Lahiru Lakmal/iStock via Getty Images

After a strong advance last year and an encouraging start to 2026, global stock markets came under acute pressure in the wake of the Iran war (started on February 28, 2026). For the first quarter, the S&P 500 and MSCI World indices each declined 4.33% and 3.57%, respectively, while the Russell 2000 and MSCI EAFE (local, USD) fared a bit better at 0.89%, 0.15%, and -1.24%, respectively. With energy prices soaring and the war ongoing, risk appetites have dampened. As investors try to navigate heightened geopolitical and economic uncertainty, FMI takes comfort knowing that our portfolios are comprised of high-quality businesses with robust balance sheets, that trade at discounts to their respective benchmarks. Stock market pullbacks can create compelling long-term investment opportunities, which we strive to capitalize on.

Crude Awakening

The most consequential development in the Iran war is the blockage of the Strait of Hormuz, where ~20% of the world’s global oil and liquified natural gas (LNG) pass through. Asia is the region most affected by the closure, with the Gulf economies hardest hit. This has led to the “largest supply disruption in the history of the global oil market,” per the International Energy Agency (IEA), which has coordinated the release of 400 million barrels of oil from emergency reserves to help cushion the blow. Despite these efforts, oil eclipsed $100 per barrel both in the U.S. and overseas, with fears that it could spike significantly higher from here if the conflict drags on. The economic implications would be wide-ranging and felt globally.

Like tariffs, high energy prices act as a de facto tax on consumers, with lower-income households feeling the most pressure given a larger percentage of their income is spent on utilities and fuel. With the average price of gas at a U.S. pump topping $4 for the first time since 2022, consumers are already starting to feel the pinch. Businesses are also facing headwinds on profit margins due to rising input and transportation costs (some shipping lanes are being rerouted to avoid the region). Lower-quality businesses which lack pricing power are likely to face the most significant challenges. Rothschild & Co estimates that sustained oil prices of $100 per barrel in the U.S. for three months would lift the consumer price index (CPI, the most widely recognized gauge for inflation) from 2.4% to 4.0% this year. This would create significant economic growth headwinds as well, as they forecast each 10% increase in the U.S. Energy CPI would reduce quarterly annualized GDP growth by approximately 0.7%.

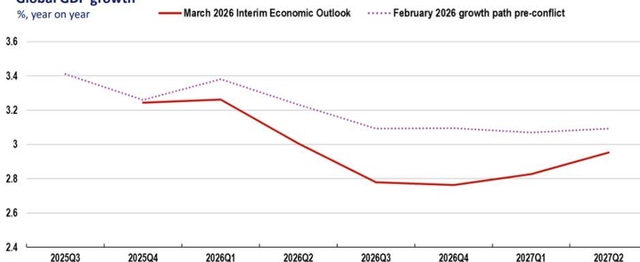

Global central banks find themselves in a difficult situation, contending with rising inflation and interest rates, while employment and economic growth are weakening. A prolonged conflict could undoubtedly trigger a recession, or perhaps worse, stagflation. Less than a month after the war began, the OECD had already cut its global GDP growth forecasts, per the chart below:

The conflict in the Middle East is testing the resilience of the global economy

Source: OECD

Global GDP growth%, year on year

Market Rotation: Barrels and Bombs

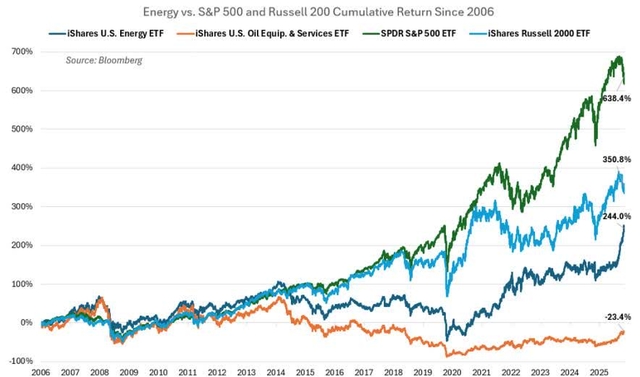

Not surprisingly, energy and defense stocks have outperformed in recent periods. Historically, FMI’s portfolios have had an underweight exposure to both given business quality and valuation considerations.

Energy companies are highly dependent on commodity prices, which ultimately are out of their control. Prices are driven by global supply and demand dynamics, or other factors such as OPEC decisions and geopolitical events. The energy sector has historically been known for boom-and-bust cycles: high prices incentivize overinvestment, resulting in oversupply, which leads to falling prices, causing capital destruction and underinvestment, then supply tightens, prices rise, and the cycle repeats. High capital intensity and poor capital allocation have weighed on the long-term return profiles of these businesses, with many failing to earn their cost of capital over a full cycle. While these can be great trading stocks from time to time, energy has been a tough place to invest over the last 20 years, as the following chart depicts:

Conversely, defense companies have outperformed broader market indices over the long term. FMI’s exposure to defense has been limited due to business quality concerns around a reliance on government budgets (which have grown slowly most years), government deficits and stretched balance sheets, political and regulatory risk, and limited pricing power (cost-plus and fixed-price contracts). As we have discussed in prior letters, Russia’s invasion of Ukraine in 2022 became a major shot in the arm for European defense, meaningfully altering the spending trajectory for Germany and several others. The broadening conflict in the Middle East certainly helps the cause. Valuations today appear to reflect these improved growth expectations.

