Matteo Colombo

Investment Summary

We are currently exploring the more obscure pockets of the market in search of selective opportunities for the next 3-5 years. The movies and entertainment industry is one such domain.

Madison Square Garden Sports Corp. (NYSE:MSGS) is a personal favourite (note I didn’t say personal “investment” favourite), hosting numerous high-value tickets at its famous Madison Square Garden. I have long been enamoured by the many sports and entertainment events run at this oracle every year. But this is a classic case of where emotions and investment should not mix. For all its wonders on the entertainment side, my excitement is dampened when examining MSGS’s fundamental economics.

As I will demonstrate here, MSGS has 1) tremendously inefficient capital turnover and 2) equally slack operating margins, which produce 3) little-to-no earnings relative to capital invested in the business. As a result, there is often very little free cash left over “at the end of the year.” In other words, MSGS isn’t throwing off the free cash flow that would suggest management could unlock substantial value in the future.

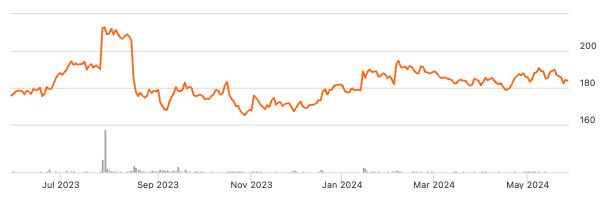

MSGS share price evolution – trailing 12 months.

Seeking Alpha

Based on my appraisal of the company’s fundamentals and its standing in the industry, I believe there are more selective opportunities elsewhere. Rate hold.

Background fundamentals

The company owns and operates a valuable portfolio of sports assets, including the NBA’s Knicks and the NHL’s Rangers. Its primary income sources include 1) ticket sales, 2) suite rental fees, 3) distributions from NHL and NBA contracts, 4) sponsorships, and 5) food + beverage sales.

Revenue is strongly influenced by the above teams’ performance. The equation is simple: 1) strong team performance leads to 2) increased demand for tickets, hospitality, and merchandise, and 3) enhanced sponsorship opportunities. Playoff qualifications also drive higher attendance and in-game spending.

Revenues have been lumpy over the years. In 2014, the company booked $913 million in sales on a loss of $117 million. In 2017, sales were $1.3 million, but they had reduced to $730 million by 2019. In 2023, the company did $887 million in sales on earnings of $46 million, its second-highest result in a decade.

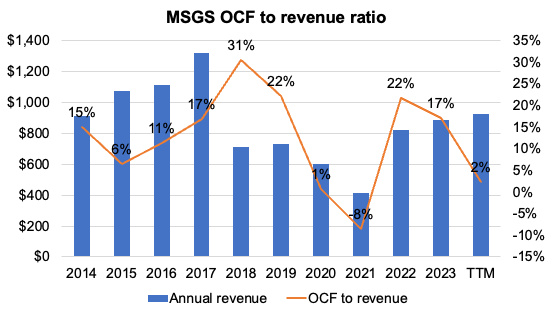

Growth isn’t a factor in the equation. So, business returns and cash flow should be – if this is a name worth buying. Figure 1 shows the company’s annual operating cash flow to sales ratio, calculated by dividing the operating cash flows by revenues on an annual basis. Revenues have been cyclical as seen, but cash flows produced from business operations have not surfaced above 22% of sales since 2019. In the last 12 months, cash flows as a function of revenues are just 200 basis points.

Figure 1.

Company filings

Industry Outlook

The movies and entertainment market is expected to grow at a high pace over the coming decade. Forecasts project a compounding growth rate of 7.3% per year over this time. Additional research projects an 8.1% compounding growth rate into 2030. Tailwinds behind this high growth include 1) investments made by digital content and distribution platforms and 2) the rise of video and content streaming platforms. This has enabled companies within the space to focus on more regional content, to drive penetration in niche markets.

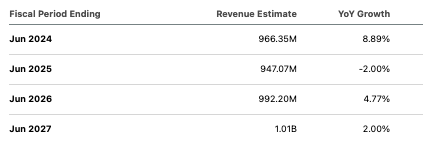

In my opinion, MSGS is not well-positioned to benefit from this growth. For one, consensus estimates project around 9% sales growth this year. However, it sees this contracting sharply in 2025 and 2026, respectively. Looking over the next three years to 2027, the median growth estimate is less than half that of the industry’s projected growth rate.

