georgeclerk

Introduction

Regional banks have been hit pretty hard during the current rate-tightening cycle, in particular with the SVB fallout. Many investors like myself are expecting a meaningful turnaround in 2024 as US regional banks started to see easing off from the pressure to pay up to keep depositors from leaving.

First Financial Bankshares (NASDAQ:FFIN) is a regional commercial banker operating in Texas, a state that sees the fastest growing population in recent years. FFIN is one of my top picks for regional banks. The excellent track record of dividend growth and recent earning records during the tightening cycle have been the main attractions. FFIN has very small exposure to the office assets. So it should be fine from any immediate impacts of FED rate-cut delay. I’m actively monitoring FFIN and looking for buying opportunities during any market dips.

TOP dividend growth regional bank player in the state with fastest growing population

Historically, the regional banking industry is known for having good companies with strong dividend growth history. It is particularly true for the states where the local economy is doing better. The state of Texas is one of these states that are experiencing strong economy growth, benefited mainly from new people moving into the state. In fact, Texas is the fastest growing state in the nation according to USA today.

Texas First Financial Bank is a community bank that operates 80 branches across the state of Texas. Thanks to the population growth tailwind, the bank has done very well up until the FED rate hiking started, and more severe headwinds emerged from the regional bank crisis in early 2023.

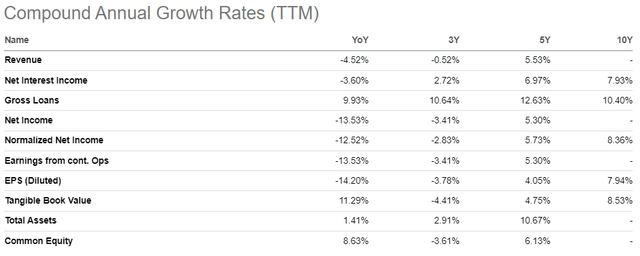

The following table provides a good snapshot of First Financial Bank business (growth).

FFIN Growth Metrics from SA

The 5-year revenue of 5% is decent considering that the last year was at -4.52%. The net interest income grows faster with 6.97% average rate over the last 5 years, again that included the 1-year negative -3.6%. Loans continue to grow at a rapid pace, with double-digit 10.40% on the 10-year average. Even year-over-year shows a respectable 9.93% increase. The total assets have grown at an impressive average of 10.67% for 5 years.

Notice the income & earning slow-downs in the YoY metrics. Part of the reason for the profit drop was the higher rates to keep deposits, which is the primary source of funding for smaller banks like First Financial. Looking forward, depositors are less likely to flee mid-sized lenders than they were following the banking turmoil of 2023. I believe the profit margin should be improved going forward that could lead to a meaningful recovery for the profit growth.

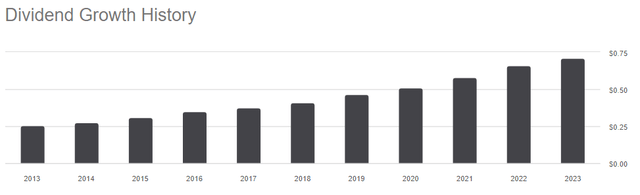

FFIN pays a 2.40% dividend at the moment, which is higher than the broad market average. What attracts me the most is its excellent dividend growth history, as shown below:

FFIN dividend growth last 10 years from SA

To me, a steady dividend growth over 10 years is the most reliable proof of a well-executed operation in a profitable business.

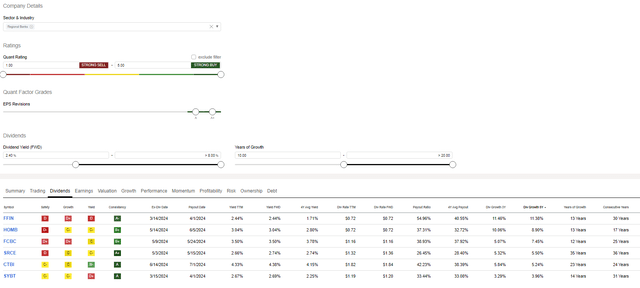

Picking up banks stocks based on the fundamentals from bottom up has not been easy for me because there are hundreds of regional banks to choose from. My favorite approach is to use dividend growth history as NorthStar indicator. I’ve found FFIN sitting at the top of the list by following my selection process based on the tools available from Seeking Alpha:

