selvanegra

Thesis overview

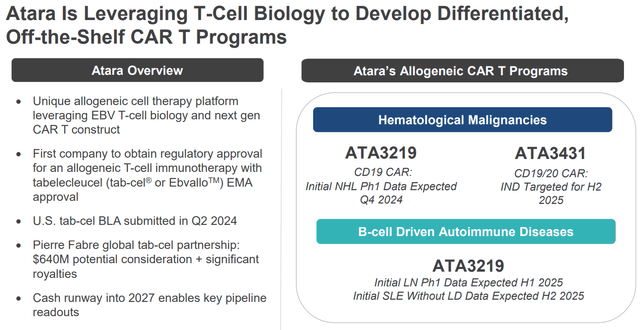

Atara Biotherapeutics (NASDAQ:ATRA) is a commercial stage biotech developing allogeneic EBV T cells for oncology and autoimmune indications. Notably, ATRA got a world-first approval of an “off-the-shelf” allogeneic T-cell therapy (tab-cel) by EMA in December 2022 and is nearing FDA approval (following considerable regulatory delays). As explained in my prior coverage, ATRA remains significantly undervalued based on tab-cel alone considering remaining regulatory ($80M) and commercial (up to $520M) milestones as well as significant double-digit royalties of potential peak US sales >$500M.

Even though I consider ATRA undervalued based on pending tab-cel milestones and future royalties, in the short/medium-term ATRA will likely have to burn all this cash in its remaining pipeline. Therefore, it is important to consider whether the pipeline is worth it. With a cash runway into 2027 (assuming tab-cel approval in 2024) I believe ATRA has enough cash to deliver first clinical data from its remaining pipeline. Even though ATRA’s assets are in the very early stages of clinical development (phase 1) there are good reasons to expect positive results. Furthermore, ATRA’s allogeneic EBV T cell-based platform appears to have important advantages over competition. The most important short-term risk is regulatory delays (either FDA not accepting the BLA submission and/or a complete response letter) which would mean the need for a cash raise to get through 2024.

Here I provide an update on tab-cel and focus on the potential of ATRA’s CAR-T therapy for autoimmune indications relevant to competition.

To sum up my thesis;

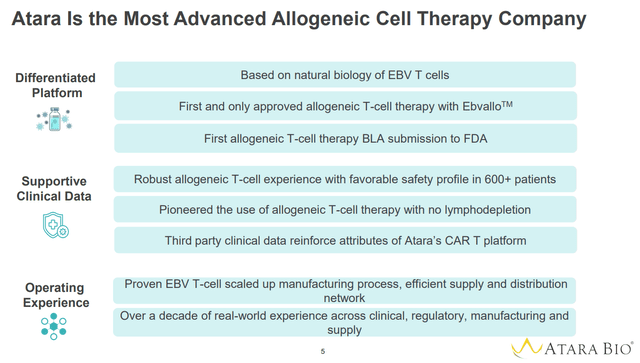

We know that CAR-T therapies work in both B-cell malignancies and B-cell-dependent autoimmune indications. Therefore we know that ATRA’s CAR-T therapy will most likely work as well. Notably, key features of ATRA’s platform (including EBV-specific T-cell receptor, use of memory phenotype, use of the 1XX costimulatory domain) have already been clinically validated by either academia or the industry. Importantly, ATRA’s platform has been validated by tab-cel approval, the world’s first allogeneic CAR-T approval. Despite fierce competition, ATRA’s CAR-T platform combines all the best attributes of its competition. Therefore, there is promising potential for commercial differentiation in the future. Assuming tab-cel approval in 2024, along with some other reasonable assumptions, ATRA’s cash runway into 2027 should be sufficient to deliver proof-of-concept clinical data for Non-Hodgkin Lymphoma (ph1 data expected Q4 2024) and SLE (ph1 data expected throughout 2025).

Summary of ATRA thesis (Company presentation)

Tab-cel update

Since my last coverage, the following has happened;

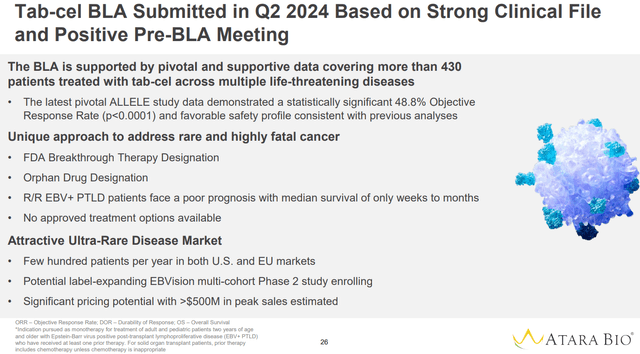

As anticipated, ATRA reported positive clinical data from the ongoing Multicohort Phase 2 EBVision Trial, supporting the label-expansion potential to other EBV-positive immunodeficiency-associated lymphoproliferative diseases. ATRA announced publication of data from the ongoing phase 3 trial in Lancet, highlighting the novelty and importance of the data. Notably, that day ATRA spiked to as high as $37 (split-adjusted price). ATRA announced BLA submission on May 20. The FDA has to decide whether the submission will be accepted within 60 days. Therefore, we should have news in July. ATRA has spent years of regulatory discussion with the FDA, and it has already been more than 2 years since tab-cel approval in Europe. Therefore, I don’t expect any surprises. Considering Breakthrough Therapy Designation, tab-cel should be eligible for a priority review, meaning a PDUFA date within 6 months of submission, i.e. October 2024. EbvalloTM (tab-cel) has been awarded the prestigious 2024 Prix Galien International Award for “Best Product for Orphan/Rare Diseases” further highlighting the scientific achievement by ATRA.