In that vein, it is not unreasonable to expect that MSGS might lose market share in this time, which would, in my estimation, clamp its already embattled top line.

Figure 2.

Seeking Alpha

Q1 FY’24 insights

A good sign is that both of the company’s core assets outside of The Garden – that is, its NBA and NHL assets – were in the play-offs this year. This is critical for the company to maintain a level of growth in ticket sales and merchandise.

The CEO echoed this in his remarks:

“Our third quarter results reflect solid operating performance across our business, driven by ongoing enthusiasm for the Knicks and Rangers, as both teams concluded successful regular seasons and qualified for the playoffs.”

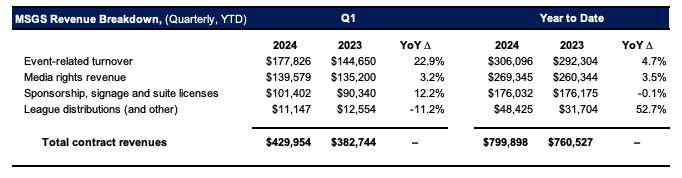

The company did $430 million of business during the first quarter of ‘24, up 12% year over year (Figure 3). Higher ticket sales, coupled with strong growth across the portfolio, underlined growth.

As to the divisional revenue breakdown (Q1, and YTD):

Event-related turnover was up 23% year-on-year to $177.8 million, whereas it clipped 12% growth in revenue sponsorship and suite licenses.

For the year to date, sales in these segments were up 4.7% and down 0.1% year over year, respectively. It is unclear how much of this was price vs. demand.

Figure 3.

Company filings

The direct operating expense margin as a percentage of sales was ~63%, producing operating income of $79 million (18% pre-tax margin). By the end of Q1, it had $58.8 million of receivables due from customers, up from $20.1 million this time last year. It also recognized contract assets with maturity less than 12 months of $64.7 billion, a large step up from the $19.5 million booked last year. The balance sheet contains ~$118 million in deferred revenue, which is sales booked without any transfer of goods or services.

My view of MSGS’s Q1 2024 earnings is that they were largely in line with expectations. No data points stood out to me. In fact, it would have been a relatively flat year, had both of its sporting assets failed to make the play-offs.

Fundamental economics

One of the main draw-cards of this industry is the low intensity of tangible assets as a percentage of total capital. Assets such as licensing, royalties, sponsorships, and other intangible means often make up the asset structure, meaning incremental capital requirements are often relatively low compared to other industries.

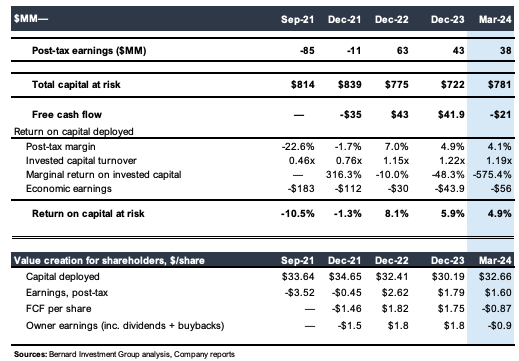

The benefit of this is that it could increase the dollar returns that movies and entertainment businesses can produce for their investors. This is not the case for MSGS, in my judgment. As seen in Figure 4, the company has around $781 million of capital at work in the business today. This is actually down over the testing period. In 2022, it produced a negative return of 1.3% on capital of $840 million. It did 6% on $722 million operating capital in 2023, and just 5% in the 12 months to March 2024.

These are abysmal numbers for a company that should be collecting large operating profits from its base due to the factors mentioned above. I would have presumed MSGS would possess consumer advantages thanks to its branding. This is not the case, however, and the return drivers immediately explained why.

This is a company operating on less than 5% post-tax margins while turning over its capital around 1.2x each rolling 12-month period. This is both inefficient and unprofitable. It tells me the company’s underlying assets do not produce a decent rate of earnings when measured against the investment required for them. We look for our equity evaluations to produce a 12% return at the minimum. MSG certainly does not fit the bill.

