Darren415

I last wrote about Planet 13 (OTCQX:PLNH) here two months ago, calling it a very cheap cannabis stock. Well, it is cheaper now, as the price is 13% lower. The company just reported its Q2, and I am even more confident now. In this piece, I discuss the fundamentals, look at the chart and compare its valuation to peers.

Q2 Was Strong for Planet 13

In Q2, revenue soared, boosted by a partial month for its Florida acquisition, VidaCann, which closed May 6th. Sequentially, revenue grew 36% to a record $31.1 million. This was 20% higher than a year ago. VidaCann added $7.3 million during its partial quarter. The 10-Q revealed that revenue would have been $36.8 million if VidaCann had been part of Planet 13 the entire quarter.

VidaCann boosted not only revenue, but also gross profits and adjusted EBITDA. The gross margin for the company was reported at 50.9%, and the company disclosed that the pro forma gross margin was 46.4%. A year ago, the company reported gross margin of 46.0%. Adjusted EBITDA was $3.2 million compared to $2.8 million a year ago and breakeven in Q1.

According to AlphaSense, two analysts are projecting big growth for Planet 13. After the report, they think that 2024 revenue will rise 83% to $180 million, with 2025 revenue of $250 million. I am not seeing forward adjusted EBITDA estimates, but a 12% adjusted EBITDA margin would yield adjusted EBITDA of $30 million.

The company updated its balance sheet, with some debt assumed following the VidaCann acquisition. Net cash at the end of the quarter was $16.4 million. Tangible book value fell to $87.9 million.

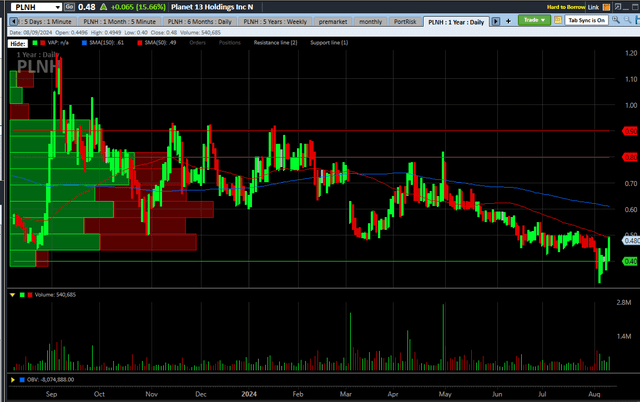

The Planet 13 Chart Broke Down

One of the reasons I liked the stock so much was that I thought it had limited downside due to its strong balance sheet and low valuation. This proved wrong, as the stock broke down badly, setting an all-time low ahead of its Q2 report:

Schwab

I am not sure what drove it down, but it made that 15.7% rally on Friday kind of meaningless to me. I see support at $0.40, and I see potential resistance at $0.80 and $0.90. The warrants from that equity offering are at $1.04.

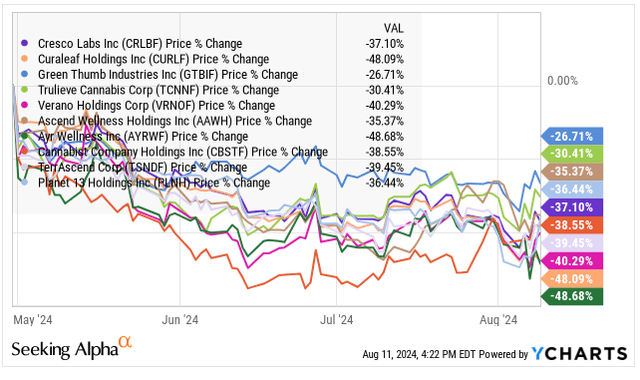

Planet 13 has fallen, but it is not alone. All cannabis stocks have been pulling back, especially the MSOs. Here is the action for Planet 13 and the Tier 1 and Tier 2 names since 4/30, when the market peaked:

YCharts

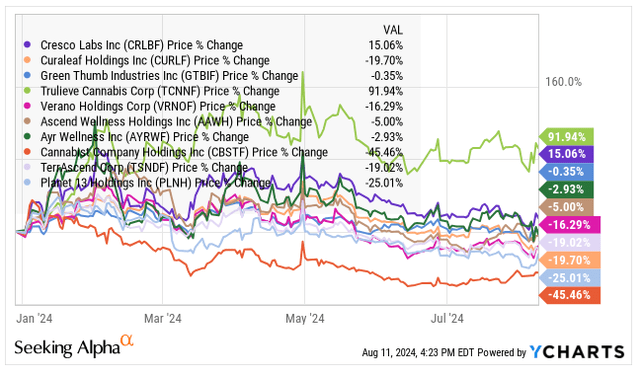

Here are the year-to-date returns:

YCharts

So, Planet 13, down 25% year-to-date, is one of the worst performers in 2024.

Planet 13 Is a Cheap Stock

It’s important to remember how few publicly traded MSOs have positive tangible book value or net cash. I think Planet 13 really stands out. It currently trades at 1.8X tangible book value.

Investors seem to favor the very large MSOs, but these large companies are challenged to grow. They are already in lots of markets, and doing M&A to expand is tough. Planet 13 has new markets it could enter, and it would be a good acquisition candidate too.

It looks like no other MSO can grow as much as Planet 13 in 2025, but the stock isn’t widely followed. I think that investors will start paying attention to the 2025 outlook soon. Ahead of this strong quarterly report, I had shared a year-end target of $0.86 based on achieving an enterprise value of 8X projected adjusted EBITDA in 2025 of $23 million. My best guess is that the projections will be higher than this.

Conclusion

I like some MSOs a lot right now. It seems like cannabis will be rescheduled, and the end of 280E is a good thing for these companies. My model portfolio at 420 Investor has a 1/3 exposure to MSOs through four names, and Planet 13 is my largest MSO position currently at 12.5%. This is my 4th largest position overall.

The strong balance sheet at Planet 13 should protect it to the downside if 280E stays in operation, but its elimination will boost the after-tax income of the company. The stock should have substantial growth. It’s not widely followed at this point and stands out to me as being very attractively priced.

I have been optimistic about the opportunities for the company in Florida if its voters opt to approve adult-use in the elections in November. This would be their fourth adult-use state, if so, and I think the company knows how to do adult-use. I just spent 11 days in NYC, and I visited a store there near Times Square (Nicklz). That market is finally picking up as the state clamps down on the unlicensed retailers and offers more licenses, too. I think that New York would be a great market for Planet 13 to open a superstore.

Planet 13 doesn’t need to get into New York for its investors to do very well. It is big in Nevada, a market that has stalled recently but could lift. It is new to California, a state with a lot of opportunity. It has a single store in Illinois near the Wisconsin border. Finally, it is now much larger in Florida’s medical cannabis market following an acquisition, and investors should benefit greatly if the state goes adult-use. Planet 13 seems to have limited downside and tremendous upside.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

GIPHY App Key not set. Please check settings