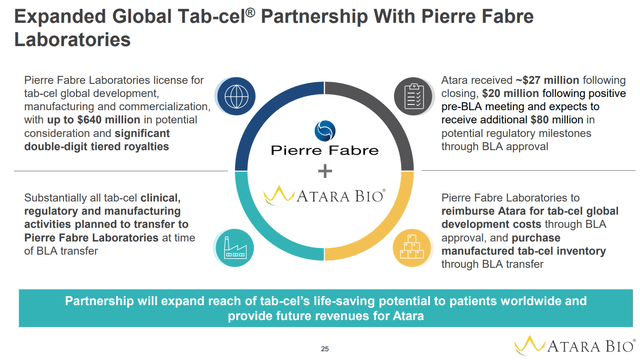

Overview of the partnership with Pierre Fabre (Company presentation)

Overview of tab-cel potential (Company presentation)

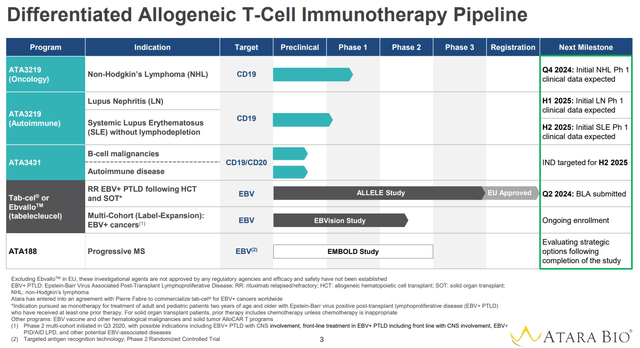

Overview of the pipeline

Beyond tab-cel ATRA is developing the following assets;

ATA3219 (a CD19-targeted allogeneic CAR-T therapy); The asset is currently been evaluated in; An ongoing ph1 study in non-Hodgkin lymphoma (NHL), with initial data expected in Q4 2024. Two planned phase 1 studies in patients with Systemic Lupus Erythematous (SLE). In the first study the treatment will be administered following lymphodepletion and initial data are expected in H1 2025. In the second study the treatment will be administered without lymphodepletion and initial data are expected in H2 2025. ATA3431, a dual CD19/CD20 CAR-T cell therapy being developed for B-cell malignancies and autoimmune indications. The asset is still in the preclinical stage with IND targeted for H2 2025. ATA188, an EBV-targeted CAR-T cell therapy. As explained in prior coverages (1, 2), despite strong scientific rationale, the treatment has failed in EMBOLD ph2 study. Interestingly, the asset is still listed in the pipeline and ATRA is evaluating strategic options. I do not consider ATA188 in my thesis, but it would be a nice surprise if there is any progress in that front, which is a scenario I wouldn’t rule out.

As will be discussed below in more detail there are very good reasons to expect that ATRA’s therapy will work fine. Additionally, there are valid reasons to expect that ATRA will be able to differentiate itself from fierce competition in the field.

ATRA’s pipeline (Company presentation)

Overview of some good reasons why ATRA is an underestimated CAR-T company (Company presentation)

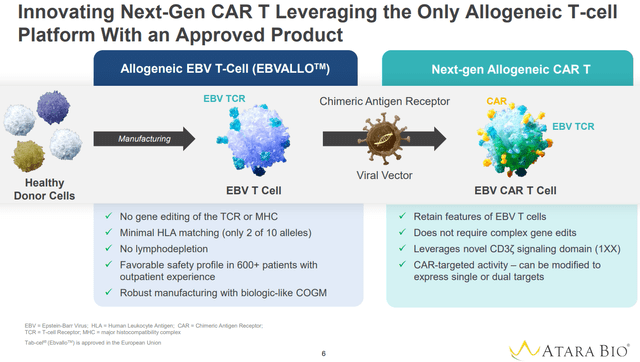

Overview of ATRA’s CAR-T platform (Company presentation)

We already know that CAR-Ts work!

There are already several FDA-approved CAR-T cell therapies in hematology (Ciltacabtagene autoleucel, Idecabtagene vicleucel, Axicabtagene ciloleucel, Brexucabtagene autoleucel, Lisocabtagene maraleuce, Tisagenlecleucel). Notably, all are autologous CAR-Ts. Tab-cel is to my knowledge the only allogeneic CAR-T approved (currently just in Europe but finally nearing FDA approval).

Beyond hematology, there are significant publications, both by academia (e.g. 1, 2, 3, 4, 5, 6) and the industry, illustrating the potential of CAR-Ts in auto-immune indications. To my knowledge, no such therapy has been approved yet, at least not in the US.

The competition in the autoimmune indications field will be discussed in a subsequent section. However, my point here is that we already know CAR-Ts work, both in hematology and auto-immune indications. So I don’t see why ATRA’s CAR-Ts won’t work as well. The big question is whether ATRA’s platform is competitive enough, which will be discussed in the sections below.

