imaginima

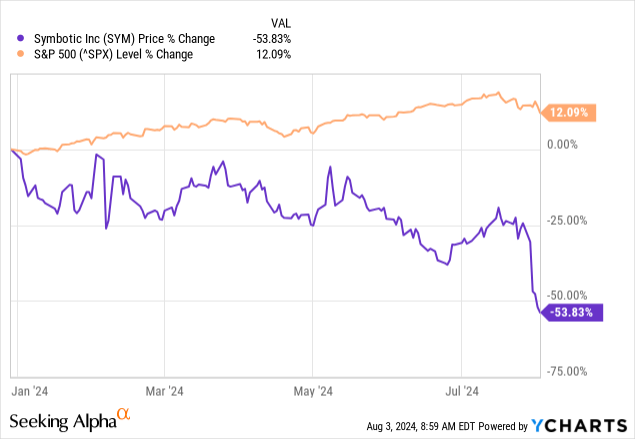

When I last wrote about Symbotic (SYM) at the end of 2023, I suggested that investors who had yet to buy the stock avoid it. The stock is a high-risk investment, and the prospects of future dilution made it a bad bet. That assessment was correct, as the stock declined 56.55% since the end of 2023 compared to the S&P 500 (SPX) rising 12.12%.

Data by YCharts

Data by YCharts

Symbotic remains a high-risk, early-stage company, so investors who err on the side of caution should still avoid this stock. However, speculative investors looking for a stock with a high upside should consider buying. After dropping significantly over the last seven months, the stock’s valuation is far more reasonable. I am upgrading the stock to a buy, but only for investors comfortable investing in high-risk stocks.

This article will discuss the Chief Executive Officer’s (“CEO”) comments at Symbotic’s 2024 Investor Day. It will also examine why the stock dropped after its recent earnings, the company’s fundamentals, risks, and valuation, and why I upgraded the stock to Hold.

Symbotic 2024 investor day

The company held an investor day on May 9, 2024. The presentation was nearly an hour and 45 minutes long, so I won’t review it all in this article. Any investor interested in investing in Symbotic should view the whole presentation on YouTube. I will only discuss some of CEO and Founder Rick Cohen’s commentary at the event.

Rick Cohen founded Symbotic in 2016 to improve operating efficiencies in modern warehouses and lower costs. The following image shows the sites where the company has already deployed its warehouse design.

Symbotic 2024 Investor Day Presentation

The following image shows the backlog of new sites outside its Greenbox program. I discussed the Greenbox, Warehouse-as-a-Service Joint Venture with SoftBank (SFTBY) (SFTBF) under the subhead “The company’s Green Box initiative” in my previous article on the company.

Symbotic 2024 Investor Day Presentation

The following image shows a map of the non-Greenbox systems within the U.S. in Green and the potential Greenbox systems from its nine current customers in white. Note that Greenbox makes Symbotic a global company.

Symbotic 2024 Investor Presentation

CEO Cohen said at the presentation that if it builds out all of the potential locations with those nine Greenbox customers, there will be four to five times more dots on the map. He also said the company intends to add one to two customers annually. Suppose those statements are factual; the above image would only be a fraction of the systems that Symbotic will deploy.

The company refers to its current system as the Brooksville system, a reference to Walmart’s Brooksville, Florida, distribution center. The company expects to have ten of those systems up and running within the next year. Each one of those systems costs hundreds of millions of dollars. At the end of fiscal 2021, the company only had $252 million in sales. At the end of fiscal 2023, it had $1.18 billion in sales. At the midpoint of fourth quarter FY 2024 guidance, the company should produce $1.75 billion in sales at the end of its fiscal year in September 2024. So, the top line is growing rapidly as the company installs more of these systems. CEO Cohen said during the investor event:

The pace of technological acceleration, the pace of adoption from Symbotic is accelerating, the pace of growth and sales for us is accelerating, the talent base is accelerating, and that’s what I’m most excited about …This will be the slowest sales year the company has for the next 50 years.