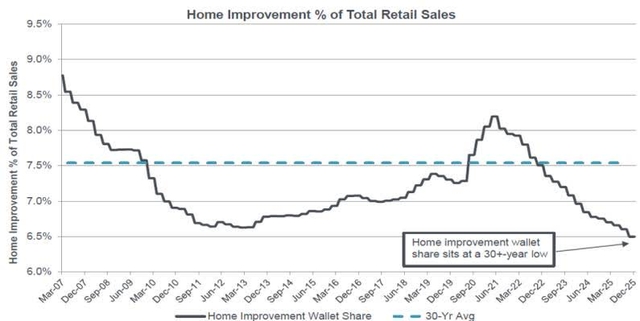

Meanwhile, FMI’s overweight exposure to durables and manufacturing end-markets, specifically geared towards building materials, housing and construction, have hurt our relative performance in recent quarters. We have leaned into this segment over the last few years as cyclical pressures (higher rates, affordability challenges) have weighed on the stocks. We find the housing repair and remodel (R&R) market to have an especially attractive long-term set-up, for several reasons. The median age of the housing stock in the U.S. continues to climb, now up to 42 years (from 31 in 2005). Older homes require more maintenance, upgrades, and system replacements (HVAC, plumbing, electrical, etc.). Over 50% of homeowners have mortgage rates below 4%, creating a “lock-in” effect where it may make more sense to renovate than to sell and buy a new home at a much higher rate. With rising home prices in recent years, homeowners are also now sitting on near-record levels of home equity, creating financial capacity to invest in their homes. Lastly, there is believed to have been around $50 billion of deferred maintenance in recent years, as home improvement spending has been well below historical levels (as shown in the middle chart), creating pent-up demand. To take advantage of this investment opportunity, we hold several competitively advantaged businesses across each of our portfolios: Large Cap (Carrier Global Corp. (CARR), Ferguson Enterprises Inc. (FERG), Masco Corp. (MAS)), Common Stock (Fortune Brands Innovations Inc. (FBIN), Hayward Holdings Inc. (HAYW), Louisiana-Pacific Corp. (LPX)), International (Ferguson Enterprises Inc., Fluidra S.A. (FLUIF), Howden Joinery Group PLC (HWDJY)), and Global (Masco Corp., Carrier Global Corp., Ferguson Enterprises Inc.). When cyclical weakness turns into an end-market recovery, there is potential for low valuation multiples on depressed earnings to create coiled springs.

Despite the market rotations described above, it’s important to remember that things can change quickly. The market drivers of today may not be the drivers of tomorrow. In the past, stock market reactions to military conflicts have been sharp, but relatively short-lived. As outlined in the RBC table on the bottom, on average, the S&P 500 has fallen around 6% after a military conflict, bottoming just 13 trading days after the event while taking 28 days to recover. Notably, declines coinciding with crude oil spikes (red boxes above) tend to be larger in magnitude (-13% on average) and take longer to recover. The S&P 500 recently declined 8.5% from its peak at the start of the war. If the war ends in the coming weeks, we may have already hit bottom. If there is no end in sight, the market could continue to face increasing pressure. Anything is possible.

S&P 500 responses to select military interventions and hostilities since World War II

Event Start date* Trading days to trough % change to trough Trading days back to even N. Korea invades S. Korea June 25, 1950 15 -12.9% 56 U.S. spy plane shot down in USSR May 7, 1960 2 -0.6% 4 Bay of Pigs invasion April 15, 1961 6 -3.0% 14 Cuban Missile Crisis Oct. 16, 1962 6 -6.3% 13 Gulf of Tonkin Incident (Vietnam) Aug. 2, 1964 4 -2.2% 29 Lead-up to Six-Day War (June 6) May 14, 1967 15 -5.6% 20 Tet Offensive (Vietnam) Jan. 29, 1968 25 -6.0% 46 Cambodian Campaign (Vietnam) May 1, 1970 18 -14.9% 86 Yom Kippur War, Arab oil embargo Oct. 6, 1973 42 -16.1% 6 years** Soviet-Afghan War Dec. 24, 1979 7 -2.3% 10 Intervention in Grenada Oct. 25, 1983 11 -2.8% 15 Lead-up to intervention in Panama Dec. 15, 1989 2 -2.2% 8 Iraq invades Kuwait, oilfields seized Aug. 2, 1990 50 -15.9% 131 Lead-up to Gulf War (Desert Storm) Jan. 1, 1991 6 -5.7% 13 Intervention in Yugoslavia (Balkans) March 24, 1999 3 -4.1% 11 U.S. spy plane captured in China April 1, 2001 3 -4.9% 7 War in Afghanistan Oct. 7, 2001 1 -0.8% 3 Lead-up to Iraq War Feb. 5, 2003 24 -5.6% 28 Russia intervention in Ukraine Feb. 11, 2022* 17 -7.4% 27 12-Day War (Israel/U.S. and Iran) June 12, 2025 5 -1.3% 7 Average of all 20 events — 13 -6.0% 28

Click to enlarge

Source: RBC Wealth Management, RBC Global Asset Management, National Security Archive at George Washington University, Wikipedia, U.S. Naval Institute

Click to enlarge

Fortunately, FMI’s focus on business quality, discounted valuations, and balance sheet strength have typically led to relative outperformance in more difficult stock markets.

Contrarian Special: FMI

In recent years, we have written extensively about the headwinds facing investors that deploy a value-oriented approach and/or a quality focus. After enduring a historically tough stretch for value investing, more recently, quality has been challenged both domestically and overseas.

Despite the backdrop, we remain committed to our investment process, fine-tuned over the last 45+ years. We cannot control the behavior of the stock market. Over full cycles, valuations and balance sheets matter. We are investing right alongside you, our investors.