Theoretical advantages of ATRA’s platform

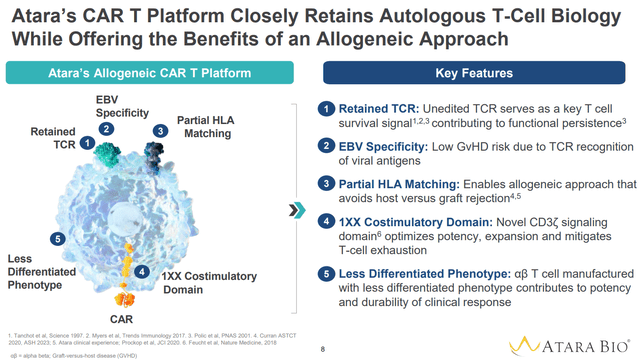

Advantages of ATRA’s platform are summarized in the images below and include the following;

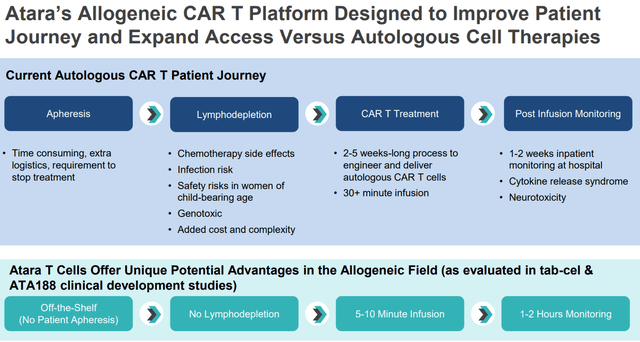

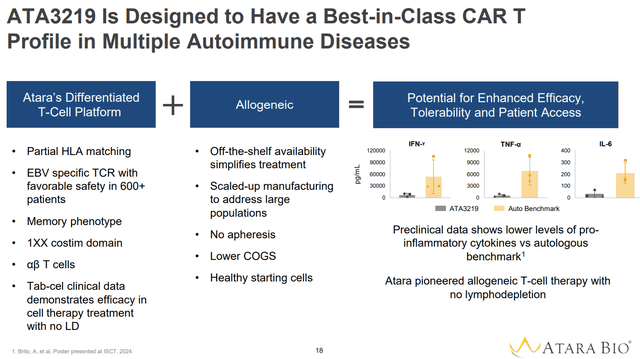

EBV specificity reduces Graft vs Host Disease (GvHD) risk due to targeting of viral antigens. This obviates the need for T-cell receptor gene editing, which improves functional persistence. Partial HLA mathing avoids host vs graft rejection and thus enables allogeneic approach. ATRA uses a less differentiated memory phenotype which contributes to potency and durability of responses. 1XX Costimulatory Domain optimizes potency and expansion, mitigates T-cell exhaustion and reduces cytokine release syndrome. All above factors combined seem to obviate the need for lymphodepletion, by allowing ATRA’s EBV CAR-T cells to expand and persist in vivo. Whether this will also work in auto-immune indications, as has clearly worked for tab-cel, remains to be seen (lymphodepletion may prove to be necessary to help “reset” the immune system and achieve durable responses in auto-immune indications).

Beyond these advantages, ATRA has already gone through lengthy discussions with the FDA to overcome regulatory hurdles (especially manufacturing-associated) associated with bringing an allogeneic cell therapy to the clinic. Therefore, ATRA is much more advanced than the competition in this regard.

“Off-the-self” available, no need for lymphodepletion and safety are major advantages of ATRA’s platform (Company presentation)

Key features of ATRA’s CAR-T platform and associated advantages (Company presentation)

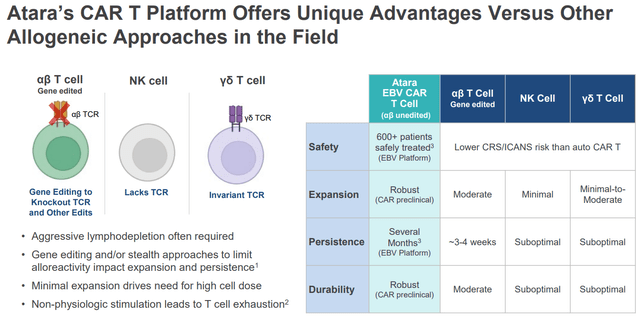

Advantages over alternative CAR-T platforms (Company presentation)

Advantages of ATRA’s platform over approved autologous CAR-T therapies, bispecifics and some allogeneic CAR-Ts (Company presentation)

ATRA’s edge in autoimmune indications (Company presentation)

Above theoretical advantages have been confirmed in the clinic and in preclinical studies

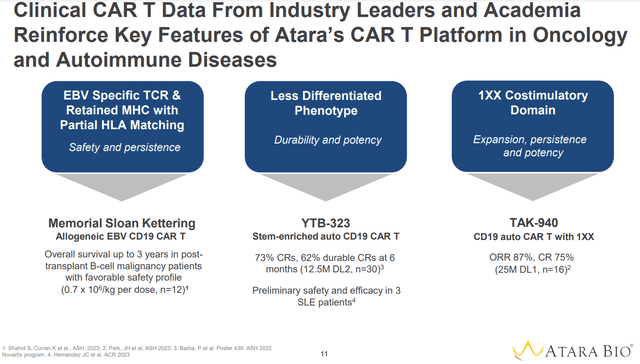

Available data from Tab-cel use, including real-life experience from post-approval use in Europe, confirm the above advantages, including safety (with regards to tumor flare reaction, cytokine release syndrome or immune effector cell-associated neurotoxicity syndrome, and graft-versus-host disease), no need for lymphodepletion, and durable responses. Additionally, data from academia and industry leaders confirm the clinical efficacy of several aspects of ATRA’s platform (see image below);

High and durable efficacy against post-transplant B-cell malignancy patients has been shown in a study by Memorial-Sloan Kettering with allogeneic EBV CD19 CAR T. High and durable efficacy using Novartis’ YTB323 (a less differentiated memory phenotype anti-CD19 CAR-T) against both in B-cell malignancies and SLE. Efficacy of CD19 auto CAR T with 1XX domain against B cell malignancies proven by Takeda’s TAK-940.

