ElementalImaging

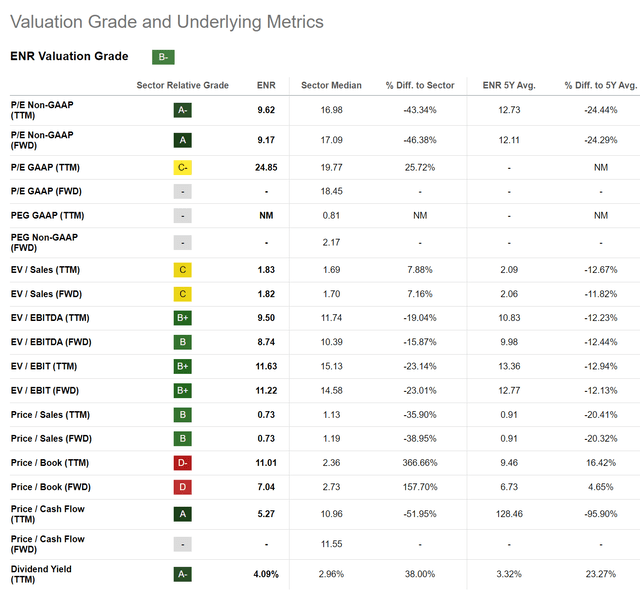

I recently came across Energizer Holdings, Inc. (NYSE:ENR) while screening for cheap companies. ENR certainly fits the bit of being ‘cheap’, as the company trades at just 9.2x Non-GAAP Fwd P/E with a 4.1% dividend yield (Figure 1).

Figure 1 – ENR trades at a cheap valuation (Seeking Alpha)

However, is ENR a ‘value-trap’ or a ‘turnaround’ candidate?

In my opinion, ENR is an interesting value opportunity for patient investors. Assuming the company can execute its strategy of generating FCF and paying down debts, I see 60-100% total return upside to ENR’s shares.

The key risk to ENR is the company’s heavy debt load limiting the company’s financial flexibility if the economy turns sour. I rate ENR a buy.

Company Overview

Energizer Holdings is best known for manufacturing and selling batteries and portable lighting products under the Energizer, EVEREADY, Rayovac, and VARTA brand names. ENR is also a leading designer and marketer of automotive cleaning and fragrance products under recognizable brands such as A/C Pro, Armor All, Bahama & Co., California Scents, and many others.

Energizer can trace its corporate history back to 1896 when W.H. Lawrence invented the first dry cell battery for consumer use. The current iteration of the company was spun off from Edgewell Personal Care Company (EPC) in 2015.

Ill-Fated Transaction Saddled The Company With Excessive Debt

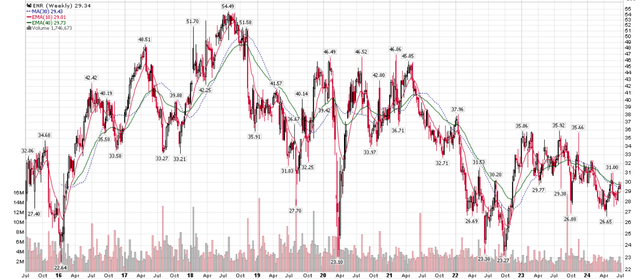

Energizer’s stock price peaked in 2018 at ~$55 / share and has been in a downtrend for the past six years (Figure 2).

Figure 2 – ENR stock performance (stockcharts.com)

The turning point in the company’s stock price appears to be Energizer’s ill-fated acquisition of the Rayovac, VARTA, Armor All, STP, and A/C Pro brands from Spectrum Brands (SPB) in 2019 (announced in 2018) for $2 billion in cash. The transaction saddled ENR with more than $3 billion in long-term debts.