—–

The following stock examples capture a few pockets of the market where we are finding attractive investments. Both Huron Consulting Group Inc. (HURN) and Booking Holdings Inc. (BKNG) have sold off on artificial intelligence (AI) concerns, which we think are overblown and misunderstood. IMCD is facing cyclical fundamental pressures which we expect to abate over our investment time horizon:

Huron Consulting Group Inc. (HURN) – Common Stock

Huron is a leading consulting firm serving hospitals, health systems, and higher education institutions. Decades of successful engagements have earned the company deeply entrenched relationships within its core end markets. While these industries are not typically associated with rapid growth, Huron’s value proposition is squarely aimed at helping organizations navigate an unrelenting stream of business model, regulatory, and technology challenges – pressures that have only intensified. Because these institutions tend to operate with lean internal resources, they consistently rely on outside expertise to work through complex issues, creating a durable and recurring source of demand for Huron’s services. Management sees a substantial opportunity to deepen penetration within the existing customer base over the coming years, and the company’s strategy of broadening its capabilities – both organically and through tuck-in acquisitions – should drive further wallet share gains. In aggregate, we believe Huron can grow its top line in the low double digits annually, comprised of mid-to-upper single-digit organic growth supplemented by a modest contribution from M&A. Combined with a commitment to margin expansion and a consistent track record of share repurchases, we see a credible path to low-to-mid teens earnings per share growth on an annualized basis. Concerns about AI disrupting the consulting model have pressured Huron’s valuation and weighed on the shares. We believe this risk is largely misunderstood. Huron views AI as a revenue opportunity – one it is already pursuing by helping clients develop and implement AI roadmaps – while simultaneously leveraging the technology internally to reduce its own costs. Both efforts are underway. Further reinforcing the company’s resilience, management noted that ~ 2/3rds of 2025 revenue was outcome-based, fixed-fee, or recurring in nature, and that its highly skilled consultants delivering mission-critical work for institutions facing disruption are considerably more insulated than other consulting models. At a low-teens forward earnings multiple, we believe the shares offer compelling value relative to the quality and durability of the underlying business.

Booking Holdings Inc. (BKNG) – Large Cap/International/Global

Booking is the largest online travel agency in the world. This is a network effect business model, where Booking acts as an aggregator of supply (independent hotels) on one side and demand (leisure travelers) on the other. This aggregation of fragmented supply and demand allows them to charge a healthy commission when a user books a room, which in turn allows them to outspend all other players on customer acquisition while still earning good returns. Booking is best-in-class at digital marketing, earning the highest returns on acquired traffic of all the online travel agencies. Booking has tremendous scale and an asset-light business model, generating very high returns on capital and free cash flow. Most of their revenue is generated from independent hotels that depend on Booking not just to deliver incremental guests, but also for cross-currency payments, merchandising, and customer service. Recently, shares have come under pressure over fears that AI will displace online travel agencies. We believe these concerns are overblown. AI is unlikely to recreate Booking’s global network of hotels given the extreme fragmentation of supply and Booking’s on-the-ground sales force. Booking’s payments and customer service capabilities are also difficult to replicate, further protecting the business against new entrants. In our view, new AI tools are more likely to integrate Booking’s existing inventory and capabilities into their models, rather than recreating these features themselves. If travel research shifts from traditional search to LLMs, Booking’s historical expertise in digital marketing makes them well-positioned to win this traffic. Furthermore, AI should boost Booking’s margins through efficiencies in customer service and marketing. At a mid-teens forward earnings multiple, we believe Booking shares are attractive on both a relative and absolute basis.

IMCD N.V. (IMCDY) (IMCD NA) – International/Global

IMCD is a leading global distributor of specialty chemicals and ingredients, operating across more than 60 countries. The business benefits from a resilient foundation, with approximately 55% of sales – and an even greater share of profits – derived from life science end markets, including pharmaceuticals, beauty and personal care, food and nutrition, and home care. Specialty chemical distributors like IMCD also bring meaningful value-added capabilities to both suppliers and customers, fostering deep, sticky relationships that support attractive margins and strong returns on invested capital. While the industry enjoyed a robust period of growth in the years immediately following COVID, more recent results have been weighed down by soft end-market demand and customer destocking. We view this slowdown as cyclical rather than structural, and expect the business to return to more consistent, above-average organic growth as conditions normalize. The long-term drivers remain firmly intact: rising consumption of specialty chemicals, ongoing product innovation, and increasing outsourcing to distributors. Larger players with meaningful scale advantages are also well positioned to reinvest in their offerings and capture share from smaller competitors. This dynamic should further enhance IMCD’s organic growth profile coupled with their consistent and disciplined approach to bolt-on M&A provides an additional avenue for compounding growth. Taken together, we believe IMCD has a long and visible growth runway, with the potential to compound earnings per share at a double-digit rate over the coming years. At a mid-teens forward earnings multiple, the shares are trading meaningfully below the company’s long-term historical valuation averages. We believe that the combination of strong earnings growth and multiple expansion sets up a compelling return profile for investors over the next several years.

Thank you for your continued support of Fiduciary Management, Inc.

Fiduciary Management Inc.Small Cap Equity Composite12/31/2014 – 12/31/2024

Year Total Return Gross of Fees % Total Return Net of Fees % *Benchmark Return % Number of Portfolios Dispersion % Three Year Ex-Post Standard Deviation Total Composite Total Firm Assets End of Period ($ millions) Percentage of Firm Assets % Composite *Benchmark Assets End of Period ($ millions) End of Period ($ millions) 2015 -5.72 -6.52 -4.41 171 0.34 11.18% 13.98% $ 2,597.2 $ 21,042.9 12.34% 2016 21.65 20.65 21.31 171 0.46 12.02% 15.77% $ 2,596.0 $ 22,626.7 11.47% 2017 15.42 14.49 14.65 171 0.84 11.12% 13.91% $ 2,774.0 $ 25,322.0 10.96% 2018 -8.10 -8.83 -11.01 160 0.74 11.73% 15.79% $ 2,220.4 $ 19,833.6 11.20% 2019 27.14 26.17 25.53 119 1.83 12.44% 15.71% $ 2,415.0 $ 22,609.9 10.68% 2020 4.40 3.60 19.96 104 1.49 21.15% 25.27% $ 2,079.2 $ 16,284.2 12.77% 2021 31.74 30.77 14.82 102 0.60 21.11% 23.35% $ 2,294.9 $ 17,068.4 13.45% 2022 -4.98 -5.70 -20.40 96 0.29 22.76% 26.02% $ 2,173.9 $ 13,021.5 16.69% 2023 26.34 25.41 16.93 92 0.38 18.02% 21.11% $ 3,050.0 $ 14,729.1 20.71% 2024 11.46 10.65 11.54 93 0.23 18.11% 23.30% $ 3,616.0 $ 14,761.5 24.50%