Advantages of key features of ATRA’s platform have been validated in prior studies by the academia or the industry (Company presentation)

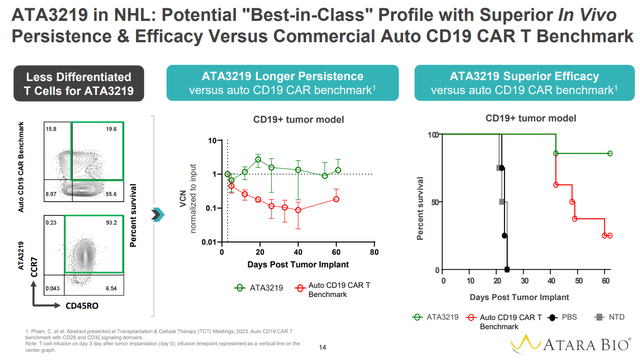

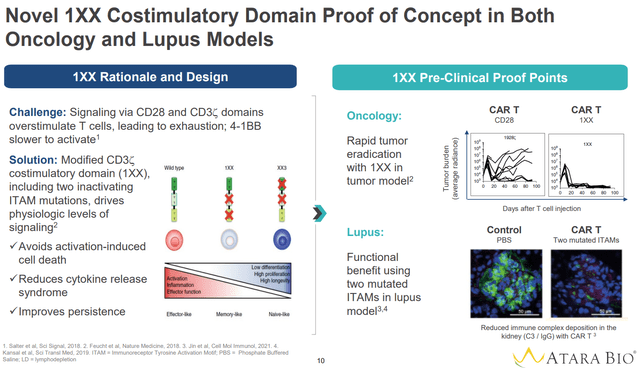

Preclinical data further support the advantages of the platform (see images below);

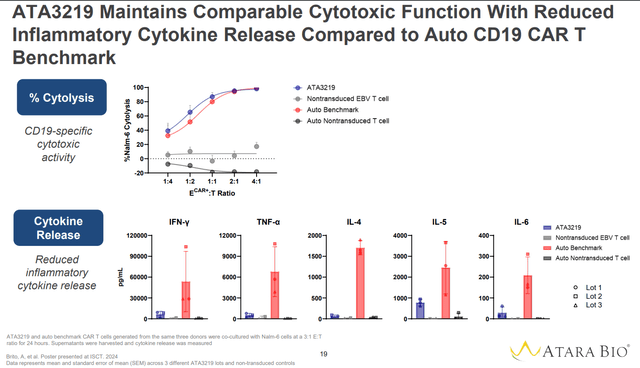

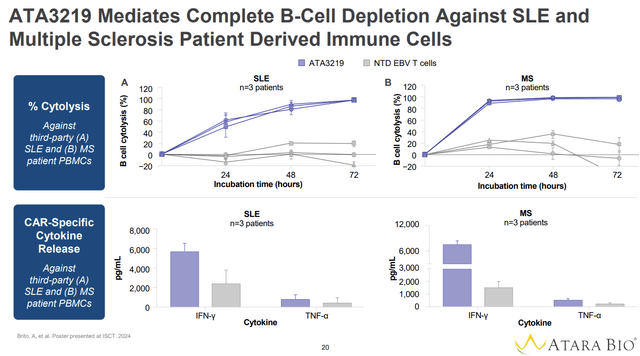

Better persistence and superior efficacy of ATA3219 vs benchmark auto CAR-T. Improved antitumor efficacy of CAR-Ts with the 1XX Costimulatory Domain. Improved efficacy in SLE nephritis model of CAR-Ts with the 1XX Costimulatory Domain. Comparable cytolysis but with lower levels of proinflammatory cytokines vs autologous benchmark (suggesting potential reduction of AEs while preserving efficacy).

Superior persistence and anti-tumor efficacy over benchmark autologous CD19 CAR-T (Company presentation)

1XX Costimulatory Domain increases antitumor efficacy and efficacy in lupus nephritis (Company presentation)

Lower level of proinflammatory cytokines vs autologous bench mark (Company presentation)

Comparable cytolysis with less cytokine release (Company presentation)

Complete B-cell depletion with reduced cytokine release (Company presentation)

Of note, don’t get too excited with the above images. Although I believe that ATRA’s platform is differentiated enough vs competitors, new CAR-T technologies under clinical development have considerably improved over approved autologous CAR-Ts and prior failed allogeneic CAR-Ts. What I mean is that the autologous benchmark shown in the images above is not representative of new and improved CAR-T technologies.

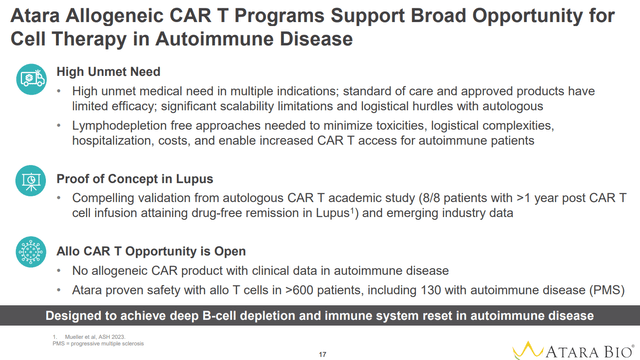

Competition in the autoimmune space

Monoclonal and bispecific antibodies are great at depleting circulating B cells and effective treatments. However, CAR T cells can cause deeper B cell depletions, including tissue-resident B cells, which allows “resetting” the immune system, resulting in durable drug-free remissions with a single infusion. This has been demonstrated by both academia and industry-sponsored studies in various indications including SLE, myositis, myasthenia gravis and scleroderma. Therefore, I will focus here on competing CAR-T companies.