As a result, it hasn’t thrown off piles of free cash flow to 1) shareholders or to 2) reinvest for growth. This company doesn’t pay dividends but retains all earnings from shareholders each year. Free cash flow has been lumpy, with a $21 million outflow in the last 12 months, not acceptable given the return and invested capital of about 5%. Management is deploying capital at a disadvantage, in my opinion.

Figure 4.

Company filings

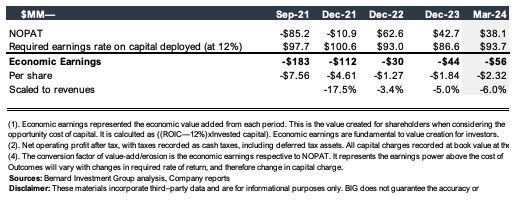

For context as to what this means in the investment sense, Figure 5 illustrates what the company needed to produce in earnings to create economic value to us. Economic value is defined as any dollar or percentage of earnings that are above the 12% threshold margin. Think of it like giving a fund manager capital to work with, and benchmarking this against a 12% hurdle rate—which, by the way, is the long-term average of the broad indices.

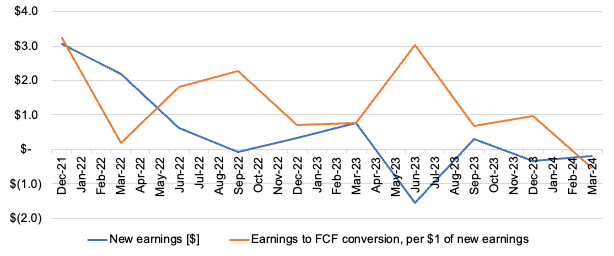

In 2023, management needed to produce $86.6 million in net operating profit after tax on capital of $722 million. It did around half that amount at $42.7 million, meaning the economic loss was $44 million. So even though there was an accounting profit of $46 million 2023, this was an economic loss when put against our stipulated hurdle rate of 12%. This is further exemplified in Figure 6, illustrating both 1) the decline of earning growth and 2) management’s results in rotating earnings into free cash flow. Both have been relatively low for my standards.

This isn’t a new trend, either. Since 2021, the company has generated an economic loss of $19.60 per share. I’m therefore unsurprised to see MSGS trading below its May 2019 average range of around $200 per share. This section of analysis corroborates a neutral view and suggests that management needs to grow that return on invested capital to unlock value for shareholders going forward.

Figure 5.

Company filings

Figure 6.

Company filings

Valuation

The company sells exorbitant multiples of both earnings and net assets. It currently trades at 185x trailing earnings and 68.2x EBIT. It is also priced more than 7x EV/invested capital.

It is tremendously hard to believe MSGS can work itself into these multiples. For instance, the P/E is more than 900% premium to the sector. This is for a company whose earnings have been lumpy at best, and contracted sharply from $5.99 per year in 2018 to $1.00/share in the trailing 12 months. Earnings are forecast by consensus to increase by 23% this year, only to lift by 35% the year after—but this is misleading because it would be off such a low base.

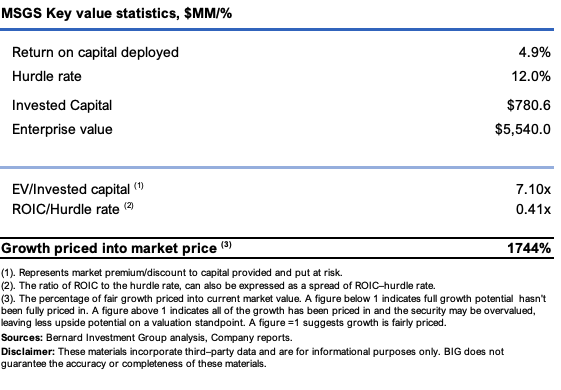

To get a cleaner picture of how the market has priced MSGS and what may be under-captured, I have compared the company’s EV/invested capital multiple to the ROIC/hurdle rate multiple as a kind of “no growth” ratio. Enterprise value is the market value of capital employed, whereas invested capital is the book value of the same, so this is a fair comparison to make. If management rolls out another 5% return on invested capital of $780 million, my estimate is the company is tremendously overvalued and has far too optimistic projections priced into its current market capitalisation.

