Shutthiphong Chandaeng

Investment Thesis

The Trade Desk (NASDAQ:TTD) is set to report its Q2 2024 resultsthe following Thursday, 8 August, after hours.

I’ll cut to the chase, TTD is priced at 30x next year’s EBITDA. This makes it arguably the most expensive advertising stock. And if we put aside its long-term narrative about multiple tailwinds, its fundamentals today point to a company that is growing at mid-20s% and not more.

In sum, I don’t believe this stock offers investors a satisfactory risk-reward. Being asked to pay $100 per share for TTD is too much for me.

Rapid Recap

In June, I said,

While I recognize that there is a lot to like in its prospects, I ultimately don’t believe there’s enough margin of error in its valuation. Or better put, I believe there are better opportunities elsewhere.

Author’s work on the TTD

The Trade Desk is a stock that I’ve mostly rated as a hold in the past 12 months. And during this period, as I noted in my quote, the stock has underperformed the S&P500 as there have been better opportunities elsewhere.

Looking ahead over the next year, I’m not convinced that its prospects are all that enticing. Here’s why.

The Trade Desk’s Prospects Are Mixed

I’ll describe what The Trade Desk does, followed by its bullish drivers, before discussing some timely negative elements.

The Trade Desk enables advertisers to buy and manage digital advertising space with precision and efficiency. Their platform helps advertisers select where to place ads, analyze data to target specific audiences, and optimize campaigns for better results. Specializing in Connected TV and retail media, The Trade Desk aims to make advertising more personalized and effective for brands.

In the near term, The Trade Desk is positioned to continue outpacing the broader digital advertising industry. This growth is driven by the increasing adoption of UID2, which enhances the use of first-party data and the value of the open internet. The company’s partnerships with major industry players like Disney (DIS) and Roku (ROKU) in the Connected TV space expand opportunities for advertisers to reach audiences with premium content, highlighting the company’s potential for sustained success.

Additionally, The Trade Desk’s commitment to transparency and leveraging advanced technology for better decision-making positions it well within the nearly $1 trillion advertising market. The rise of subscription companies incorporating advertising to diversify revenue streams, as seen with Netflix’s (NFLX) ad-supported tier, further bolsters The Trade Desk’s prospects.

That’s the positive narrative. Now let me put forth the following aspect.

Data by YCharts

Data by YCharts

On the back of Alphabet’s (GOOG)(GOOGL) earnings results, the market has decidedly skewed away from advertising companies. Alphabet’s advertising was up 11% y/y, which was rather middle of the road. Even though Alphabet noted the strength of advertising, I believe that this rather pedestrian growth rate is a read-through to The Trade Desk too. My point is that despite it being an election year and many above-noted tailwinds, the fundamentals don’t appear to be all that strong. Or better put, as strong as expected.

Given this balanced background, let’s now discuss its fundamentals in more detail.