The CEO also said there is a moat around what the company is doing, and no other company is doing what it does. The moat he refers to is that its warehouse system is costly and challenging to develop—a technological moat. Most warehouse systems consist of human pickers and conveyor belts, and Symbotic’s system is a radical redesign of how a warehouse operates and stores items. Refer to my previous article on the company, which describes its warehouse platform under the subhead, “It has a unique warehouse architecture.” The company had numerous failures in developing the warehouse system, and in some cases, the CEO refunded the money back to early customers when the first systems failed to work. The system is so complex and expensive that once Symbotic installs it, switching to any emerging competitor product is cost prohibitive—a switching cost moat.

CEO Cohen also said at the event, “What we’ve created is the iOS, the platform for integrating new technology into all forms of robots.” He analogized Symbotic to Amazon’s (AMZN) early days when it was only a bookseller. Now, look at how many different products Amazon sells. Similarly, this company is now only using robotics in warehouses. In the future, it could use its robotics platform in other use cases. The CEO elaborated (emphasis added), “(In) the future…we don’t know what we are going to sell, we don’t know how big the market is, but we do know that we are so much lower cost at moving boxes than any other person-based or automation-based system anywhere in the world.” He implies that the market opportunity may be far more extensive than warehouses.

Symbotic’s fundamentals

The good news is that demand remains robust for its solutions, evidenced by the solid backlog of $22.8 billion. The bad news is that aggressively scaling up its business to meet demand has led to execution issues and construction delays that have slowed the deployment of these warehouse automation systems. When the speed of deployment is too slow, it can show up as increased Systems costs and declining gross margins if the company fails to manage these costs effectively. We will discuss Systems costs and gross margin later.

First, let’s examine the company’s issues with slowing deployments, which started earlier in 2024. Chief Financial Officer (“CFO”) Carol Hibbard said on the company’s first-quarter earnings call:

We have temporarily stabilized the pace of system deployment starts. Our future revenue growth is really driven by our ability to scale deployments and progress.

What she likely meant by that statement was that management put in some solutions to fix the issues at the root of slowing deployments and stabilized the downtrend in deployment starts. The company understands that slow deployments can negatively impact revenue growth over the long term. By the second quarter, deployment starts hit bottom and reaccelerated in the third quarter. CFO Hibbard said on the company’s third-quarter earnings call (emphasis added):

As planned, system starts reaccelerated in the third quarter. We started five new system deployments and completed three systems, bringing us up to 21 fully operational systems. We expect quarterly system starts to increase in the fourth quarter.

CEO Cohen said on the company’s third-quarter fiscal year (“FY”) 2024 earnings call (emphasis added):

As you recall, two years ago, we embarked on a strategy to outsource much of the manufacturing and installation of our systems. This approach enabled us to scale at a rapid pace. Based on our key learnings over multiple deployments, we plan to reabsorb a portion of the construction management processing starting this quarter, which will reduce costs. We believe bringing some of these functions back in-house will help us put a sharper focus on the implementation process and reduce costs further. In the short term, our revenue growth may slow as we make these changes.

The company produced revenue growth in the third quarter of FY 2024 of 58% year-over-year. So, the potential issue of slowing revenue growth did not show up in the third quarter. However, management has called for 18.6% revenue growth in the fourth quarter at the midpoint of guidance. The table below shows analysts forecast fourth-quarter FY 2024 revenue growth to drop to 19.88% before rebounding to 36.41% in the company’s first quarter FY 2025.

Seeking Alpha

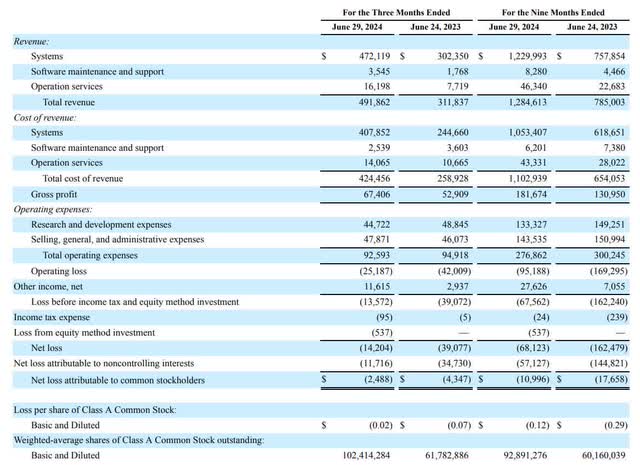

The following image shows the company’s third quarter FY 2024 income statement. While the company improved the pace of systems starts over FY 2024, the company still has issues with gross margin. Systems costs of revenue grew by 66.70%, which is around 8.7% higher than revenue growth.