A search in ClinicalTrials.gov for CAR-T therapies in autoimmune indications/ lupus/ myasthenia gravis/ myositis/ scleroderma shows 78 registered trials. Notably, a lot of competition is emerging from China. The vast majority of relevant trials are early phase, about a third being in the phase 2 stage and none currently being in a phase 3 stage. A summary of the competition can be found in the Table below (note that the list of companies in the Table is not exhaustive, but it is sufficient in my opinion to provide a comparison of ATRA’s platform to competition).

Company Asset name Target Donor Lymphodepletion Stage of clinical development

Notes

Cabaletta bio (CABA)

CABA-201 CD19 Autologous Yes. Being tried in pemphigus without lymphodepletion ph1/2 4-1BB costimulatory domain to reduce CRS/ ICANS

Kyverna Therapeutics (KYTX)

KYV-101

CD19

Autologous

Standard lymphodepletion regimen in all registered studies

LN ph1/2

SC ph1/2

MS ph2

MG ph2

KYV-201 preclinical (“multiple indications”)

It was recently announced that 1 SLE patient relapsed within 5 months of KYV-101 treatment despite initial response.

Kyverna Therapeutics (KYTX) KYV-201 CD19 Allogeneic No info (preclinical). Preclinical TCR KO + HLA-A KO + pan HLA Class II

Cartesian Therapeutics (RNAC)

Descartes-08 BCMA Autologous No

MG ph2 completed

SLE/other ph1/2

mRNA CAR-T cell therapy (see text for more details). Current dosing protocol requires 6 weekly infusions. Cartesian Therapeutics (RNAC) Descartes-15 BCMA Autologous No ph1 ready More potent than Descartes-15

Autolus Therapeutics (AUTL)

Obe-cel CD19 Autologous Yes refractory SLE ph1 Obe-cel uses a CD19 binder with fast-off rate which reduces toxicities and improves engraftment and persistence Autolus Therapeutics (AUTL) AUTO8 BCMA/CD19 Autologous Likely yes Preclinical No studies for autoimmune indications yet

BMS (BMY)

BMS-986353/CC-97540 CD19 Autologous Yes Ph1 4-1BB co-stimulatory domain and an epidermal growth factor receptor safety switch

Mustang Bio (MBIO)

MB-106 CD20 Autologous Unclear (preclinical) preclinical Allogene Therapeutics (ALLO) ALLO-329 CD19/CD70 Allogeneic No/ reduced SLE ph1 to start early 2025 uses ALLO’s “Dagger” technology to selectively eliminate alloreactive T cells thus improving persistence of alloCAR-T cells

Fate Therapeutics (FATE)

FT819 CD19 Allogeneic No SLE ph1

1XX costimulatory domain similar to ATRA.

TCR KO.

CRISPR Therapeutics (CRSP)

CTX112 CD19 Allogeneic Preclinical SLE preclinical

incorporates novel edits designed to enhance CAR T potency and reduce CAR T exhaustion.

TCR KO.

Sana Biotechnology (SANA)

SC291 CD19 Allogeneic

Yes

LN/ extrarenal SLE/ AAV ph1

different approach to avoid immune rejection of allogeneic cells which requires gene editing (HLA Ι/ΙΙ knock-out + CD47 overexpression)

TG Therapeutics (TGTX)

Azer-cel CD19 Allogeneic Preclinical Preclinical

Recently acquired from Precision Biosciences for autoimmune indications.

TCR KO

Impact Bio IMPT-514 CD19/CD20 Autologous Yes

SLE ph1/2

SLE/AAV/IIM ph1

JW Therapeutics JWCAR029 (relma-cel) CD19 Autologous Yes

moderate/severe SLE ph1

SS ph1

iCell Gene Therapeutics BCMA-CD19 cCAR T cells BCMA/CD19 Autologous Yes

r/r SLE ph1

MS preclinical

AstraZeneca (AZN) AZD-0120/GC012F BCMA/CD19 Autologous Yes

MG ph1

SLE ph1,

FasTCAR technology which drastically shortens cell production from weeks to overnight AbelZeta Inc C-CAR168 BCMA/CD20 Autologous No lymphodepletion reported in ph1 protocol SLE/MS/NMO/IMNM ph1 Essen Biotech BH002 BCMA/CD19 Autologous Yes refractory SLE ph1 Novartis AG (NVS) YTB323 CD19 Autologous Yes refractory SLE 2-day manufacturing process that preserves T-cell stemness Guangdong Ruishun Biotech Co., Ltd RJMty19 CD19 Allogeneic Yes

refractory SLE ph1

SLE/IIM/SS/AAV ph1

double-negative T cells a subtype of mature T cells that express CD3 and either αβ+ or γδ+ T cell receptor (TCR), but not CD4, CD8 or CD56. The platform has several advantages (including high proportion of stem cell-like memory T cells not causing graft-versus-host disease (GvHD), resistance to host-versus-graft (HvG) rejection, scalability, and storability) but limited clinical evidence so far. Luminary Therapeutics LMY-922 BAFF/BCMA/TACI Allogeneic Preclinical Preclinical “Immune Cloaking” technology that does not require nuclease editing Click to enlarge

Abbreviations: AAV= ANCA-associated vasculitis, CRL= cytokine-release syndrome, ICANS= immune effector cell-associated neurotoxicity syndrome, IMNM= Immune-Mediated Necrotizing Myopathy, KO= knock-out, LN= lupus nephritis, MG= myasthenia gravis, MS= multiple sclerosis, NMO= neuromyelitis optica, r/r= relapsed/refractory, SLE= systemic lupus erythematosous, TCR= T-cell receptor.