Click to enlarge

*Benchmark: Russell 2000 Index®

Returns reflect the reinvestment of dividends and other earnings.

The above table reflects past performance. Past performance does not guarantee future results. A client’s investment return may be lower or higher than the performance shown above. Clients may suffer an investment loss.

Fiduciary Management, Inc. claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Fiduciary Management, Inc. has been independently verified for the periods 12/31/1993 – 12/31/2024. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The Small Cap Equity Composite has had a performance examination for the periods 12/31/1993 – 12/31/2024. The verification and performance examination reports are available upon request.

FMI was founded in 1980 and is an independent investment counseling firm registered with the SEC and the State of Wisconsin. The firm manages over $14.7 billion in assets of pension and profit sharing trusts, mutual funds, Taft-Hartley funds, insurance company portfolios, endowments and personal trusts. The firm includes both institutional and mutual fund business. Although the firm has participated in wrap programs, it is a separate and distinct business, and is excluded from firm-wide assets.

The FMI Small Cap Equity Composite was created and incepted in January 1980. These accounts primarily invest in small to medium capitalization US equities.

The FMI Small Cap Equity Composite reflects time-weighted and asset-weighted returns for all discretionary accounts, with a market value greater than $500,000 as of month end. A small percentage of composite assets (typically ranging from 0-5%) historically has been invested in unmanaged fixed income securities at the direction of account holders. From December 31, 1993 thru September 30, 2002 all accounts included were managed for at least one quarter, from October 1, 2002 to present all accounts were managed for at least one month. All returns are calculated using United States Dollars and are based on monthly valuations using trade date accounting. All accounts in this composite are fee paying. Gross of fees returns are calculated gross of management fees, gross of custodial fees, gross of withholding taxes and net of transaction costs. Net of fees returns are calculated net of actual management fees and transaction costs and gross of custodial fees and withholding taxes. Dispersion is calculated using the equal weighted standard deviation of all accounts in the composite for the entire period. As of 12/31/2011, the trailing three year annualized ex-post standard deviation for the Composite and Benchmark are required to be stated per GIPS®. FMI uses gross returns to calculate these.

Currently, the advisory fee structure for the FMI Small Cap Equity Composite portfolios is as follows:

Up to $25,000,000 0.85% $25,000,001-$50,000,000 0.80% $50,000,001-$100,000,000 0.70% $100,000,001 and above 0.60%

Click to enlarge

The firm generally requires a minimum of $3 million in assets to establish a discretionary account. High Net Worth individuals may establish an account with a minimum of $1,000,000, however, the firm reserves the right to charge a minimum dollar fee for High Net Worth individuals depending on the client servicing involved. The minimum account sizes do not apply to new accounts for which there is a corporate, family, or other substantial relationship to existing accounts. In addition, the firm reserves the right to waive the minimum account size and minimum annual fee under certain circumstances. A complete list and description of all firm composites and FMI distributed mutual funds are available upon request.

The Russell 2000 Index® measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 8% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Small Cap Equity composite uses the Russell 2000 Index® as its primary index comparison.

GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Policies for valuing investments, calculating performance, and preparing GIPS Reports are available upon request.

Fiduciary Management Inc.Large Cap Equity Composite12/31/2014 – 12/31/2024

Year Total Return Gross of Fees % Total Return Net of Fees % *Benchmark Return % Number of Portfolios Dispersion % Three Year Ex-Post Standard Deviation Total Composite Total Firm Assets End of Period ($ millions) Percentage of Firm Assets % Composite *Benchmark Assets End of Period ($ millions) Total Firm Assets End of Period ($ millions) 2015 -1.54 -2.16 1.38 655 0.27 9.94% 10.48% $ 14,304.1 $ 21,042.9 67.98% 2016 14.85 14.16 11.96 636 0.32 10.48% 10.59% $ 12,562.9 $ 22,626.7 55.52% 2017 19.90 19.24 21.83 628 0.32 9.70% 9.92% $ 12,722.2 $ 25,322.0 50.24% 2018 -3.07 -3.62 -4.38 540 0.29 9.85% 10.80% $ 9,901.1 $ 19,833.6 49.92% 2019 24.58 23.94 31.49 371 0.42 9.95% 11.93% $ 10,493.0 $ 22,609.9 46.41% 2020 11.32 10.70 18.40 266 0.55 17.09% 18.53% $ 8,684.6 $ 16,284.2 53.33% 2021 19.33 18.77 28.71 219 0.32 17.08% 17.17% $ 9,177.4 $ 17,068.4 53.77% 2022 -13.29 -13.71 -18.11 177 0.33 19.94% 20.87% $ 6,054.5 $ 13,021.5 46.50% 2023 21.74 21.19 26.29 158 0.30 16.78% 17.29% $ 5,616.5 $ 14,729.1 38.13% 2024 11.04 10.54 25.02 131 0.29 16.73% 17.15% $ 5,103.9 $ 14,761.5 34.58%

Click to enlarge

*Benchmark: S&P 500 Index®

Returns reflect the reinvestment of dividends and other earnings.

