sitox

Invesco Large Cap Growth ETF (NYSEARCA:PWB) was launched on March 3, 2005 and is managed by Invesco Capital Management LLC. It offers exposure to large-cap U.S. stocks with capital appreciation potential.

Though since its inception, PWB has accumulated $815 million in AUM and boasts a sophisticated approach to selecting stocks, it hasn’t done much better than the broad market and has underperformed competing ETFs in the long run. For this reason, the fees charged here are unreasonably high and investors may be better served to pick any of the alternatives mentioned in this article.

Methodology

First, let us take a look at the general approach of the fund to create its portfolio. PWB tracks the Dynamic Large Cap Growth Intellidex Index which aims to compile around 50 large-cap stocks with strong growth attributes. Here’s a broad overview of the selection/management process of the index:

It begins with an available universe of the 2,000 largest (based on market cap) and most liquid stocks trading on NYSE, NYSE American, and NASDAQ. Then it narrows it down to 50 stocks, of which 15 receive 50% of the total weight based on scoring the best model score used by the index provider. The index rebalances and reconstitutes quarterly.

The model score I mentioned refers to what the index provider calls a Style Score, which is calculated by subtracting the Growth score of a candidate from its Value score. Specifically, if the result is strongly positive, then the candidate’s Style is growth and if it’s strongly negative, then it’s Value. If the Growth and Value scores are more or less the same, then the candidate stock is not considered at all.

Now, the Growth score is the sum of the following factors: long-term projected earnings growth (50% weight), earnings growth (12.5% weight), sales growth (12.5% weight), cash flow growth (12.5% weight), and book value growth(12.5% weight). And the Value score is calculated by summing these factors: price/forecast earnings (50% weight), price/book ratio (12.5% weight), price/sales (12.5% weight), price/cash flow (12.5% weight), and dividend yield (12.5% weight).

The methodology is surely sophisticated, and that may somewhat justify the high fees PWB charges.

Allocations

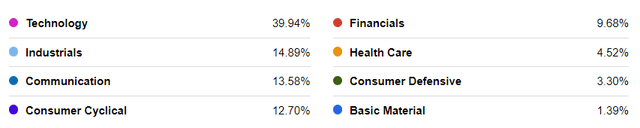

Next, let’s view how this fund is allocated. First, PWB doesn’t have concentration limits as it’s evident from its ~40% allocation to Tech stocks:

Seeking Alpha

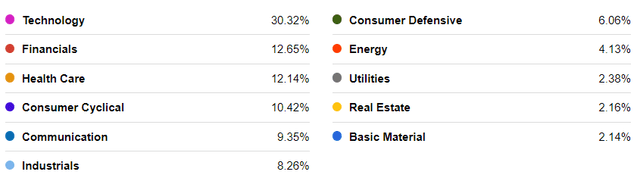

Below, you can see the current sector allocations of the SPDR S&P 500 ETF Trust (SPY), which are quite different:

Seeking Alpha

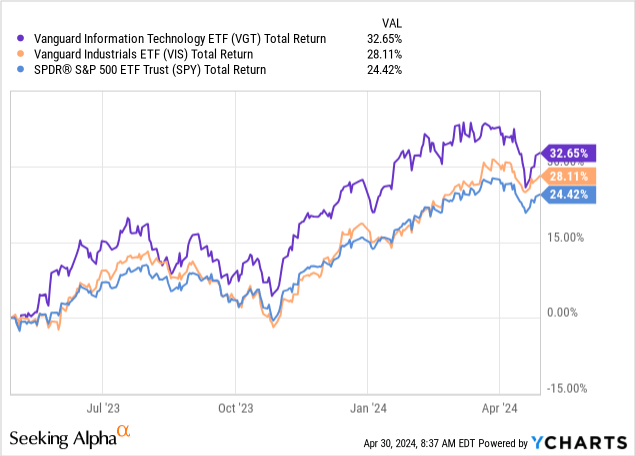

A tilt toward tech stocks makes sense as they often exhibit the growth characteristics growth ETFs generally look for. In the last 12 months, the Technology and Industrials (second biggest allocation of PWB) sectors have outperformed the broad market:

Data by YCharts

Data by YCharts

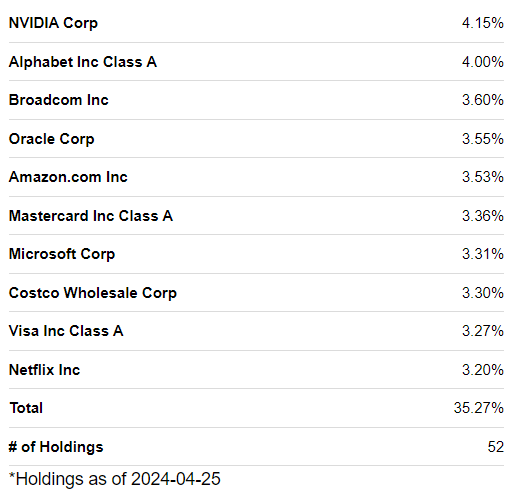

Now, even though the index normally gives 50% of the weight to only 15 out of 50 constituents, the fund is currently better diversified as you can see from its top 10 holdings comprising 35.27% of the portfolio below:

Seeking Alpha

All of the above holdings are big names, and it’s interesting to see how they will help the fund when it comes to future performance. But first, let’s see what results the ETF’s approach has yielded so far.

Performance & Cost

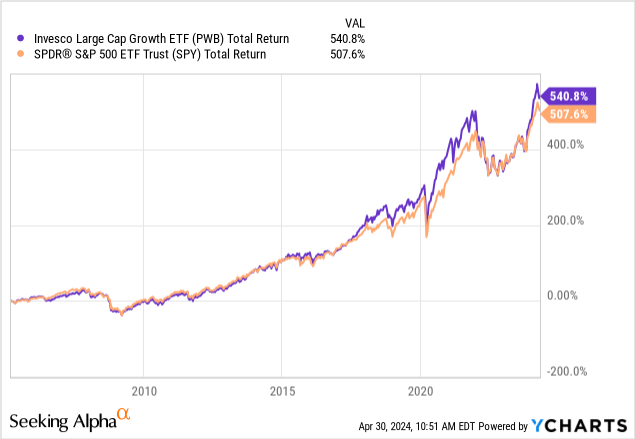

Since the fund was launched in 2005, it has outperformed SPY by a small margin:

Data by YCharts

Data by YCharts

But due to the very long period involved, that can seem, of course, meaningless for most investors. The ETF grew at a compounded annual rate of 10.57%; not much higher than 10.24% for SPY.

For this reason, PWB doesn’t seem to be a good alternative to a vanilla approach; nor does it make sense as a diversifier since it will probably overlap with any large-cap U.S. portfolio.

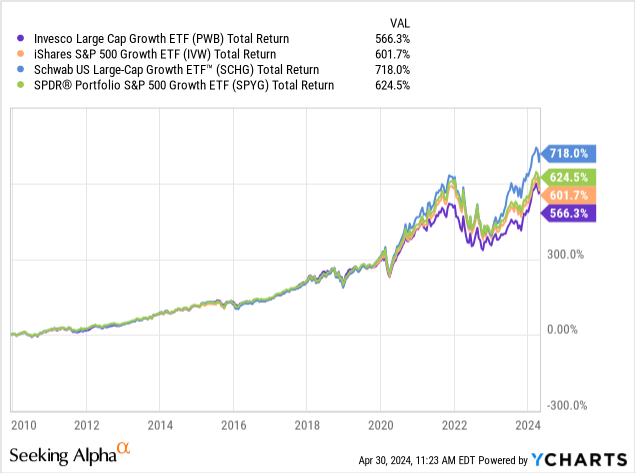

Moreover, all of its largest competitors have done a lot better, with the Schwab US Large-Cap Growth ETF (SCHG) leading the way:

Data by YCharts

Data by YCharts

And that’s interesting because SCHG is generally a lot more diversified than PWB (currently holding around 250 stocks). The expense ratio must have something to do with it, as SCHG has one of 0.04% and PWB charges 0.56%; the difference is huge enough to be reflected in the performance differential given enough time.

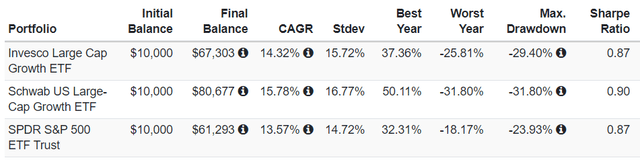

Moreover, SCHG has done better on a risk-adjusted basis, as reflected in its higher Sharpe:

portfoliovisualizer.com

Risks

So the primary risk here is the potential underperformance when compared to competing ETFs. The risk that comes with a potentially higher volatility due to the relatively concentrated portfolio is secondary.

Verdict

All in all, it appears that when it comes to large-cap growth, there doesn’t seem to be a better choice than SCHG and a worse choice than PWB. For this reason, I am rating PWB a hold. Investors are better off with a much cheaper ETF that offers large-cap growth equity exposure.

What’s your opinion? Do you own any of these ETFs? Leave a comment below and let me know! Thank you for reading.

GIPHY App Key not set. Please check settings