SweetBunFactory

Earnings season is upon us and will be very important in assessing if the iShares Semiconductor ETF (NASDAQ:SOXX) is priced right. This ETF is flat for July and has just made its largest drop since April, but it still has a one-year gain of 46% gain and a P/E ratio of 36. It appears some holders are getting nervous and selling before the numbers are out.

A Closer Look at SOXX

SOXX was launched in 2001, way before the current AI craze and just after the internet bubble popped. Its performance between inception and 2013 was unimpressive as it first crashed and then took 12 years to break back above its launch price. This period weighs on its long-term performance statistics.

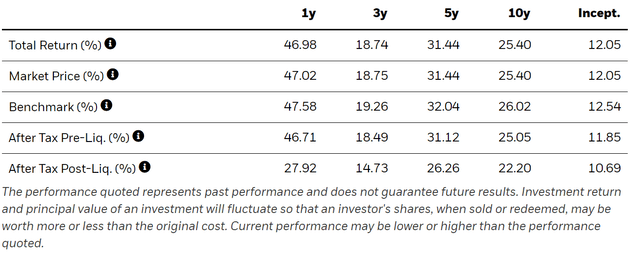

Returns (iShares)

The 1-yr and 5-yr returns are much more impressive, obviously due to the demand for chips in AI and cloud services.

As the fund page statesSOXX provides exposure to “U.S. companies that design, manufacture, and distribute semiconductors.” It is a passively managed fund which has a simple composition. According to the prospectusthe underlying Index is made up of:

… the 30 largest U.S.-listed companies that are classified according to the ICE Uniform Sector Classification schema within the semiconductors industry (as determined by ICE Data Indices, LLC or its affiliates (collectively “Index Provider” or “IDI”)). Constituents must also meet other eligibility criteria determined by the Index Provider, including minimum market capitalization and liquidity requirements.

Interestingly, SOXX does not use a simple market capitalization weighting method which means NVIDIA Corporation (NVDA) is not its largest holding.

Top 10 Holdings (Seeking Alpha)

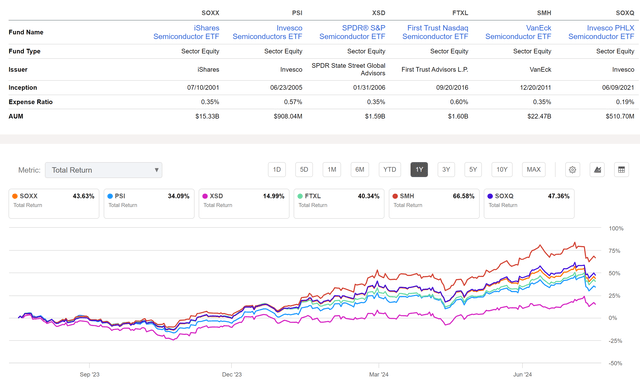

This has weighed on its performance. For comparison, the VanEck Semiconductor ETF (SMH) has a ~20% weighting in NVDA and is the best-performing ETF in this space as a result.

Peer Comparison (Seeking Alpha)

SOXX compares favorably to the rest of its peers and the 0.35% expense ratio is average. $15B and ample liquidity are other attractions.

The Numbers are Still Impressive

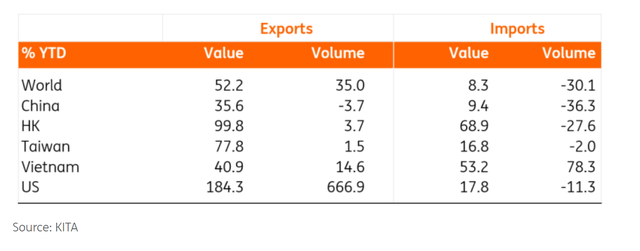

Semiconductors have had an amazing run since the 2022 low and the numbers continue to improve. The graphic below shows South Korean chip exports for H1 2024.

South Korea Exports (ING)

SK Hynix – the second-largest memory chipmaker – had been the sole supplier of its High Bandwidth Memory (HBM) to NVIDIA until March, which is known to command about 80% of the AI chip market. SK Hynix announced that its HBM chips used in AI chipsets were sold out for this year and almost sold out for 2025 (as of May 2024) as businesses aggressively expand their artificial intelligence services.

Source: ING July 22, 2024.