The above table reflects past performance. Past performance does not guarantee future results. A client’s investment return may be lower or higher than the performance shown above. Clients may suffer an investment loss.

Fiduciary Management, Inc. claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Fiduciary Management, Inc. has been independently verified for the periods 12/31/1993 – 12/31/2024. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The Large Cap Equity Composite has had a performance examination for the periods 12/31/2000 – 12/31/2024. The verification and performance examination reports are available upon request.

FMI was founded in 1980 and is an independent investment counseling firm registered with the SEC and the State of Wisconsin. The firm manages over $14.7 billion in assets of pension and profit sharing trusts, mutual funds, Taft-Hartley funds, insurance company portfolios, endowments and personal trusts. The firm includes both institutional and mutual fund business. Although the firm has participated in wrap programs, it is a separate and distinct business, and is excluded from firm-wide assets.

The FMI Large Cap Equity Composite was created and incepted on 12/31/2000. These accounts primarily invest in medium to large capitalization US equities.

The FMI Large Cap Equity Composite reflects time-weighted and asset-weighted returns for all discretionary accounts with a market value greater than $500,000 as of month end beginning January 1, 2012. From December 31, 2000 thru September 30, 2002 all accounts included were managed for at least one quarter, from October 1, 2002 to present all accounts were managed for at least one month. All returns are calculated using United States Dollars and are based on monthly valuations using trade date accounting. All accounts in this composite are fee paying. Gross of fees returns are calculated gross of management fees, gross of custodial fees, gross of withholding taxes and net of transaction costs. Net of fees returns are calculated net of actual management fees and transaction costs and gross of custodial fees and withholding taxes. Dispersion is calculated using the equal weighted standard deviation of all accounts in the composite for the entire period. As of 12/31/2011, the trailing three year annualized ex-post standard deviation for the Composite and Benchmark are required to be stated per GIPS®. FMI uses gross returns to calculate these.

Currently, the advisory fee structure for the FMI Large Cap Equity Composite portfolios is as follows:

Up to $25,000,000 0.55% $25,000,001-$50,000,000 0.50% $50,000,001-$100,000,000 0.45% $100,000,001 and above 0.35%

Click to enlarge

The firm generally requires a minimum of $3 million in assets to establish a discretionary account. High Net Worth individuals may establish an account with a minimum of $1,000,000, however, the firm reserves the right to charge a minimum dollar fee for High Net Worth individuals depending on the client servicing involved. The minimum account sizes do not apply to new accounts for which there is a corporate, family, or other substantial relationship to existing accounts. In addition, the firm reserves the right to waive the minimum account size and minimum annual fee under certain circumstances. A complete list and description of all firm composites and FMI distributed mutual funds are available upon request.

The S&P 500 Index® is widely regarded as the best single gauge of the U.S. equities market. This index includes 500 leading companies in leading industries of the U.S. economy. Although the S&P 500® focuses on the large cap segment of the market, with approximately 75% coverage of U.S. equities, it is also an ideal proxy for the total market. The Large Cap Equity composite uses the S&P 500 Index® as its primary index comparison.

GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Policies for valuing investments, calculating performance, and preparing GIPS Reports are available upon request.

Fiduciary Management Inc.All Cap Equity Composite12/31/2014 – 12/31/2024

Year Total Return Gross of Fees % Total Return Net of Fees % *Benchmark Return % Number of Portfolios Dispersion % Three Year Ex-Post Standard Deviation Total Composite Percentage of Firm Assets % Composite *Benchmark Assets End of Period ($ millions) Total Firm Assets End of Period ($ millions) 2015 -0.14 -0.82 0.33 42 0.45 9.70% 10.55% $ 263.7 $ 21,042.9 1.25% 2016 16.71 15.90 12.63 39 0.37 10.50% 10.97% $ 275.9 $ 22,626.7 1.22% 2017 18.56 17.75 20.97 35 0.35 9.66% 10.17% $ 258.8 $ 25,322.0 1.02% 2018 -5.05 -5.70 -5.42 34 0.38 10.08% 11.15% $ 212.8 $ 19,833.6 1.07% 2019 27.65 26.87 30.66 20 0.83 10.29% 12.09% $ 208.5 $ 22,609.9 0.92% 2020 7.19 6.59 20.55 21 0.49 18.11% 19.24% $ 206.6 $ 16,284.2 1.27% 2021 23.72 23.02 25.53 18 0.36 18.19% 17.79% $ 225.9 $ 17,068.4 1.32% 2022 -10.66 -11.16 -19.28 16 0.48 20.58% 21.39% $ 180.4 $ 13,021.5 1.39% 2023 19.88 19.22 25.83 16 0.30 16.54% 17.46% $ 192.0 $ 14,729.1 1.30% 2024 11.81 11.16 23.50 14 0.27 16.43% 17.58% $ 187.8 $ 14,761.5 1.27%

Click to enlarge

*Benchmark: iShares Russell 3000 ETF® (IWV)

Returns reflect the reinvestment of dividends and other earnings

The above table reflects past performance. Past performance does not guarantee future results. A client’s investment return may be lower or higher than the performance shown above. Clients may suffer an investment loss

Fiduciary Management, Inc. claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Fiduciary Management, Inc. has been independently verified for the periods 12/31/1993 – 12/31/2024. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The All Cap Equity Composite has had a performance examination for the periods 12/31/2007 – 12/31/2024. The verification and performance examination reports are available upon request.

FMI was founded in 1980 and is an independent investment counseling firm registered with the SEC and the State of Wisconsin. The firm manages over $14.7 billion in assets of pension and profit sharing trusts, mutual funds, Taft-Hartley funds, insurance company portfolios, endowments and personal trusts. The firm includes both institutional and mutual fund business. Although the firm has participated in wrap programs, it is a separate and distinct business, and is excluded from firm-wide assets.