Symbotic Third Quarter FY 2024 Earnings Release.

Symbotic’s third quarter FY 2024 earnings release stated:

Our system gross margin fell below expectations due to elongated construction schedules and implementation costs. We are focused on improving our planning, speed of implementation and project management to improve performance.

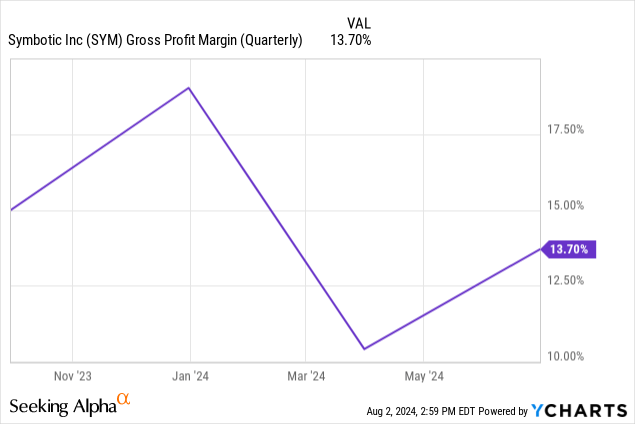

The elevated System costs in the third quarter caused the company’s gross margin to decline 325 basis points from the previous year’s comparable quarter to 13.70%. In my last article on the company, I said, “The good news is the company has structured most of its backlog on a cost-plus fixed-profit basis, which helps the company maintain its gross margin during times of high inflation or other events that could cause Symbotic’s expenses to rise.” Investors who thought they didn’t have to worry much about gross margin declines were likely to be ticked off by the performance of the gross margins in 2024.

Data by YCharts

Data by YCharts

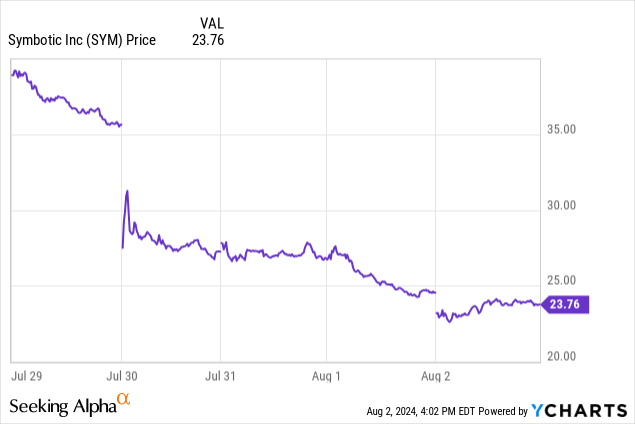

The market likely did not like hearing that revenue growth may slow or seeing gross margins compress due to execution issues. The day after the company released third-quarter earnings, the stock dropped 23.5%.

Data by YCharts

Data by YCharts

The market’s perception of the company’s actions will determine when the stock will recover. If the market sees that the company has effectively addressed its execution issues by accelerating system deployments, expanding its gross margin, and reaccelerating revenue growth, it could help the price recover.