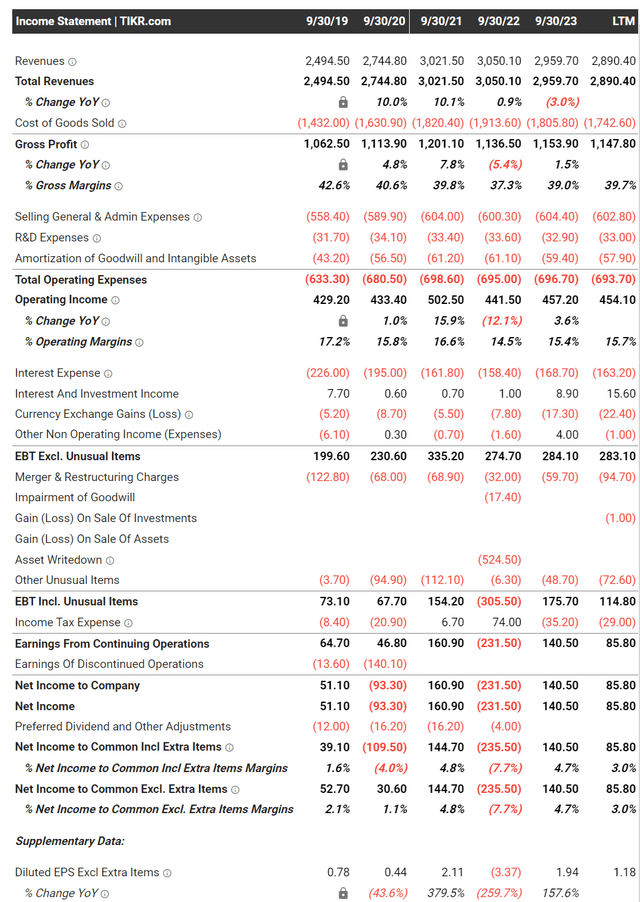

After write-offs and restructuring charges of over $1 billion in the past 5 fiscal years, Energizer shareholders do not appear to have much to show for the transaction, as the company earned $1.52 / share in fiscal 2018 compared to $1.18 in the last twelve months (Figure 3).

Figure 3 – ENR financial summary (tikr.com)

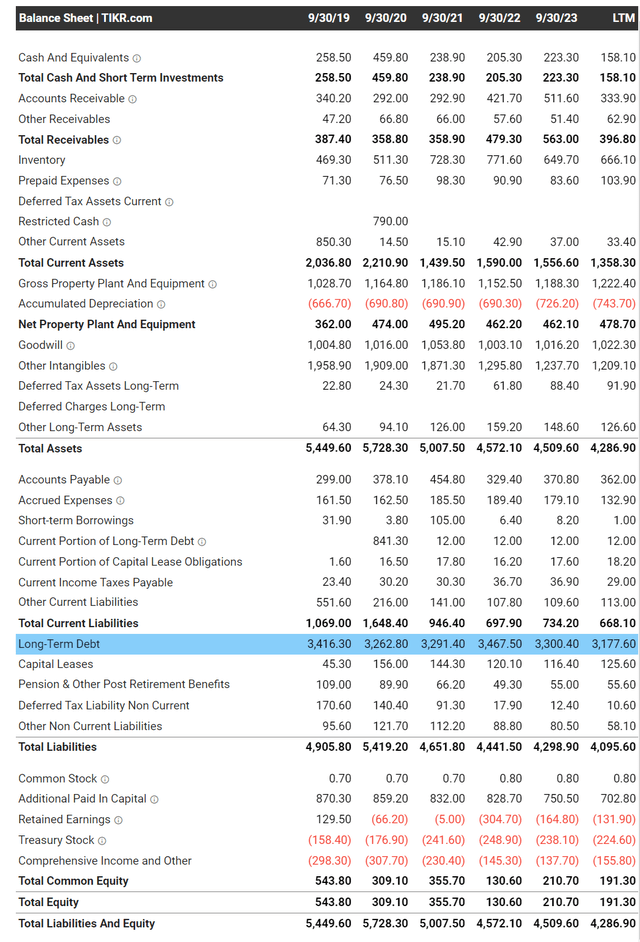

The company’s balance sheet also does not appear to have shown much progress, as Energizer still has $3.2 billion in long-term debt compared to $3.4 billion at the end of Fiscal 2019 (Figure 4).

Figure 4 – ENR balance sheet summary (tikr.com)

Is Energizer Finally Turning The Corner?

However, selling disposable batteries to consumers appears to be a fundamentally wonderful business, as evidenced by Energizer’s 15-17% operating margins and low-capex intensity.