Figure 7.

BIG estimates

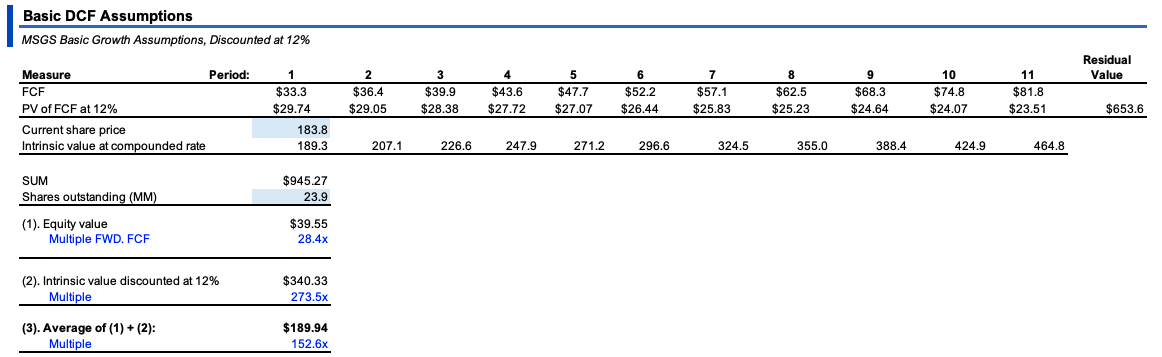

To quantify this, I will turn to Figure 8 and Figure 9. The first illustrates my projections at MSGS’s steady state of operations over the next 10 years. This assumes no change to its current trajectory—that is, recent growth rates, operating margins, and investments required to maintain competitiveness and growth. I then discount these estimates at the 12% threshold margin to arrive at a fair value figure.

This gets me to an implied valuation of around $189-$190/share, roughly in line with where MSGS trades today. Again, this supports my neutral view. As further evidence, most of the projected value lies in the “continuing value”., That is, after the 10-year forecast.

Figure 8.

BIG estimates

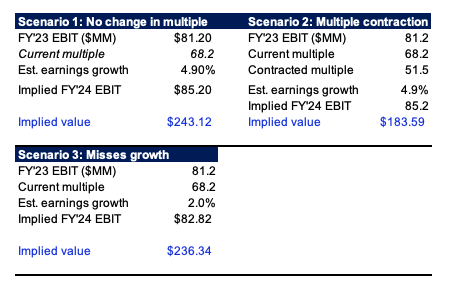

Secondly, a 68x trailing pre-tax multiple is extremely susceptible to contraction. It hasn’t been earnings growth driving this multiple or the share price, as I’ve discussed previously. Therefore, it does appear to be primarily the multiple driving the stock price – or at least holding it at current levels.

I’m going to run the scenario where management does hit my estimated growth targets of 4.9% in pre-tax income this year. If investors continue to pay the 68 times multiple, the company would be worth $243 to me today.

Similarly, if it didn’t hit the growth figures and clips 2% great instead, then at the same multiple, the company is worth $236 per share. But if the multiple contracts sharply – and it could, in my view – to say 51.5 times, even if the company hits the stipulated growth rates, the valuation implied reduces to $183. Even if it gets to 10% in earnings growth, if the multiple contracts to that mark, I get to a valuation of $192 per share. This clearly demonstrates how susceptible the share price is to the multiple contraction, and that most of its current valuation is tied up in the multiple investors are paying rather than the fundamentals of the company.

Figure 9.

BIG estimates

In short

Companies within the entertainment industry often benefit from attractive economics that enable 1) high reinvestment of cash flows and 2) incremental earnings growth with each capital allocation decision. Because of the industry tailwinds, it is up to management to bring out each individual company’s competitive advantages.

My judgment is that MSGS will continue to struggle on the chart, given (i) its unattractive economics and (ii) underlying assets that are neither productive nor profitable. I get to a valuation of $189 per share on a discounted cash flow basis, but estimate the stock could trade at around $183 per share in the event of a sharp multiple contraction. In short, rate hold.

GIPHY App Key not set. Please check settings