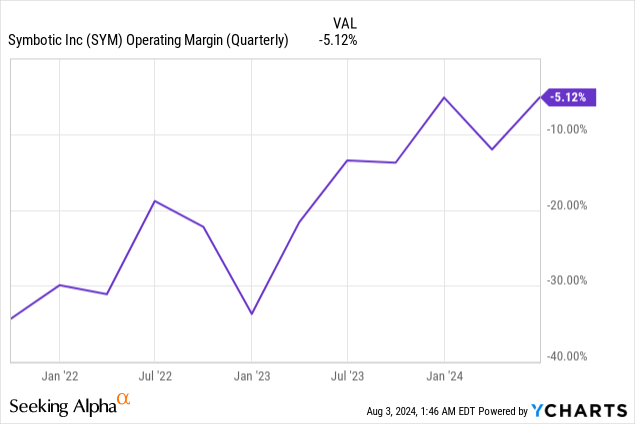

Third-quarter operating expenses declined 2.4%. CFO Hibbard said, “We continue to improve our operating leverage with focus on prudent expense management.” As a result, the company’s operating margin improved to a 5.12% loss in the third quarter.

Data by YCharts

Data by YCharts

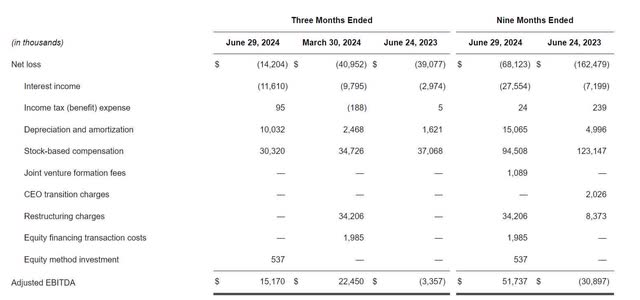

The company emphasizes non-GAAP (Generally Accepted Accounting Principles) adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) numbers as a measure of profitability. The following shows the reconciliation of GAAP net loss to adjusted EBITDA.

Symbotic Third Quarter FY 2024 Earnings Release.

Symbotic likely emphasizes adjusted EBITDA as it highlights the company’s core profitability by removing non-cash and one-time expenses. The above table shows that in the third quarter of FY 2024, EBITDA declined 32% year-over-year. The EBITDA margin decreased by approximately 420 basis points to 3.0%. Its highest expense is stock-based compensation, at around 6% of quarterly revenue.

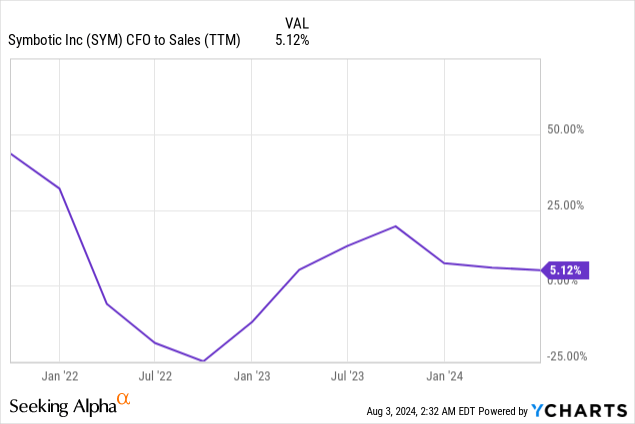

The following image shows that Symbotic’s third quarter cash from operation (“CFO”) to sales dropped to 5.12% due to the company’s execution issues. This drop hurt free cash flow (“FCF”).

Data by YCharts

Data by YCharts

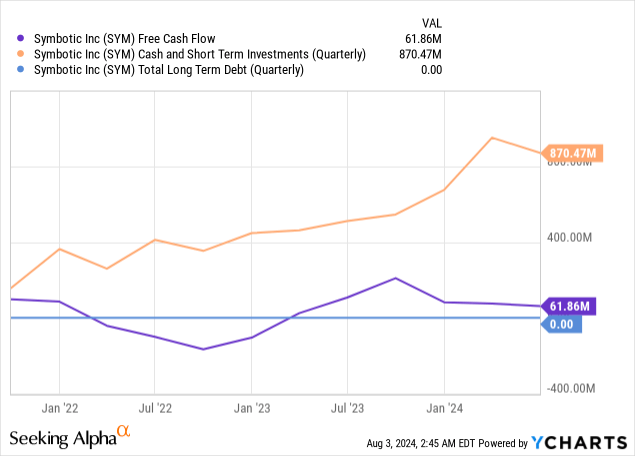

The company’s trailing 12-month (“TTM”) FCF was approximately $62 million, a significant drop from the $209 in TTM FCF that it was at in my December 29, 2023 article. The company has a solid balance sheet. It ended the quarter with $870.47 million in cash and equivalents and has no long-term debt. It has a quick ratio of 1.18, meaning it has enough money to pay its liabilities over the next year.

