenue for its fleet (as above).

Expenses normalised by revenue/fleet size (Numbers found across various company websites/filings)

The above table isn’t an exhaustive list of expenses, but I did compare other useful expense items. SB’s G&A expense is slightly above the average. Depreciation isn’t operationally important since it isn’t a cash item (it’s practically a way to offset taxes). I also pulled out interest expenses to get a sense of the debt burden. SB was middle of the pack here, though I will touch more on the debt later.

Pillar 4: Capital Allocation

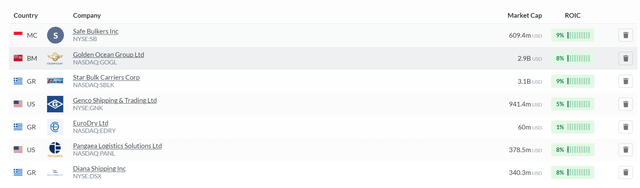

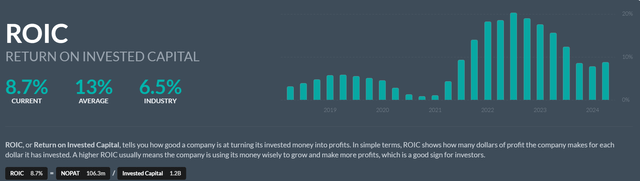

I prefer a smaller dividend and reinvestment into the company, provided the management is generating good returns. SB has a good ROIC compared to its peers, as shown below.

ROIC comparison between peers (Alpha Spread)

ROIC historical chart for SB, with industry average (Alpha Spread)

Management’s smaller dividend is shown below. Some of the payout ratios for SB’s peers would worry me.

Dividend table (Seeking Alpha)

The smaller dividend allows more cash for vessel purchases and upgrades—and we see that below in the second largest capex to operating cash flow ratio.

Cash flow chart (Seeking Alpha)

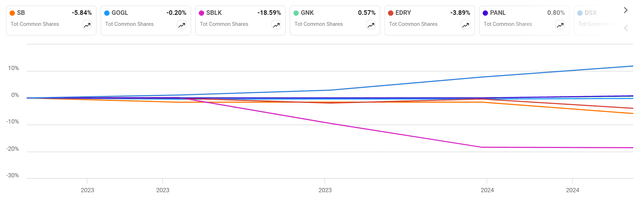

It also enables share repurchases. SBs reduced its share count by 6%, only beaten (by some margin) by Star Bulkers.

Total change in outstanding common shares chart (Seeking Alpha)

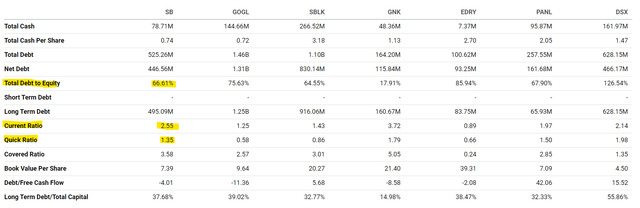

I’ll briefly note that SB is levered in a sector-typical way, as shown below. Its current ratio and quick ratio are fairly unremarkable. I also note an Altman-Z score of 1.4, again very typical for the sector. I have no real solvency concerns, though theoretically if interest rates skyrocketed long-term and the business nose-dived, the business’s financial future would look bleaker.

Balance sheet for SB peers (Seeking Alpha)

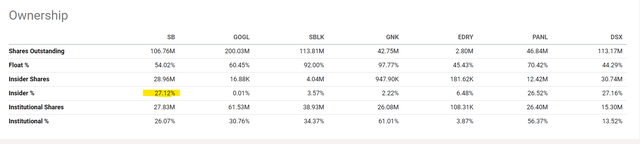

On a related point, I like that management is heavily invested in SB, though this applies equally to a few other companies.

Ownership table (Seeking Alpha)

A brief technical note

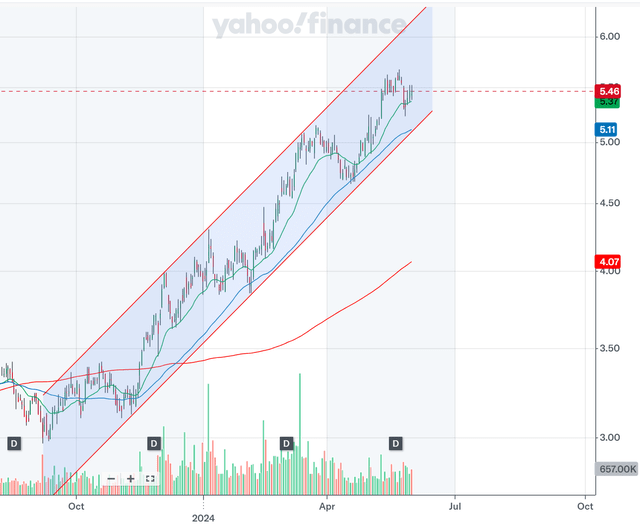

SB is in a clear uptrend and has been in a positive price channel since September last year. It has great momentum.

Price action for SB (Yahoo Finance)

Summary

SB and its stock have performed very well since my first article. SB still strikes me as the best choice in dry bulk for its relative cheapness, fleet efficiency, and capital allocation policy. Though I’m reducing this to a buy on account of the weakened sector outlook (from great to descent), I’m still optimistic about SB’s future.

GIPHY App Key not set. Please check settings