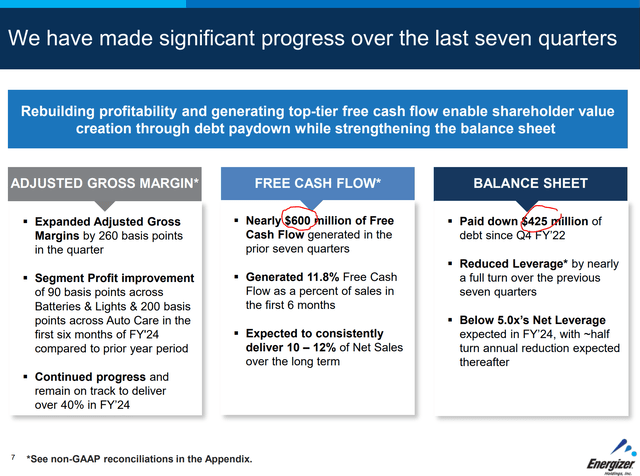

In fact, there are reasons to be hopeful, as the company claims to have generated nearly $600 million in free cash flows (“FCF”) in the prior 7 quarters and has paid down $425 million in debts (Figure 5).

Figure 5 – ENR appears to be turning the corner (ENR investor presentation)

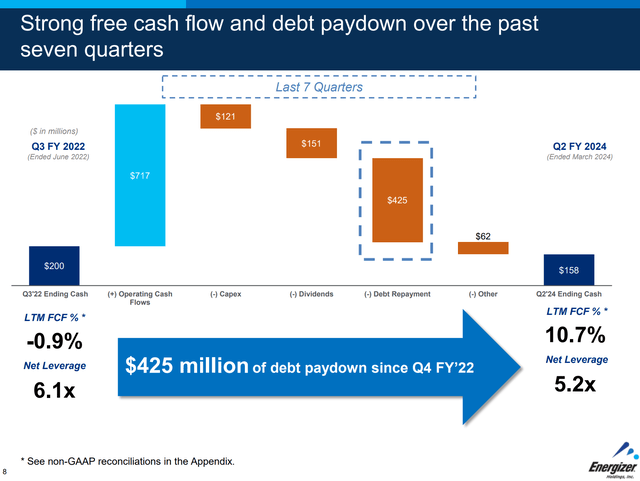

Since Q3/F22, management’s restructuring efforts have been able to boost free cash flows from a negative 0.9% FCF yield to 10.7% (Figure 6).

Figure 6 – ENR’s restructuring efforts paying off (ENR investor presentation)

Looking forward, management believes the company can consistently deliver 10-12% of Net Sales as FCF. This should allow Energizer to quickly deleverage the business, from 6.1x Net Debt / EBITDA in Q3/F222 to 5.2x currently, and <5.0x by the end of fiscal 2024. Management expects to be able to reduce leverage by half a turn every year thereafter.

Path To Steady Value Creation

In my opinion, taking management at their word, shareholders have a clear path to a 60% gain on their shares or more over the next few years.

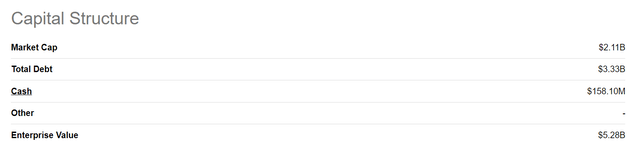

Referring to Figure 1 above, we can see that Energizer is currently valued at 8.7x Fwd EV/EBITDA. At the same time, we can see that ENR’s balance sheet is debt-heavy, with $3.3 billion in debts and leases outstanding (Figure 7).

Figure 7 – ENR enterprise value is debt-heavy (Seeking Alpha)

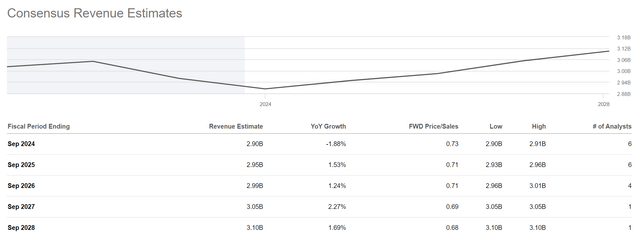

Assuming the company can generate 10% of Net Sales as FCF, then that equates to ~$300 million of FCF annually for the next 5 years (Figure 8). If all of ENR’s FCF is directed towards paying down debts, then at the end of 2028, I estimate Energizer’s debt balance to be ~$2.0 billion ($3.3 billion less $1.35 billion in FCF).

