Alllex/E+ via Getty Images

By Erik Norland

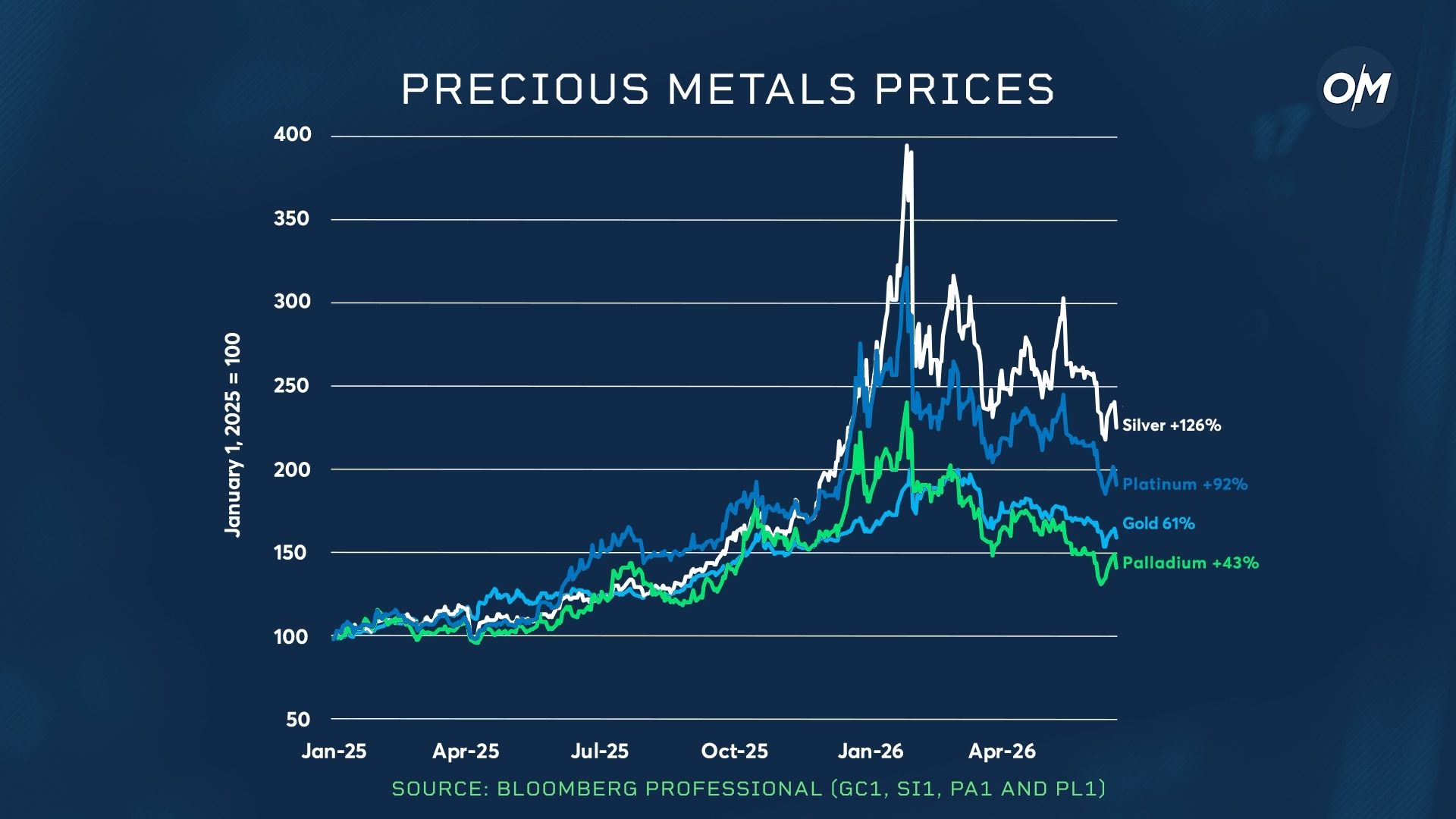

Precious metals spent two years defying gravity. The rally that ran through 2024 and 2025 was one of the most sustained in recent memory until January 2026, when it wasn’t.

Prices have since retreated sharply, leaving investors to ask three questions at once: What built this run-up? What caused the reversal? And where might they be headed next?

The answer to the first question is not a single catalyst but a convergence. The run-up in precious metals prices appeared to have been based on three market narratives:

Heightened concerns over the independence of major central banks Central banks cutting rates despite core inflation remaining above target Government budget deficits running at historically elevated levels

The turning point for precious metals came on January 23, 2026, as word spread on Wall Street that Kevin Warsh was being nominated as the next Federal Reserve Chairman.

As a well-known critic of quantitative easing and holding rates near zero for extended periods, Warsh’s appointment signaled the conclusion of the Fed’s accommodative era.