The FMI All Cap Equity Composite was created and incepted on 12/31/2007. These accounts primarily invest in small, medium and large capitalization US equities.

The FMI All Cap Equity Composite reflects time-weighted and asset-weighted returns for all discretionary accounts. From December 31, 2007 all accounts were managed for at least one month. All returns are calculated using United States Dollars and are based on monthly valuations using trade date accounting. All accounts in this composite are fee paying. Gross of fees returns are calculated gross of management fees and custodial fees and net of transaction costs. Net of fees returns are calculated net of actual management fees and transaction costs and gross of custodial fees and withholding taxes. Dispersion is calculated using the equal weighted standard deviation of all accounts in the composite for the entire period. As of 12/31/2011, the trailing three year annualized ex-post standard deviation for the Composite and Benchmark are required to be stated per GIPS®. FMI uses gross returns to calculate these.

Currently, the advisory fee structure for the FMI All Cap Equity Composite portfolios is as follows:

Up to $25,000,000 0.65% $25,000,001-$50,000,000 0.55% $50,000,001-$100,000,000 0.50% $100,000,001 and above 0.45%

Click to enlarge

The firm generally requires a minimum of $3 million in assets to establish a discretionary account. High Net Worth individuals may establish an account with a minimum of $1,000,000, however, the firm reserves the right to charge a minimum dollar fee for High Net Worth individuals depending on the client servicing involved. The minimum account sizes do not apply to new accounts for which there is a corporate, family, or other substantial relationship to existing accounts. In addition, the firm reserves the right to waive the minimum account size and minimum annual fee under certain circumstances. A complete list and description of all firm composites and FMI distributed mutual funds are available upon request.

iShares Russell 3000 ETF® seeks to track the investment results of the Russell 3000® Index (the “Underlying Index”), which measures the performance of the broad U.S. equity market, as defined by FTSE Russell (the “Index Provider” or “Russell”). The Underlying Index is a float-adjusted capitalization-weighted index of the approximately 3,041 largest public issuers domiciled in the U.S. and its territories, as determined by Russell. The Underlying Index includes large-, mid- and small capitalization companies and may change over time. The All Cap Equity composite uses the Russell 3000 Index® as its primary index comparison. In September 2022, the benchmark was changed from the Russell 3000 Index® to iShares Russell 3000 ETF® for all periods.

GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Policies for valuing investments, calculating performance, and preparing GIPS Reports are available upon request.

Fiduciary Management Inc.International Equity Hedged Composite12/31/2014 – 12/31/2024

Year Total Return Gross of Fees % Total Return Net of Fees % *Benchmark Return % Number of Portfolios Dispersion % Three Year Ex-Post Standard Deviation Total Composite Total Firm Assets End of Period ($ millions) Percentage of Firm Assets % Composite *Benchmark Assets End of Period ($ millions) Assets End of Period ($ millions) 2015 4.24 3.46 -1.00 ≤ 5 0.00 8.14 12.46 $ 2,832.9 $ 21,042.9 13.46% 2016 11.04 10.23 1.38 ≤ 5 0.38 7.39 12.00 $ 5,946.2 $ 22,626.7 26.28% 2017 16.51 15.70 25.10 ≤ 5 0.02 7.04 11.03 $ 8,209.3 $ 25,322.0 32.42% 2018 -8.63 -9.27 -13.81 ≤ 5 0.06 7.22 10.82 $ 6,287.8 $ 19,833.6 31.70% 2019 18.11 17.29 22.03 ≤ 5 0.08 8.30 10.97 $ 7,522.0 $ 22,609.9 33.27% 2020 0.98 0.25 7.58 ≤ 5 0.27 17.52 17.63 $ 3,576.9 $ 16,284.2 21.97% 2021 15.81 14.95 11.46 ≤ 5 0.00 17.57 16.54 $ 3,541.7 $ 17,068.4 20.75% 2022 -8.51 -9.19 -14.36 ≤ 5 0.00 19.31 20.18 $ 3,291.8 $ 13,021.5 25.28% 2023 23.21 22.33 18.40 ≤ 5 0.00 13.66 17.20 $ 4,478.0 $ 14,729.1 30.40% 2024 8.48 7.69 3.50 ≤ 5 0.00 13.36 17.41 $ 4,566.0 $ 14,761.5 30.93%

Click to enlarge

*iShares MSCI EAFE ETF® (EFA)

Returns reflect the reinvestment of dividends and other earnings.

The above table reflects past performance. Past performance does not guarantee future results. A client’s investment return may be lower or higher than the performance shown above. Clients may suffer an investment loss.

Fiduciary Management, Inc. claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Fiduciary Management, Inc. has been independently verified for the periods 12/31/1993 – 12/31/2024. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The International Equity Hedged Composite has had a performance examination for the periods 12/31/2010 – 12/31/2024. The verification and performance examination reports are available upon request.

FMI was founded in 1980 and is an independent investment counseling firm registered with the SEC and the State of Wisconsin. The firm manages over $14.7 billion in assets of pension and profit sharing trusts, mutual funds, Taft-Hartley funds, insurance company portfolios, endowments and personal trusts. The firm includes both institutional and mutual fund business. Although the firm has participated in wrap programs, it is a separate and distinct business, and is excluded from firm-wide assets.

The International Equity Hedged Composite was created and incepted on 12/31/2010. This composite invests mainly in a limited number (usually between 25-40) of large capitalization (namely, companies with more than $5 billion market capitalization) foreign companies.