Figure 8 – ENR revenue estimates (Seeking Alpha)

If we assume Energizer’s valuation stays the same at $5.3 billion in enterprise value, that means the company’s equity should be worth $3.5 billion ($5.3 billion EV – $2.0 billion debt + $160 million cash), or 65% higher at the end of 2028.

Furthermore, we can see that Energizer is currently valued at a discount to its Consumer Staple peers, who are trading at a median multiple of 10.4x Fwd EV/EBITDA. This is most likely due to the company’s bad balance sheet and poor growth prospects.

If Energizer can address its debt overhang, it may be reasonable to expect ENR’s valuation multiple to expand. Assuming a modest expansion in ENR’s valuation multiple to 9.4x Fwd EV/EBITDA (still a discount to peers due to slower growth), ENR’s equity could be worth $3.8 billion (9.4 x $600 million in EBITDA – $2.0 billion debt + $160 million cash) or 80% upside.

Finally, Energizer should be able to handily pay its 4.1% dividend yield if it can generate the expected levels of FCF. So assuming management can execute, patient investors can look forward to 60-100% total returns from their investment in ENR stock over the next few years.

Risks to ENR

While I have laid out a bullish scenario above on how shareholders can achieve 60-100% returns on ENR stock over the next few years, there are also risks to consider.

First, investors are dependent on management to stay true to their strategy and continue to deleverage ENR’s balance sheet instead of going after spurious M&A transactions. Readers are reminded that ENR’s current CEO, Mr. Mark Lavigne, was Energizer’s General Counsel before his current appointment in 2021, so he presided over the disastrous Spectrum transaction as a senior executive at Energizer. Once Energizer’s leverage is reduced, he may return to empire-building mode and pursue another value-destroying acquisition.

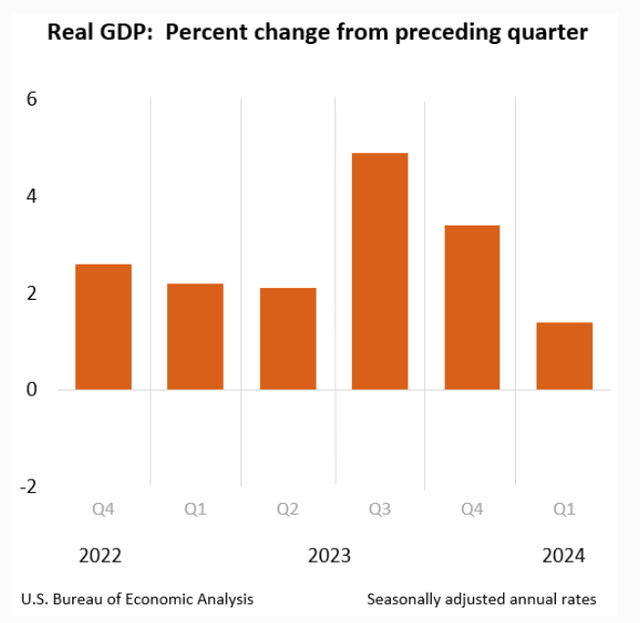

Another risk to Energizer has to do with the U.S. economy. The above bullish scenario assumes the economy remains steady for the next 5 years without major shocks. This may be wishful thinking, as economic growth has slowed significantly in recent quarters (Figure 9). If the economy falls into a recession, then Energizer’s sales may be negatively impacted.

Figure 9 – Economic growth has slowed (BEA)

While batteries are considered a consumer staple and should see continued demand even in a recession, the same cannot be said of automotive care products. When consumers are financially stretched, they may cut back on discretionary items like Armor All or California Scents.

Conclusion

In my opinion, Energizer Holdings may present an interesting opportunity for patient investors. Assuming the company can execute its strategy of running its operations for cash flows to pay down debt, shareholders could see 60-100% in total returns over the next 5 years.

However, the risk to Energizer is the company’s heavy debt load, which limits the company’s financial flexibility if the economy turns sour. Weighing the rewards vs. the risks, I believe Energizer’s cheap valuation is worth a buy rating.

GIPHY App Key not set. Please check settings