That shift was confirmed at his first FOMC meeting in mid-June, when the committee dropped its easing bias and opened the door to future rate hikes. With that, one of the pillars of the precious metals bull market had been pulled.

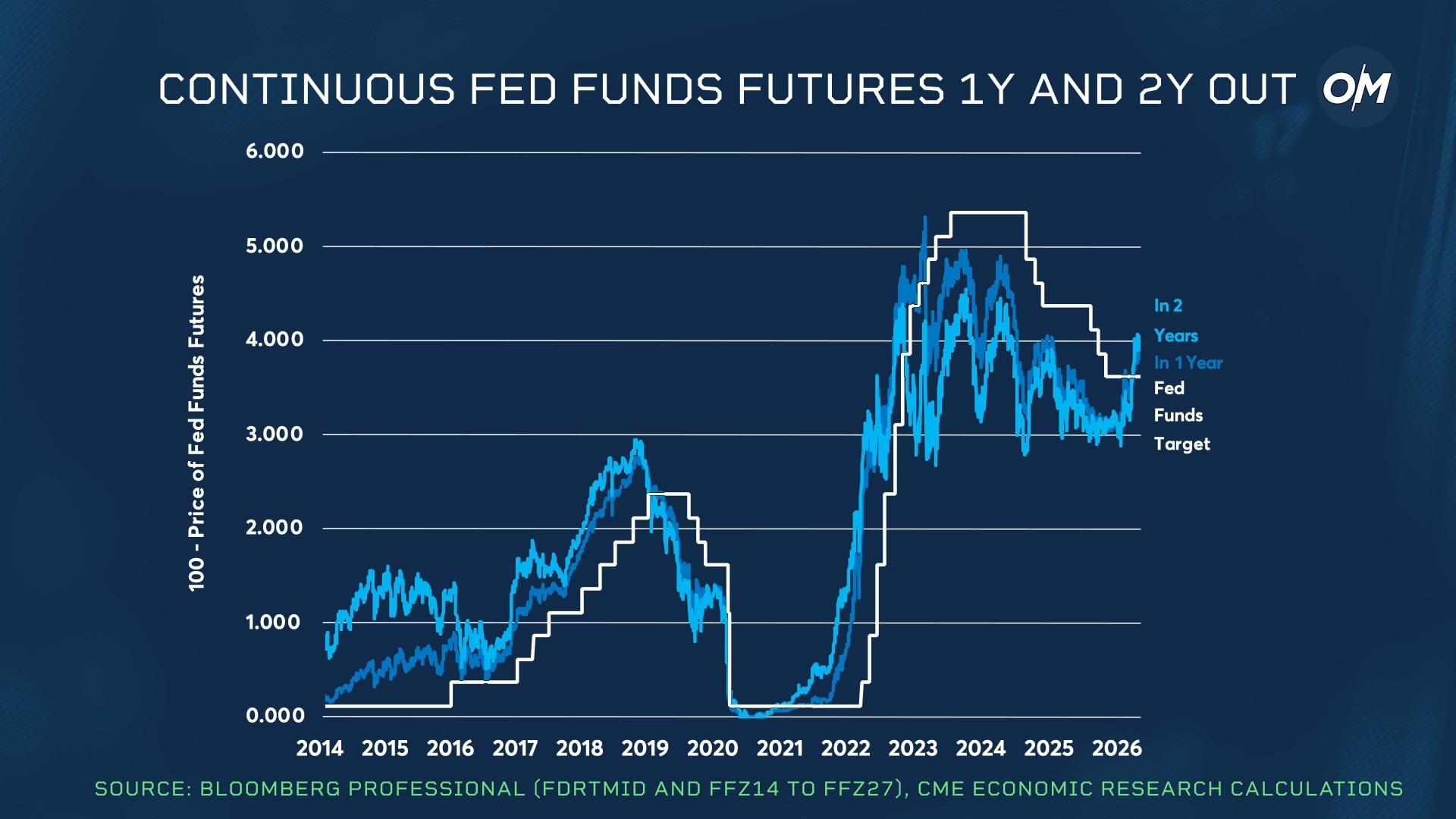

A New Global Interest Rate Landscape

The Fed’s pivot did not happen in isolation. The global monetary landscape has shifted from a tailwind to a distinct headwind. The European Central Bank, the Reserve Bank of Australia and Norges Bank have all followed the Bank of Japan in raising interest rates, while Fed Funds futures now indicate that the Fed itself could tighten policy this year.

Higher rates are inherently bearish for precious metals; they elevate the opportunity cost of holding non-yielding assets like gold. But the rate level may matter less than what it signals.