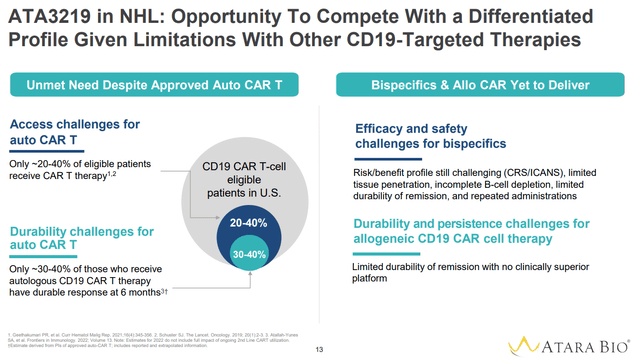

It is clear that competition in the field is fierce. So for a small biotech like ATRA to succeed the science must have significant differentiation. Based on the above, it seems that ATRA combines all the best attributes of the various other platforms;

Allogeneic platform allowing off-the-shelf availability. Allogeneic competition is relatively limited; KYTX (preclinical), ALLO (ph1 to start early 2025), FATE (ph1), CRISP (preclinical), TGTX. In other words, ATRA is not far behind allogeneic competition and is the only one with already one allogeneic product approved. Notably, all competition requires gene editing (mainly TCR KO) to allow allogeneic CAR-T cell therapy (see point below). On the contrary, most competition insists on the traditional autologous therapies (which requires an apheresis step to isolate T-cells from the patients) and generally takes longer (although newer technologies have drastically reduced the time necessary for manufacturing autologous CAR-T cell therapies to as low as overnight or 2 days). Does not require TCR gene editing or any gene editing at all to avoid GvHD and to avoid immune rejection. This improves the functionality of T-cells, simplifies the manufacturing procedure and reduces the risks associated with extra gene-editing steps.An important obstacle for allogeneic T-cell therapy is GvHD and immune rejection. Most allogeneic competition, including KYTX, FATE, CRISP, TGTX, use T-cell receptor gene editing to avoid these problems. Exceptions are Guangdong Ruishun Biotech Co., Ltd (which uses double-negative T cells, described above), SANA ( HLA Ι/ΙΙ knock-out + CD47 overexpression) and ALLO (CD70 targeting eliminates alloreactive T cells). Does not require lymphodepletion.As of now, only a few companies seem to be attempting a lymphodepletion-free CAR-T cell treatment, including CABA, RNAC, ALLO and FATE. It is safe, although this doesn’t seem to be much of an advantage over competition. In contrast to oncology, in autoimmune indications CRL/ICANS do not seem to be as much of a problem. On the other hand, lymphodepletion is associated with significant adverse events. Therefore, a CAR-T cell therapy that can obviate the need for lymphodepletion (if possible) would be a major commercial advantage, as already discussed. It achieves in vivo expansion, persistence and durable responses. Whether persistence will prove to be beneficial in autoimmune indications remains to be seen. Importantly, ATRA remains the only company with an approved allogeneic CAR T cell therapy.

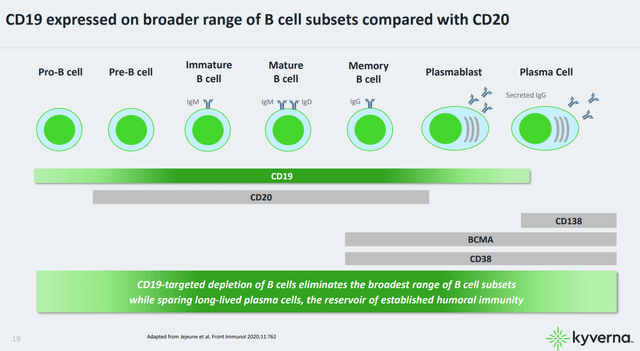

Similar to most of the competition, ATA3219 is targeting CD19-positive B-cells, which targets the broadest range of B cell (see image below), and has been validated as a good target by durable drug-free responses by both academia and the industry. Others (e.g. RNAC) have targeted BCMA which is expressed by antibody-producing plasmablasts and plasma cells and has been proposed to be a great target for autoantibody-mediated diseases. Others (e.g. iCell Gene Therapeutics, AUTL, AZN, Essen Biotech), take a further step, using dual-targeted anti-BCMA/CD-19 CAR-T cells aiming for even deeper B-cell depletion. Luminary Therapeutics use a triple-target CAR-T, targeting BAFF/BCMA/TACI. It remains to be seen if other approaches have any advantage in terms of safety/efficacy over targeting just CD19. Of note, there is nothing stopping ATRA developing BCMA-targeted or dual-targeted BCMA/CD19-targeted T cells using its platform if this approach proves to be better.