The International Equity Hedged Composite reflects time-weighted and asset-weighted returns for all discretionary accounts. All returns are calculated using United States Dollars and are based on monthly valuations using trade date accounting. All accounts in this composite are fee paying. Gross of fees returns are calculated gross of management fees, gross of custodial fees, gross of withholding taxes and net of transaction costs. Net of fees returns are calculated net of actual management fees and transaction costs and gross of custodial fees and withholding taxes. Dispersion is calculated using the equal weighted standard deviation of all accounts in the composite for the entire period. As of 12/31/2011, the trailing three year annualized ex-post standard deviation for the Composite and Benchmark are required to be stated per GIPS®. FMI uses gross returns to calculate these.

Currently, the advisory fee structure for the International Equity Hedged Composite portfolios is as follows:

Up to $25,000,000 0.70% $25,000,001-$50,000,000 0.65% $50,000,001-$100,000,000 0.60% $100,000,001 and above 0.55%

Click to enlarge

The firm generally requires a minimum of $10 million in assets to establish a discretionary account. The minimum account sizes do not apply to new accounts for which there is a corporate, family, or other substantial relationship to existing accounts. In addition, the firm reserves the right to waive the minimum account size and minimum annual fee under certain circumstances. A complete list and description of all firm composites and FMI distributed mutual funds are available upon request.

The iShares MSCI EAFE ETF® seeks to track the investment results of the MSCI EAFE Index (the “Underlying Index”), which has been developed by MSCI Inc. (the “Index Provider” or “MSCI”). The Underlying Index is a free float-adjusted, market capitalization-weighted index designed to measure large- and mid-capitalization equity market performance of developed markets outside of the U.S. and Canada. The Underlying Index includes stocks from Europe, Australasia and the Far East and, as of July 31, 2021, consisted of securities from the following 21 developed market countries or regions: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom (the “U.K.”). The MSCI EAFE Net Index (USD)® is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Net Index (USD)® consists of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom. It is reported in local currency and net of hedges. The International Equity Hedged Composite uses the iShares MSCI EAFE ETF® as its primary benchmark comparison. In September 2022, the benchmark was changed from MSCI EAFE Net Index (USD)® to iShares MSCI EAFE ETF® for all periods.

GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Policies for valuing investments, calculating performance, and preparing GIPS Reports are available upon request.

Fiduciary Management Inc.International Equity Unhedged Composite12/31/2019 – 12/31/2024

Year Total Return Gross of Fees % Total Return Net of Fees % *Benchmark Return % Number of Portfolios Dispersion % Three Year Ex-Post Standard Deviation Total Composite Total Firm Assets End of Period ($ millions) Percentage of Firm Assets % Composite *Benchmark Assets End of Period ($ millions) Assets End of Period ($ millions) 2020 4.88 4.09 7.58 ≤ 5 0.00 n/a n/a $ 56.7 $ 16,284.2 0.35% 2021 10.43 9.64 11.46 ≤ 5 0.00 n/a n/a $ 108.6 $ 17,068.4 0.64% 2022 -16.23 -16.84 -14.36 ≤ 5 0.30 22.12 20.20 $ 80.7 $ 13,021.5 0.62% 2023 23.72 22.90 18.40 ≤ 5 0.30 17.71 17.20 $ 112.0 $ 14,729.1 0.76% 2024 3.43 2.72 3.50 ≤ 5 0.48 17.65 17.41 $ 93.1 $ 14,761.5 0.63%

Click to enlarge

*iShares MSCI EAFE ETF®

Returns reflect the reinvestment of dividends and other earnings.

The above table reflects past performance. Past performance does not guarantee future results. A client’s investment return may be lower or higher than the performance shown above. Clients may suffer an investment loss.

Fiduciary Management, Inc. claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Fiduciary Management, Inc. has been independently verified for the periods 12/31/1993 – 12/31/2024. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The International Equity Unhedged Composite has had a performance examination for the periods 12/31/2019 – 12/31/2024. The verification and performance examination reports are available upon request.

FMI was founded in 1980 and is an independent investment counseling firm registered with the SEC and the State of Wisconsin. The firm manages over $14.7 billion in assets of pension and profit sharing trusts, mutual funds, Taft-Hartley funds, insurance company portfolios, endowments and personal trusts. The firm includes both institutional and mutual fund business. Although the firm has participated in wrap programs, it is a separate and distinct business, and is excluded from firm-wide assets.

The International Equity Unhedged Composite was created and incepted on 12/31/2019. This composite invests mainly in a limited number (usually between 25-40) of large capitalization (namely, companies with more than $5 billion market capitalization) foreign companies.

The International Equity Unhedged Composite reflects time-weighted and asset-weighted returns for all discretionary accounts. All returns are calculated using United States Dollars and are based on monthly valuations using trade date accounting. All accounts in this composite are fee paying. Gross of fees returns are calculated gross of management fees, gross of custodial fees, gross of withholding taxes and net of transaction costs. Net of fees returns are calculated net of actual management fees and transaction costs and gross of custodial fees and withholding taxes. Dispersion is calculated using the equal weighted standard deviation of all accounts in the composite for the entire period. As of 12/31/2021, 36 months of performance is not available; therefore the three year annualized ex-post standard deviation is not presented for the composite or the benchmark.

Currently, the advisory fee structure for the International Equity Unhedged Composite portfolios is as follows:

Up to $25,000,000 0.70% $25,000,001-$50,000,000 0.65% $50,000,001-$100,000,000 0.60% $100,000,001 and above 0.55%

Click to enlarge

The firm generally requires a minimum of $10 million in assets to establish a discretionary account. The minimum account sizes do not apply to new accounts for which there is a corporate, family, or other substantial relationship to existing accounts. In addition, the firm reserves the right to waive the minimum account size and minimum annual fee under certain circumstances. A complete list and description of all firm composites and FMI distributed mutual funds are available upon request.