Top Regional Banks Stocks EPS rev & Div Growth SA filter

The process is summarized as follows:

Starting from top regional bank list per Top Regional Banks Stocks | Stock Screener. There are 264 regional banks in the list. The next comes the EPS revisions. I believe the good EPS rev will show me how well the company is operating in the current conditions of a rate tightening cycle. With a restrictive selection of A and A+, there are 37 left. The next step is to focus on the dividend. I prefer a dividend to be higher than the market, so I use 2.4% yield, which is higher than SPY 1.6%. There are 24 such companies with a dividend higher than 2.4% I use dividend growth as a NorthStar indicator for companies of consistent quality. I’m more comfortable with growth years at least 10. This leaves me only 6 companies. Sort the list with 5-year growth rate from high to low. The top one is FFIV. FFIV actually sits on top, beating the rest in both 3-year growth and 5-year growth rate.

Is FFIN a buy right now?

FFIN is not really a cheap stock by any means in the banking sector. Historically, FFIN has enjoyed a good premium. It still carries a forward PE ratio 20.34 even now, which is higher than 10.14 sector median. For price sensitive investors, watching dips during the current volatile market could be a more sensible strategy to pick up some shares.

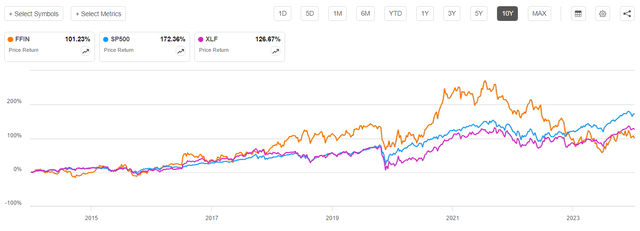

Market price behavior also suggests FFIN has been stuck in a bottom area (below $32) for sometime after outperforming both SPY and the sector index XLF handily as shown in the chart below. Shaken by the recent FED rate-cut hesitation in 2024, FFIN may not get out the price range soon. However, I believe as soon as the FED rate-cut hits the wire, I expect FFIN to take off very nicely and back to its glory days.

FFIN price chart in last 10 year with SPY and XLF

Keep in mind also that small-cap stocks are due for a rebound after lagging behind the big cap market for quite some time. This rebound will serve as a strong tailwind to FFIN when the quality small-cap stocks return back to investor’s favorite list.

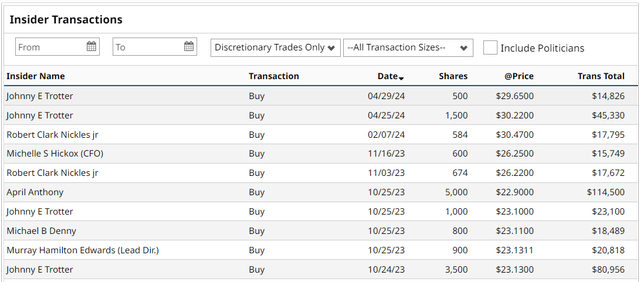

Insiders are pretty bullish on the stock. The following shows quite some buy interests from insiders in the last 6 months or so:

FFIN insiders recent buys from bartchat.com

Notice the most recent insider buys happened just a few days ago. I plan to follow the lead and open an initial long position for my dividend growth portfolio.

Risks and Caveats

One of the key risks is the US inflation. There are signs that the inflation could creep up. So the FED has to keep the interest rate “higher for longer”. The bank would have to continue or even increase the pay up for the deposits. This would hurt profit margin and lead to a sustained price slump for the stock.

The other key risk is that the US economy is not completely out of wood from a recessionary hard landing. A recession will definitely hurt the banking business on the loan side together with other business activities.

There is also a market risk for FFIN stock multiples. The market sentiment may favor the low evaluation stocks. It could put pressures on the FFIN stock price (with the built-in premium) and leave it behind for a sustained time period.

Conclusion

First Financial Bankshares (FFIN) is a regional commercial banker operating 80 branches in Texas. It is a well operated community bank with an excellent dividend growth track record that is the main driver for the stock outperformance until the rate-hiking and the regional bank crisis. There is an opportunity for dividend growth investors right now to collect some shares for regional bank recovery. I believe the FFIN will continue to benefit from the fast-growing population in Texas and resume its business growth pattern in the future.

GIPHY App Key not set. Please check settings