Data by YCharts

Data by YCharts

If the economy worsens, Symbotic should be able to ride out the downturn. Now, let’s look at the valuation.

SYM stock valuation

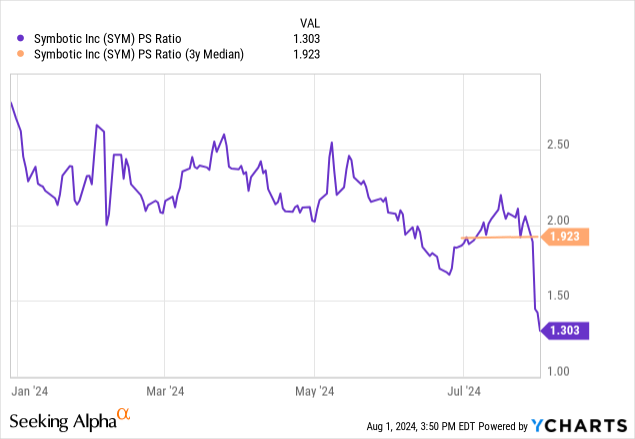

Symbotic has a price-to-sales (P/S) of 1.303, well below its three-year median. Suppose the company trades at its three-year median P/S; the stock price would be $38.69.

Data by YCharts

Data by YCharts

However, my previous article explained that the company has a dual-class share structure. The “P” in the P/S ratio is the company’s market capitalization (the number of outstanding shares multiplied by the share price). When considering only Class A shares, the P/S ratio is only 1.303. When including the Class V shares, the P/S ratio is 9.64 on August 1, 2024, significantly above the average Industrials P/S ratio of 1.56. At the time of my previous article, the P/S ratio, including the V shares, was 26.3. Many news sources only report the P/S ratio using class A shares. For instance, YCharts only shows the class A version. Investors need to remember that significant dilution will occur as V shares convert to A shares over time.

One general rule to determine a company’s valuation using analysts’ earnings-per-share (“EPS”) growth estimates and forward price-to-earnings (P/E) is that when a company’s EPS growth estimates exceed its forward P/E, the market undervalues the stocks’ EPS growth rate. According to that rule, the market undervalues Symbotic’s estimated EPS growth in fiscal 2025 and 2026.

Seeking Alpha

Suppose the stock’s 2025 forward P/E trades at its estimated growth rate of 151.78%; the stock price would be $68.30, up 176.5% over the company’s August 1, 2024, closing price of $24.70. If the stock’s 2026 forward P/E trades at its estimated growth rate of 76.66%, the stock price would be $60.56.

Symbotic Reverse DCF

The third quarter of FY 2024 reported Free Cash Flow TTM

(Trailing 12 months in millions)

$62 Terminal growth rate 3% Discount Rate 11% Years 1 – 10 growth rate 44.6% Current Stock Price (August 1, 2024, closing price) $24.61 Terminal FCF value $2.552 billion Discounted Terminal Value $11.235 billion FCF margin 3.6% Click to enlarge

Assuming a 3% terminal growth rate and an 11% discount rate, Symbotic would need to grow FCF 44.6% over the next ten years to justify the August 1, 2024 closing stock price. However, take this reverse DCF result with a massive grain of salt. A reverse DCF works best with companies with a relatively consistent FCF margin. As an early-stage company, its FCF is very inconsistent. Symbotic’s FCF margin was -28.01% in 2022 and 17.8% in 2023. Analysts expect its FCF margin will be 3.24% in 2024 and 8.39% in 2025.