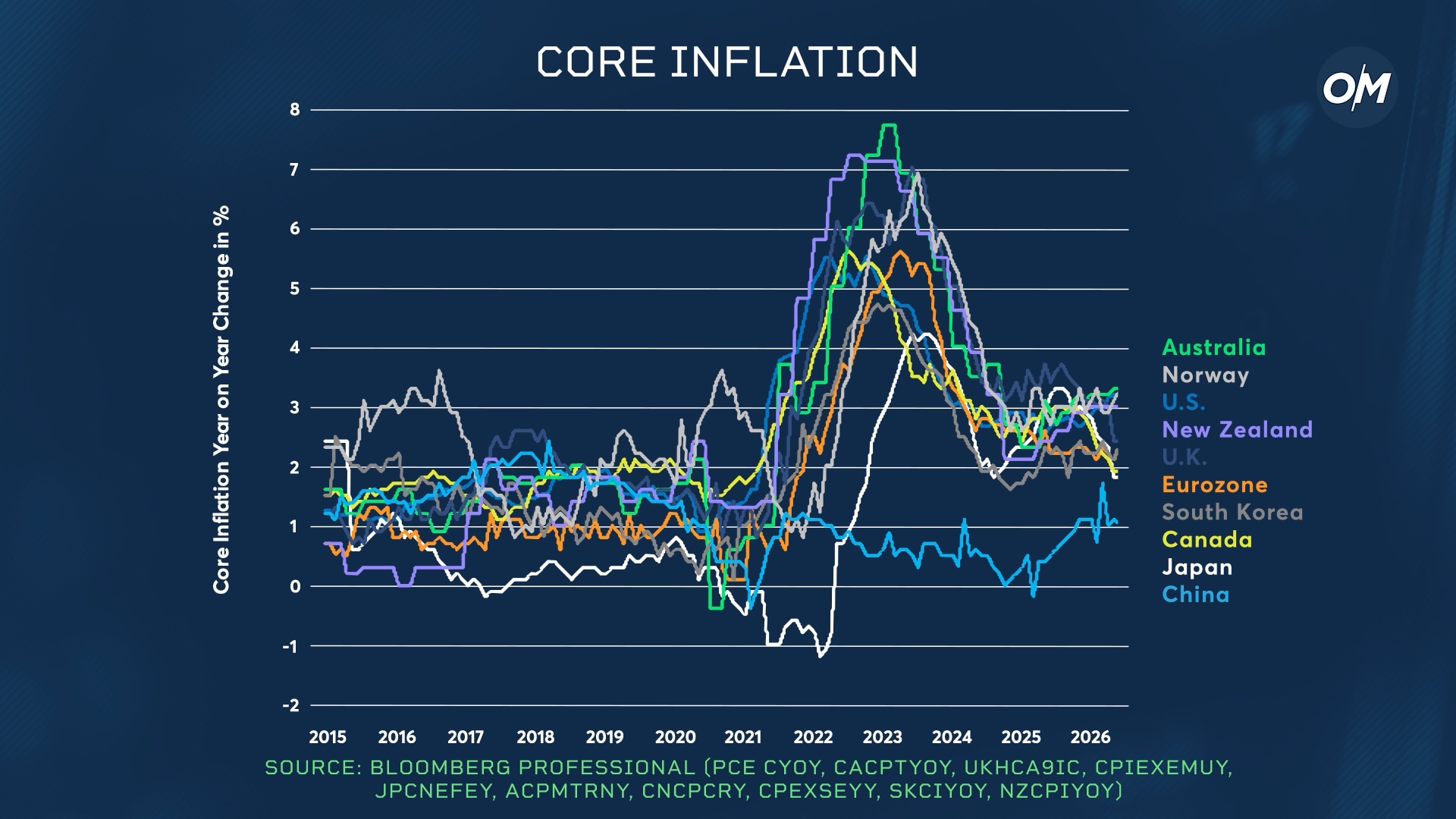

When central banks tighten, it signals they are addressing the situation, and that often erodes the fear premium embedded in precious metals prices. Core inflation is still sticky across most developed economies, but it is the policy shift, not the inflation data itself, that seems to have changed how investors are positioning.

The One Pillar That Hasn’t Moved

While central banks are beginning to tighten monetary policy, fiscal policy remains extraordinarily loose.

From the U.S. and Japan to France, Germany, the U.K., China and Brazil, governments are continuing to run abnormally large budget deficits. Longer-term, the direction of budget deficits could play a determining role in the outlook for precious metals and long-term bond yields. Any coordinated political effort to rein in deficits could lower long-term yields and reduce the structural lure of precious metals.

The precious metals rally is paused, but not necessarily over. Markets will be watching the Fed’s next moves, the trajectory of core inflation and any credible signs of fiscal policy shifts. The variable that ended the bull run has shifted. The one that could restart it has not.

GIPHY App Key not set. Please check settings