B-cell expression of various markers, including CD19, CD20 and BMCA at different stages of maturation (KYTX company presentation)

A unique approach among CAR-T cell companies is used by RNAC. In contrast to all other companies, RNAC uses mRNA (vs DNA gene editing) to prepare its CAR-T cells. This approach avoids potential risks associated with gene editing (e.g. risk of CAR-T cell malignancy). More importantly, it results in predictable pharmacokinetic/pharmacodynamic properties. This allows fine-tuning of the dose to achieve a therapeutic effect and avoid adverse events. A limitation is that multiple doses may be necessary (6 weekly doses for Descartes-8). Interestingly, RNAC is also developing an allogeneic mRNA Mesenchymal Stem Cell therapy (Descartes-33).

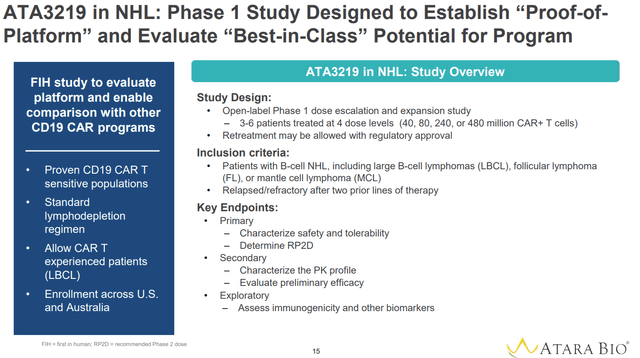

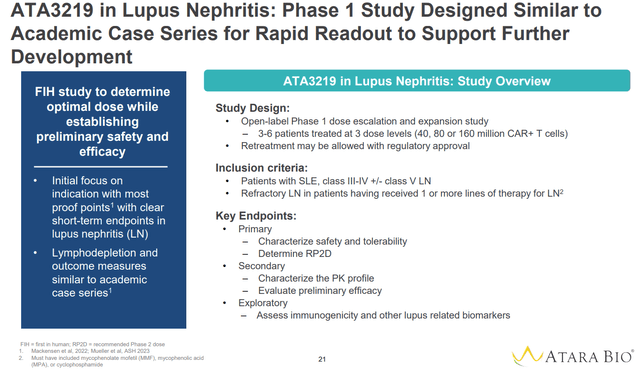

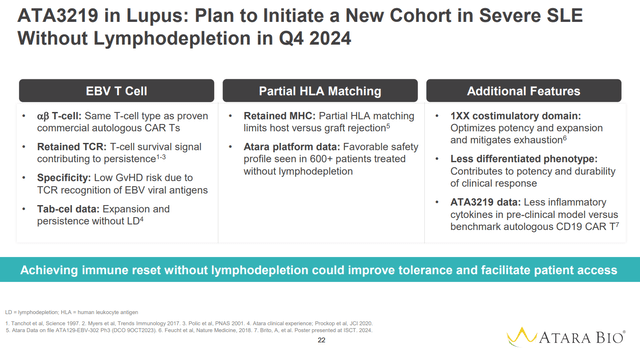

Overview of ongoing/planned studies of ATA3219

The design of ongoing planned studies is summarized in the images below. Since we already know how CAR-Ts work, I don’t expect any groundbreaking data. But these studies will provide the necessary clinical validation for further progress. From the study in NHL, it will be interesting to see if ATRA’s CAR-T therapy can improve the durability of responses. Perhaps the most important data are those expected from the expansion cohort in severe SLE, which will determine the feasibility of a lymphodepletion-free allogeneic CAR-T cell therapy in autoimmune indications, which could prove to be a major commercial advantage long-term. I highlight again here, that ATRA’s EBV-based T-cell platform does not require any further modifications to avoid GvHD and immune rejection, in contrast to other allogeneic CAR-T therapies.

Phase 1 study in NHL (Company presentation)

Phase 1 study in lupus nephritis using a standard lymphodepletion regimen (Company presentation)

Planned cohort using a lymphodepletion-free regimen (Company presentation)

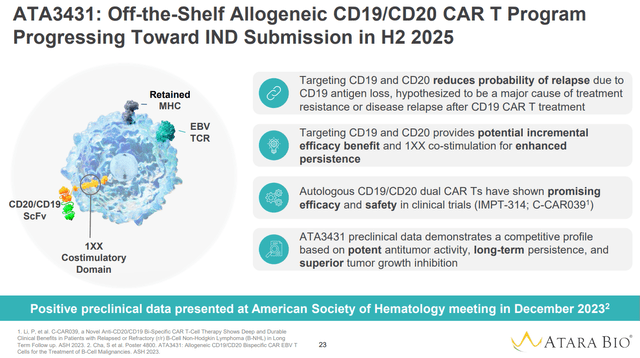

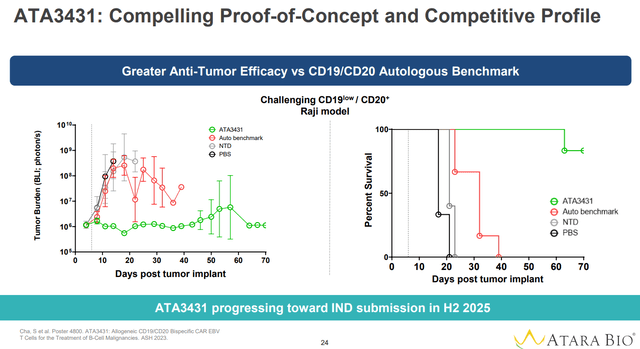

CD19/CD20 CAR T Program (ATA3431)

This program is still preclinical with an IND expected later this year. The rationale of ATA3431 is that by targeting both CD19 and CD20 the probability of relapse due to CD19 antigen loss is decreased.