Big technology companies continue to ramp up their AI capabilities and Alphabet Inc. (GOOG), (GOOGL) just announced they expect CapEx “at or above the Q1 CapEx of $12 billion.” Microsoft Corporation (MSFT), Meta Platforms, Inc. (META), Apple Inc. (AAPL) and Amazon.com, Inc. (AMZN) are all committing large sums to build AI infrastructure, which is great news for semiconductors, especially NVIDIA Corporation (NVDA).

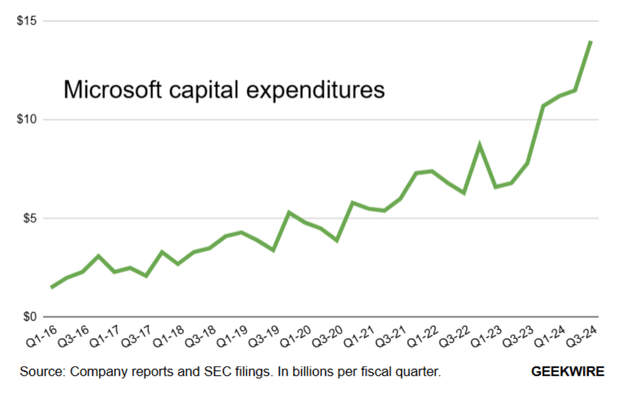

Microsoft Corporation (MSFT) is the biggest spender and is an important company to monitor. The last earnings release revealed CapEx increased 79% to a record $14 billion and the company plans to increase this into fiscal 2025 (which starts in July).

MSFT CapEx (Geekwire)

While this is all clearly positive for SOXX, we do have to wonder where it all ends and if this growth will be sustainable.

Developing Headwinds

There appears to be some pushback against the spending plans of big tech. Meta Platforms, Inc. (META) dropped sharply after its last earnings when it revealed plans to ramp up AI investment. GOOGL just released some great earnings figures but dropped after hours in what could be a reaction against its CapEx forecasts. The market seems to be concerned about where all this spending is leading as revenues from AI are small in comparison to the amounts invested.

While smaller companies are investing in AI, they don’t have the capabilities to build data centers and will pay to use AI services in the cloud developed by big tech. This means demand for chips will likely stay limited to mega-cap companies (and the Saudi sovereign wealth fund).

At some point, quite likely this year, investment from big tech will slow as the stockpiling of chips is concluded. Of course, they will have to continue to spend on improving and maintaining infrastructure, but 2024 or 2025 may well see the peak in investment, at least until a compelling use for AI is found. This may take years to develop and will likely drive the next cycle of investment.

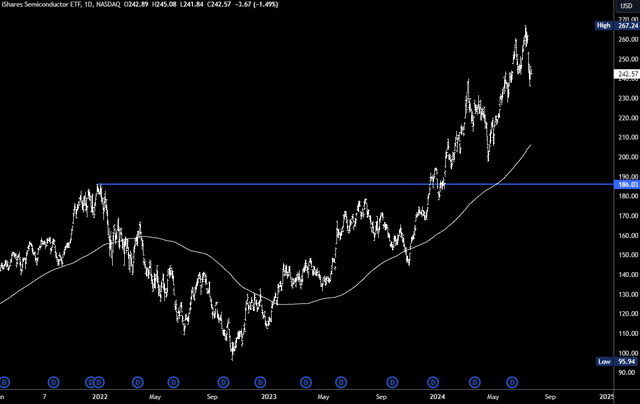

Technicals

As mentioned in the introduction, SOXX has just experienced its largest drop since April and was over -11% at last week’s low. The July reversal does look significant and based on the technicals, there is the potential for a second drop to the 200dma which is around $210 (and rising).

SOXX Chart (TradingView)

The drivers of a drop back to the $200-$210 range likely relate to earnings season, which presents several risks. Firstly, the companies SOXX holds will have to show solid results. Secondly, the mega-cap investors will have to continue spending and the reaction to spending plans will need to be positive. The drop from $267 to the current $242 has taken some of the froth off the rally and valuation, but a longer consolidation may be needed before SOXX can rally sustainably again to new highs.

Conclusions

Semiconductors have been – and will remain – a hot sector due to AI investment. That said, growth will likely level off as big tech finishes stockpiling chips, and SOXX may need to consolidate its gains. Earnings season will be important for several reasons and the recent drop is likely due to de-risking. A reversal on the chart suggests a larger pullback may be underway and the $200-$210 region can be reached over the summer.

GIPHY App Key not set. Please check settings