Remember that the company’s margin declined because it is still fine-tuning the building and installation of its systems. If Symbotic can successfully tune its processes, it should increase its FCF margins. If the company can achieve an average FCF margin of 8% over the next ten years, it would need to grow its revenue by 33% over the next ten years to justify the current price. Suppose it can achieve an average FCF margin of 10%. In that case, revenue would only need to grow 29.7%. Analysts forecast the company will grow revenue at a 40.3% compound annual growth rate over the next three years.

Seeking Alpha

So, the company has the topline growth to justify its valuation, but may need to expand its FCF margins to 10% or higher to have an upside. For instance, at an FCF margin of 10% and a revenue growth rate of 33% over the next ten years, today’s estimated intrinsic value would be $30.90. This stock may be susceptible to news of slowing revenue growth or margin declines because it can negatively impact how investors value the stock.

Risks

This company has numerous risks. It is a former Special Purpose Acquisition Company (SPAC) that entered the public markets in June 2022, well before the Security and Exchange Commission (“SEC”) established disclosure rules for SPACs in January 2024. So, investors need to be aware that the company came to market in a way that didn’t require adequate disclosure of its risks. Many companies that have used the SPAC method to become publicly traded have a history of poor returns.

In addition to diluting shareholders, Symbotic’s dual share structure has other risks for investors. For instance, the company is ineligible to join several important indexes, including the Russell 2000, S&P 500 ((SPX)), and S&P MidCap 400 (SP400). The company’s exclusion from these indexes may hurt its valuation. Symbotic’s 2023 10-K states:

The multi-class structure of our common stock may make us ineligible for inclusion in certain indices and, as a result, mutual funds, exchange-traded funds, and other investment vehicles that attempt to track those indices would not invest in our Class A Common Stock. These policies are relatively new and it is unclear what effect, if any, they will have on the valuations of publicly-traded companies excluded from such indices, but it is possible that they may depress valuations, as compared to similar companies that are included. Given the sustained flow of investment funds into passive strategies that seek to track certain indices, exclusion from certain stock indices would likely preclude investment by many of these funds and could make our Class A Common Stock less attractive to other investors. As a result, the market price of our Class A Common Stock could be adversely affected.

Because the company also has a limited operating history and has yet to achieve consistent profitability on the bottom line, the market gives it little slack for operational missteps — among the reasons the stock is down so much after releasing its third quarter FY 2024 earnings report.

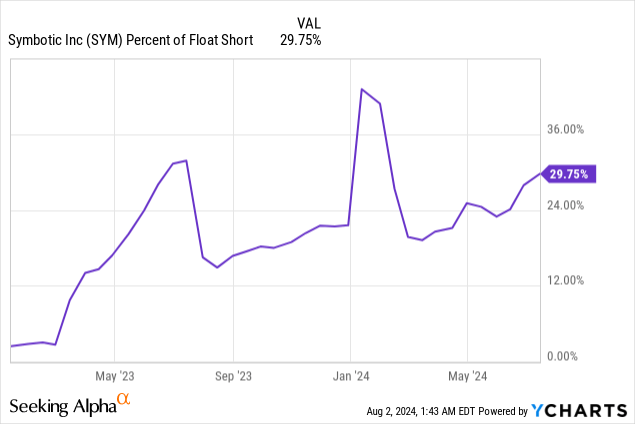

When I first wrote about this stock on December 29, 2023, 21.52% of its float was short. Today, 29.75% of its float is short. So, the company has a high degree of bearishness and negative sentiment.

Data by YCharts

Data by YCharts

Even after the stock’s post-earnings drop, there is a risk of further declines as the health of the consumer influences investor sentiment towards this warehouse automation company. Over the last several months, there has been a great deal of worry about consumer spending, especially among the demographic that shops at Walmart, a significant Symbotic partner.

Symbotic stock is a buy, but only as a speculation

This stock is among the higher-risk companies that I cover. Risk-averse investors should steer clear of it. However, Symbotic’s high potential upside and more favorable valuation compared to late December 2023 make it an exciting investment for investors willing to speculate. I am upgrading this stock to a buy, but only for risk-tolerant investors.

GIPHY App Key not set. Please check settings