Overview of ATA3431 (Company presentation)

Preclinical data suggest superior anti-tumor efficacy over autologous CD19/CD20 CAR-T benchmark (Company presentation)

Financials

ATRA reported $82.1M in Cash, cash equivalents, short-term investments and accounts receivable as of March 31, 2024. ATRA has guided a cash runway into 2027. However, this guidance is based on numerous assumptions;

anticipated regulatory milestone payments; $20 million upon acceptance of BLA submission (expected by 20 July 2024) and $60 million upon approval (expected October 2024). “anticipated purchases of tab-cel inventory through the manufacturing transfer date by Pierre Fabre”. Total inventories as of March 2024 were $16M. “anticipated reimbursement for tab-cel global development costs through the BLA transfer by Pierre Fabre”. Tab-cel R&D expenses were $22M in 2023 and $6.5M in Q1 2024. “operating efficiencies resulting from completed workforce reductions”; ATRA has guided a 35% reduction in operating expenses in 2024. Based on 2023 total operating expenses of $284.5M, this means that operating expenses for 2024 are expected to be about $185M, with “the large majority of the year-over-year operating expense reduction expected to begin in Q2 2024”. Considering Q1 operating expenses of $58.6M (R&D $45.5M, G&A $11.1M), operating expenses for the rest of 2024 (Q2-Q4) are expected to be about $123M. “the planned transition of substantially all activities relating to tab-cel at the time of the BLA transfer to Pierre Fabre potentially as early as Q1 2025, which will further reduce quarterly operating expenses”; Following this transition Pierre Fabre will be responsible for all tab-cel related expenses (including the ongoing clinical trial, regulatory procedures, manufacturing and commercialization). Notably, costs “relating to performing the services within the Additional Territory Obligation and Process Sciences Obligation” were approximately $12.3M in Q1 2024. anticipated royalties from sales of tab-cel in the U.S.; It is unclear how much royalty revenue ATRA assumes for this guidance. Assuming tab-cel achieves US peak sales >$500M as estimated by ATRA (a reasonable estimation as explained in my last coverage) and considering “significant” double-digit royalties ATRA may in few years have a yearly royalty revenue >$75M (assuming 15% royalties). Interestingly, above assumptions do not seem to include potential commercial milestone payments which can be up to $520M (details of the deal are not yet public), suggesting a conservative estimation of sales growth by ATRA.

Assuming there are no regulatory delays, most of the above assumptions are reasonable in my view. Of note, as acknowledged by ATRA in the latest 10Q, “Our existing cash, cash equivalents and short-term investments as of March 31, 2024 will not be sufficient to fund our planned operations for at least the next 12 months after the date of issuance of these financial statements”. In other words, a regulatory delay (FDA rejecting the BLA submission or a complete response letter) would mean that ATRA would have to raise cash (at least $20M just to get through 2024 according to above estimations and assuming Pierre Fabre will reimburse ATRA for tab-cel related expenses) which would likely be detrimental for current shareholders at ATRA’s current valuation.

It is important to clarify that the guided runway is based on “planned operations”. I assume that this does not account for more new clinical studies, beyond the planned ph1 SLE studies. ATRA will need considerably more cash to advance its CAR-T pipeline in later-stage clinical trials, and to expand to additional indications.

Risk factors

The major risk factors for ATRA are the following;

There is risk of regulatory delays and/or suboptimal tab-cel sales in US. This will negatively affect ATRA’s cash runway, which is dependent on the pending $80M regulatory milestone payments. ATRA will eventually need to raise considerably more funds to move the CAR-T pipeline to the next stages. Although according to ATRA longer persistence is an advantage of its platform, I have some doubts whether this is an advantage in autoimmune indications. The rationale for CAR-T cell therapy in autoimmune indication is to cause a transient deep depletion of B cells, resulting in resetting of the immune system. This transient depletion is followed by reconstitution of B cells no longer reactive to self-antigens. A longer than necessary B cell depletion may be problematic, unnecessarily prolonging the duration of immunosuppression associated with B-cell depletion. On the other hand, this persistence of CAR-T cells may be important to allow deep B-cell depletion without any lymphodepletion. I was wrong about ATRA before. Despite strong scientific rationale, ATRA failed in multiple sclerosis. Therefore, there is the risk that I am wrong about the rest of ATRA’s CAR-T pipeline as well. There is a theoretical possibility that ATRA may choose to monetize US tab-cel royalties (as it did with EU royalties) to focus on its CAR-T pipeline. This will considerably increase the investment risk. I doubt ATRA would chose to take such an action unless ph1 results in NHL/SEL are very promising.

Conclusion

Assuming all goes well with Tab-cel FDA approval, ATRA is well-funded to deliver proof-of-concept clinical data in both NHL and SLE. At current valuations, I believe ATRA is undervalued based on tab-cel alone. Even if the rest of the pipeline fails, ATRA is expected to have a yearly royalty revenue higher than its current marker cap. On the other hand, if ATRA delivers competitive data for either its oncology or autoimmune pipeline, ATRA’s valuation should easily match/surpass that of CAR-T-focused competitors (e.g. CABA, KYTX, RNAC all currently having a market cap >$300M). ATRA’s CAR-T platform combines the best attributes of various other platforms and has a best-in-class potential. On the other hand, despite very promising science, there is the risk that ATRA may fail in the clinic or may not produce competitive enough results. As discussed above, there is vast competition in the field. Furthermore, the whole thesis is based on the assumption that tab-cel will be FDA approved by the end of 2024. If not, expect dilution.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

GIPHY App Key not set. Please check settings