The iShares MSCI EAFE ETF® seeks to track the investment results of the MSCI EAFE Index (the “Underlying Index”), which has been developed by MSCI Inc. (the “Index Provider” or “MSCI”). The Underlying Index is a free float-adjusted, market capitalization-weighted index designed to measure large- and mid-capitalization equity market performance of developed markets outside of the U.S. and Canada. The Underlying Index includes stocks from Europe, Australasia and the Far East and, as of July 31, 2021, consisted of securities from the following 21 developed market countries or regions: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom (the “U.K.”). The MSCI EAFE Net Index (USD)® is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Net Index (USD)® consists of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom. It is reported in local currency and net of hedges. The International Equity Hedged composite uses the iShares MSCI EAFE ETF® as its primary benchmark comparison. In September 2022, the benchmark was changed from MSCI EAFE Net Index (USD)® to iShares MSCI EAFE ETF® for all periods.

GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Policies for valuing investments, calculating performance, and preparing GIPS Reports are available upon request.

Fiduciary Management Inc.Global Composite12/31/2023 – 12/31/2024

Year Total Return Gross of Fees % Total Return Net of Fees % *Benchmark Return % Number of Portfolios Dispersion % Three Year Ex-Post Standard Deviation Total Composite Total Firm Assets End of Period ($ millions) Percentage of Firm Assets % Composite *Benchmark Assets End of Period ($ millions) Assets End of Period ($ millions) 2024 9.77 9.29 18.66 9 0.16 n/a n/a $ 7.8 $ 14,761.5 0.05%

Click to enlarge

*iShares MSCI World ETF® (URTH)

Returns reflect the reinvestment of dividends and other earnings.

The above table reflects past performance. Past performance does not guarantee future results. A client’s investment return may be lower or higher than the performance shown above. Clients may suffer an investment loss.

Fiduciary Management, Inc. claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Fiduciary Management, Inc. has been independently verified for the periods 12/31/1993 – 12/31/2024. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The Global Equity Composite has had a performance examination for the periods 12/31/2023 – 12/31/2024. The verification and performance examination reports are available upon request.

FMI was founded in 1980 and is an independent investment counseling firm registered with the SEC and the State of Wisconsin. The firm manages over $14.7 billion in assets of pension and profit sharing trusts, mutual funds, Taft-Hartley funds, insurance company portfolios, endowments and personal trusts. The firm includes both institutional and mutual fund business. Although the firm has participated in wrap programs, it is a separate and distinct business, and is excluded from firm-wide assets.

The Global Equity Composite was created and incepted on 12/31/2023. This composite invests mainly in a limited number of medium to large capitalization (namely, companies with more than $4 billion market capitalization) U.S. and foreign companies. Currency exposure is not hedged.

The Global Equity Composite reflects time-weighted and asset-weighted returns for all discretionary accounts. All returns are calculated using United States Dollars and are based on monthly valuations using trade date accounting. All accounts in this composite are fee paying. Gross of fees returns are calculated gross of management fees, gross of custodial fees, gross of withholding taxes and net of transaction costs. Net of fees returns are calculated net of actual management fees and transaction costs and gross of custodial fees and withholding taxes. Dispersion is calculated using the equal weighted standard deviation of all accounts in the composite for the entire period. Dispersion is not shown when there are five or fewer accounts in the composite for the year. As of 12/31/2011, the trailing three year annualized ex-post standard deviation for the Composite and Benchmark are required to be stated per GIPS®. FMI uses gross returns to calculate these.

Currently, the advisory fee structure for the Global Equity Composite portfolios is as follows:

Up to $25,000,000 0.60% $25,000,001-$50,000,000 0.55% $50,000,001-$100,000,000 0.50% $100,000,001 and above 0.45%

Click to enlarge

The firm generally requires a minimum of $3 million in assets to establish a discretionary account. High Net Worth individuals may establish an account with a minimum of $1,000,000, however, the firm reserves the right to charge a minimum dollar fee for High Net Worth individuals depending on the client servicing involved. The minimum account sizes do not apply to new accounts for which there is a corporate, family, or other substantial relationship to existing accounts. In addition, the firm reserves the right to waive the minimum account size and minimum annual fee under certain circumstances. A complete list and description of all firm composites and FMI distributed mutual funds are available upon request.

The iShares MSCI World ETF objective is to provide investors with a total return, taking into account both capital and income returns, which reflects the return of the MSCI World Index®. The investment policy of the ETF is to invest in a portfolio of equity securities that as far as possible and practicable consist of the component securities of the MSCI World Index, this Fund’s Benchmark Index. The ETF intends to use optimisation techniques in order to achieve a similar return to the Benchmark Index and it is therefore not expected that the Fund will hold each and every underlying constituent of the Benchmark Index at all times or hold them in the same proportion as their weightings in the Benchmark Index. The ETF may hold some securities which are not underlying constituents of the Benchmark Index where such securities provide similar performance (with matching risk profile) to certain securities that make up the Benchmark Index. However, from time to time the Fund may hold all constituents of the Benchmark Index. The MSCI World Index® is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets. The MSCI World Index® consists of the following 23 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. It is reported in USD. The Focused Global Equity composite uses the iShares MSCI World ETF® as its primary benchmark comparison. In September 2022, the benchmark was changed from MSCI World Index® to iShares MSCI World ETF® for all periods.

GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Policies for valuing investments, calculating performance, and preparing GIPS Reports are available upon request.

References *Dates attempt to capture any material pre-event impact; actual starting dates may differ. **Following the Arab oil embargo, other economic and monetary factors negatively influenced the number of days to get back to even; this event is not counted in the average. Red circled data indicate events impacted by crude oil price spikes.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

GIPHY App Key not set. Please check settings