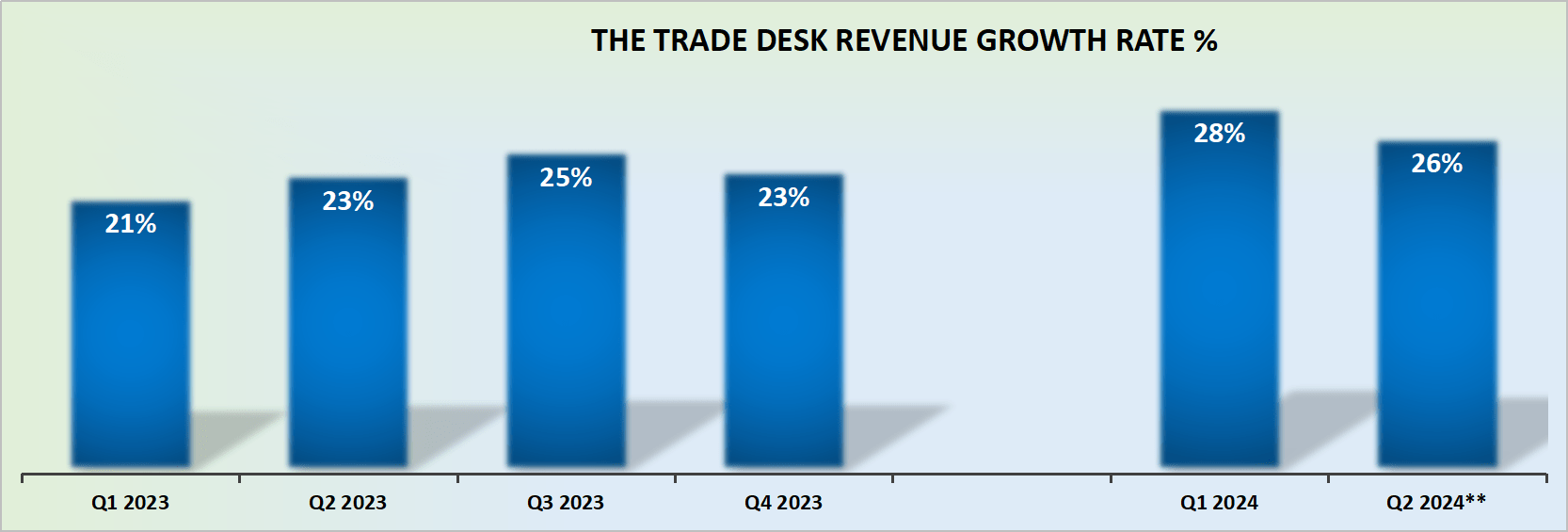

Revenue Growth Rates Could Deliver Mid-20s CAGR

TTD revenue growth rates

The Trade Desk has demonstrated that it can deliver premium growth over many years. Premium growth is a +20% compounded annual growth rate (”CAGR”), that investors can count on. Growth that is steady, predictable, and strong. This type of growth commands a premium on its stock. But before we get ahead of ourselves, let’s analyze The Trade Desk’s outlook for the remainder of 2024 and into 2025.

As its comparables are now rather easier, investors can expect The Trade Desk to deliver at least 20% CAGR. And yet, the problem here is that The Trade Desk is unlikely to return to growing at +30% any time soon.

So, putting aside its narrative of its very long tailwinds, this is a company barely delivering $2.5 billion in revenues, and its growth rates have already moderated.

As a reference point, AppLovin (APP) is delivering practically twice this revenue and strong growth rates and it’s priced substantially cheaper too. Accordingly, this brings up the following consideration, after a while, valuation matters.

TTD Stock Valuation — 30x Next Year’s EBITDA

Here are my back-of-envelope calculations. We know that The Trade Desk is on a path for $400 million of EBITDA in H1 2024. We also know that Q4 of each year is a seasonally strong quarter for advertising stocks, so we must factor in that aspect too.

Hence, I believe that The Trade Desk will achieve at least $1 billion of EBITDA in 2024, and might even exceed expectations by reaching $1.1 billion.

That question though, is whether the market is able to get enough conviction of The Trade Desk being on a path towards $1.5 billion of EBITDA in 2025?

As it stands right now, The Trade Desk is substantially more expensive than AppLovin, Meta (META), and Alphabet. Does this make for a compelling enough risk-reward bet? I’m not confident enough to make this assertion.

The Bottom Line

While The Trade Desk has many positive aspects, such as its advanced technology and strong partnerships, paying 30x next year’s EBITDA is a poor risk-reward.

The company is priced significantly higher than its peers like AppLovin, Meta, and Alphabet, despite its revenue growth moderating to mid-20s%.

This high valuation leaves little margin for error, especially considering the broader market’s lukewarm sentiment towards advertising stocks following Alphabet’s modest 11% y/y growth in advertising revenues. Given these factors, investing in The Trade Desk at such a high multiple seems too risky, with better opportunities available elsewhere in the market, for example, AppLovin.

GIPHY App Key not set. Please check settings