Nvidia (NVDA 3.99%) is the largest company in the world, and by a large margin. Second-place Alphabet (GOOG 0.61%) (GOOGL 0.85%) sits at a $4.5 trillion market cap, while Nvidia hovers around $5.1 trillion. That $600 billion gap is massive, equivalent to the size of Visa.

With Nvidia being the largest company in the world, some investors would consider the stock expensive. However, after breaking down its growth potential and current stock price, I think it’s clear that Nvidia’s stock is a great bargain here. Although it’s already the largest company in the world, Nvidia could easily grow even larger over the next few years.

Image source: The Motley Fool.

The AI build-out is still picking up steam

Nvidia’s success and the artificial intelligence (AI) arms race go hand in hand. Nvidia’s GPUs are the top computing option for AI workflows and have remained so even after some powerful custom AI chips have made their way to market. The universal nature of Nvidia’s product makes it a popular choice, and its raw performance cements its position at the top of the marketplace. The question is, how much bigger can AI spending get?

Today’s Change

(-3.99%) $-8.33

Current Price

$200.32

Key Data Points

Market Cap

$5.0T

Day’s Range

$200.02 – $203.78

52wk Range

$145.50 – $236.54

Volume

4.8M

Avg Vol

162.2M

Gross Margin

74.15%

Dividend Yield

0.13%

In 2026, the AI hyperscalers amazed investors by announcing a record-setting $650 billion in data center capital expenditures. Next year, Nvidia claims that figure will be $1 trillion or more. Nvidia likely has order information on what the AI hyperscalers are doing in 2027, so investors would be wise to trust this projection. It also suggests Nvidia should see significant growth again in 2027, making today’s stock price seem cheap.

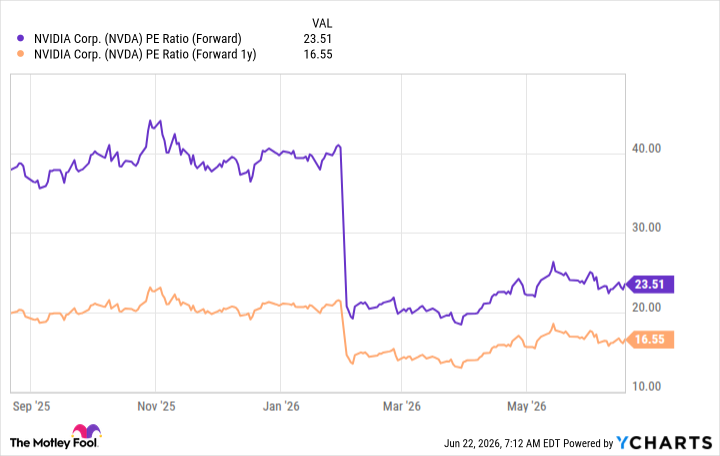

Right now, Nvidia trades for 23.5 times forward earnings, which is barely more expensive than the S&P 500 at 22 times forward earnings. With those two priced at the same level, the market is essentially saying that beyond 2026, Nvidia will not grow at a market-beating pace.

NVDA PE Ratio (Forward) data by YCharts

But projections show this isn’t true. So, this opens up a great investment opportunity. The market hasn’t priced in any of Nvidia’s anticipated 2027 growth yet, and if it’s anything like Wall Street predicts, it could be another huge year. Wall Street analysts expect Nvidia’s revenue to grow at a 41% pace next year. If Nvidia’s stock gains are tied to its business growth (which they should be), then there is major upside ahead for Nvidia’s stock, and investors should consider loading up on it as a result.

Keithen Drury has positions in Alphabet, Nvidia, and Visa. The Motley Fool has positions in and recommends Alphabet, Nvidia, and Visa. The Motley Fool has a disclosure policy.

GIPHY App Key not set. Please check settings